D2C (direct-to-consumer) e-commerce: Global market, leading players, regional trends

Discover how direct-to-consumer e-commerce is reshaping global retail, with insights on leading brands, regional trends, and market maturity. (Ad)

By Nadine Koutsou-Wehling, Data Journalist

Direct-to-consumer (D2C) e-commerce is a business model in which retailers manage the entire product journey from manufacturing to final sale through their own online store. By design, the model bypasses traditional retail intermediaries and excludes sales via third-party marketplaces.

D2C became especially popular during the pandemic, when retailers sought to reach customers beyond physical retail and wholesale channels. One of the model’s core advantages is the high degree of control it offers over the customer journey, alongside access to valuable first-party purchasing and behavioral data.

Since then, D2C has continued to expand within global e-commerce, although adoption and impact vary widely by region. Here is an overview of the current state of the global direct-to-consumer e-commerce market.

Top D2C retailers highlight the model’s advantages

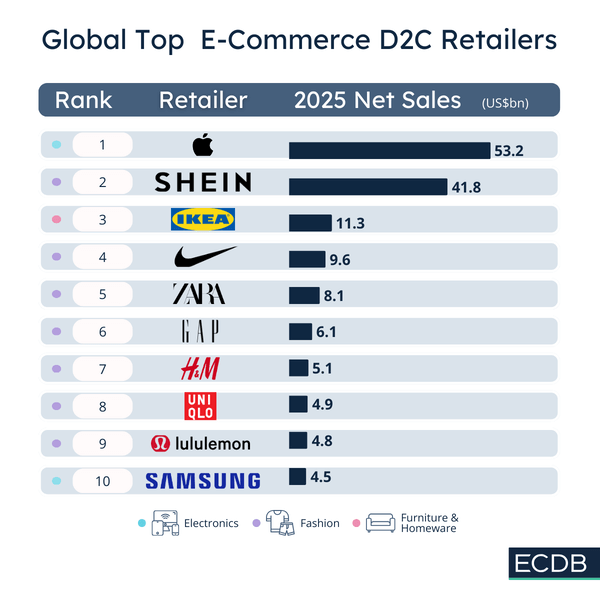

D2C revenues have grown steadily since 2020, which highlights the advantages this model brings to retailers and customers. Several retailers stand out globally for their scale and strength in direct-to-consumer e-commerce.

Apple leads worldwide with US$53.2 billion in D2C e-commerce sales, followed by Shein with US$41.8 billion. Ikea ranks third, generating US$11.3 billion in D2C net sales.

Most of the remaining brands in the top 10 are fashion retailers, including Nike, Zara, GAP, H&M, Uniqlo and Lululemon. Their strong representation responds to the structural advantages that D2C provides to the fashion industry.

Fashion retail is characterized by frequent product launches and rapidly shifting trends. D2C enables brands to react quickly, introduce limited collections, and test consumer demand without being constrained by traditional wholesale buying cycles.

Regional distribution of D2C revenues: Europe and North America lead

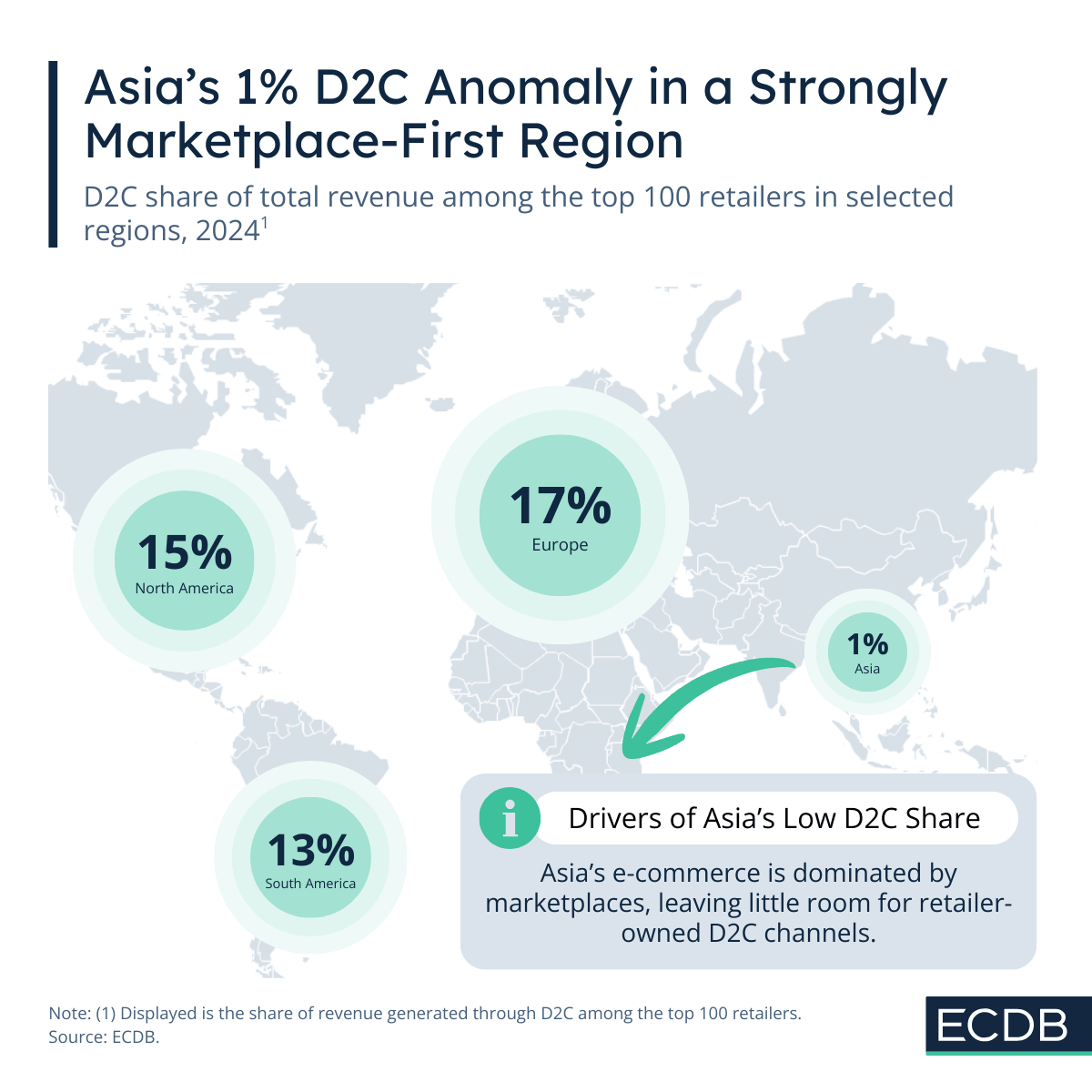

The D2C model is most established in Europe and North America. In Europe, D2C e-commerce accounts for 17% of total e-commerce revenues, while in North America the share stands at 15%.

South America and Asia trail behind. In South America, D2C brands generate around 13% of total e-commerce revenues, which remains a meaningful share. Asia presents a markedly different picture: only 1% of e-commerce revenues are attributed to D2C retailers. This disparity is largely driven by the dominance of large online marketplaces across the region. Marketplaces have played a central role in the development of Asian e-commerce, while D2C brands are often imported from Western markets rather than homegrown.

Market maturity is a key factor behind these differences. Established brands operating their own online stores have a longer history in Europe and North America, which is why their impact is so much higher.

In addition, both North American and European e-commerce are defined by brand loyalty and consumer purchasing behavior that highlights users’ unique identity. This applies to categories such as fashion, beauty, and home goods. D2C brands thrive in this environment, because they leverage own storytelling and a distinct social media presence combined with influencer marketing.

North America’s top 10 D2C retailers

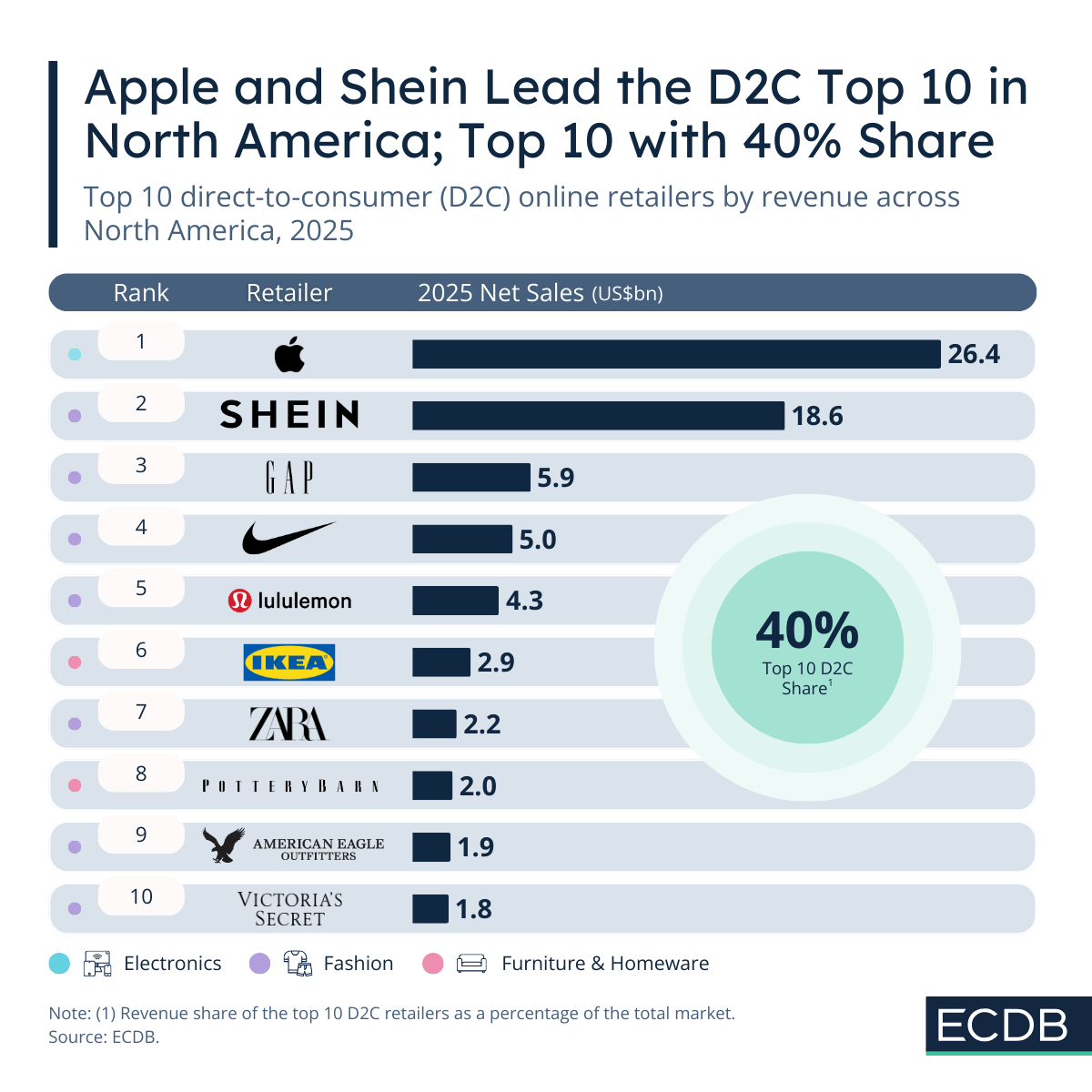

As a rule, the top 10 retailers have the greatest impact in markets where D2C is less developed as a business model. In markets where D2C is still developing, a few large retailers tend to dominate and capture most of the revenue. In more mature markets, such as North America, the market is more diverse, with many smaller D2C brands sharing influence rather than a few companies controlling it.

Apple leads the North American D2C market with US$26.4 billion in net sales in 2025, followed by Shein with US$18.6 billion. GAP, Nike, and Lululemon occupy positions three through five. They reflect the continued strength of established D2C apparel brands in the region.

Together, the top 10 D2C players hold a 40% share of the total market. Smaller D2C players account for the remaining 60% of D2C revenues.

Europe’s D2C market: Apple, Shein, and Ikea dominate

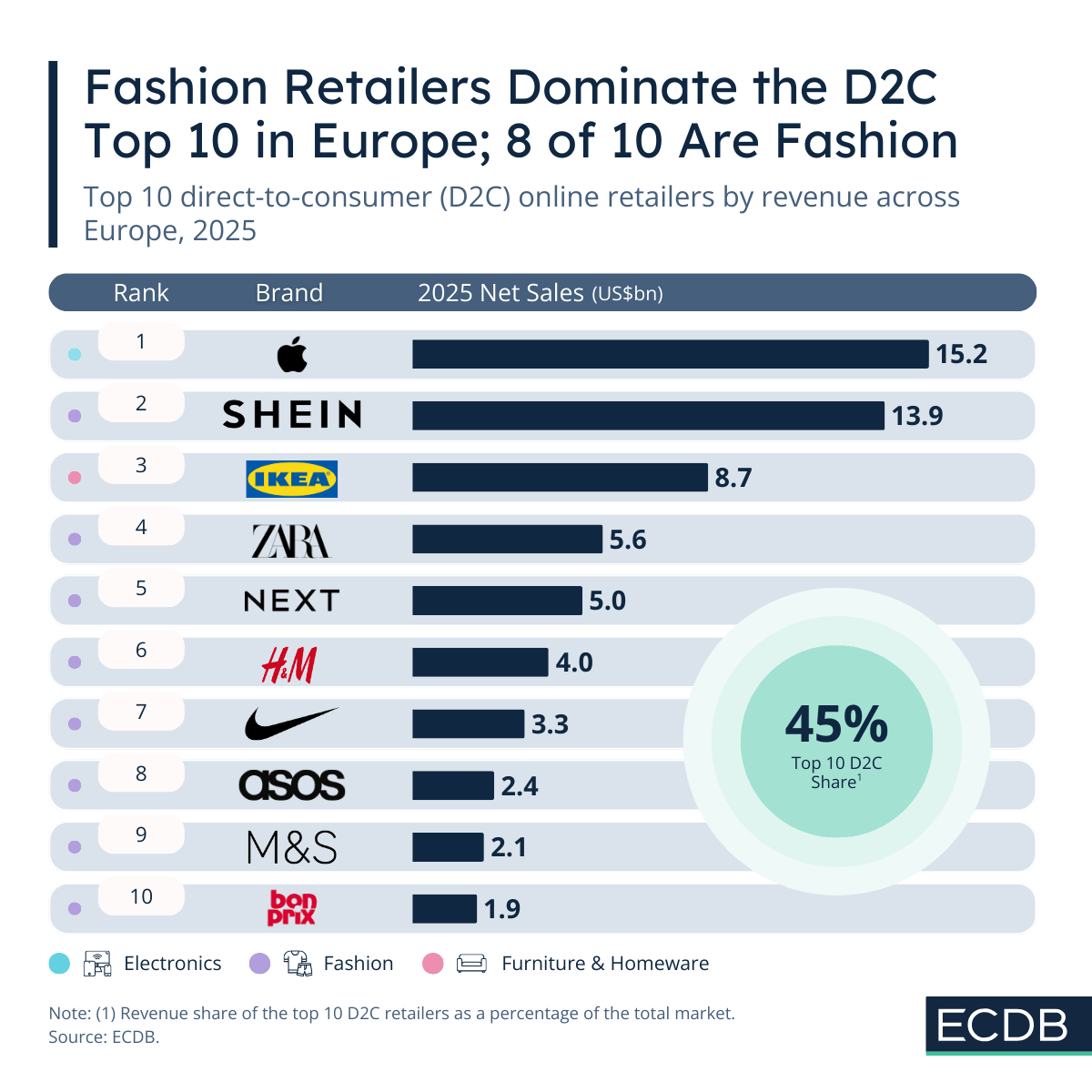

Europe has long been a hotspot for D2C e-commerce, though the market is more concentrated among the top players. This concentration is partly driven by the influence of Eastern and Southern Europe, where D2C remains less developed.

Top D2C retailers in Europe are Apple, with US$15.2 billion in net sales, Shein with US$13.9 billion, and Ikea with US$8.7 billion.

Strong UK-based fashion brands further reinforce the conclusion that Europe’s D2C landscape is shaped by a combination of established legacy brands and fashion-driven business models. In this environment, direct customer relationships, brand identity, and control over distribution remain central to competitive success.

D2C e-commerce: A growing force shaped by region and market maturity

Direct-to-consumer e-commerce has established itself as a powerful and lasting retail model, driven by greater control over the customer journey and access to valuable first-party data. While D2C adoption accelerated during the pandemic, its long-term impact varies significantly by region and is shaped by market maturity, consumer behavior, and the role of online marketplaces.