Why is electronics among the top e-commerce categories in Germany?

Explore the factors making electronics a top e-commerce category in Germany. Gain insights into consumer trends and the industry’s growth potential.

Electronics in Germany sit in a curious place. They are among the most researched products, rarely bought on impulse, and often associated with caution rather than excitement. And yet, year after year, electronics remain one of the strongest and most stable e-commerce categories in the country.

This isn’t driven by novelty or short-term trends. It’s driven by structure. The way Germans compare prices, assess quality, trust retailers, and expect logistics to work creates a near-perfect environment for buying electronics online. What might feel like a complex purchase elsewhere becomes a controlled, predictable process here.

In this article, we look at the real reasons electronics perform so well in German e-commerce and then ground those reasons in data. Let’s dive.

Why electronics resonate so strongly with German online shoppers

Electronics stand out in German e-commerce because they align with how people here like to shop.

These products sit at the intersection of planning, comparison, and trust. They are rarely emotional purchases, and rarely rushed. That alone makes them unusually compatible with online shopping in Germany.

What the data confirms is rooted in everyday behavior. Germans approach electronics as functional investments. They want to understand what they are buying, why it costs what it costs, and how long it will last. Online channels support that mindset better than physical retail, especially once the surrounding infrastructure — payments, logistics, consumer protection — removes friction from the process.

Below are the core reasons electronics have become one of the strongest and most stable e-commerce categories in Germany.

Electronics buying starts with research

Electronics purchases almost always begin long before checkout. Consumers compare specifications, read reviews, check energy ratings, and look for long-term value. This kind of decision-making does not fit well into a quick store visit, especially for higher-priced items.

Online stores support research naturally. Product pages can show detailed specs, comparison tables, compatibility information, and long-form reviews all in one place. Shoppers can pause, return later, and continue where they left off. That matters in a market where buying decisions are rarely rushed.

In Germany, this research-driven behavior is not limited to expensive devices. Even mid-range electronics often go through a comparison phase. E-commerce does not change how Germans decide — it matches it.

Price comparison is deeply embedded in buying culture

German consumers are known for being price-aware, but that does not mean they simply chase the lowest number. Instead, they compare values.

They look at price differences between retailers, consider shipping costs, warranty terms, and return conditions, and often track prices over time.

Electronics are particularly well-suited to this behavior.

Products are standardized, comparable, and transparent. A laptop or washing machine has measurable attributes that can be evaluated side by side. Online platforms make this process easier and more efficient than offline retail.

This is also where trust in established platforms plays a role. Marketplaces and large electronics retailers simplify comparison while signaling reliability. For electronics, e-commerce turns price sensitivity into confidence rather than hesitation.

Trust in consumer protection reduces perceived risk

Electronics are not low-risk products. They can be expensive, fragile, and complex. Buying them online only works when consumers feel protected if something goes wrong.

Germany’s strong consumer protection framework supports that confidence. Clear return policies, statutory warranties, and transparent seller obligations reduce fear around online purchases. When combined with reputable retailers, this creates a sense of safety that is critical for electronics.

Returns are expected to work smoothly. That expectation lowers the barrier to buying devices online, even for cautious shoppers. Electronics succeed online in Germany because the system absorbs risk, not the buyer.

Logistics reliability supports bulky and fragile products

Electronics place high demands on logistics. Devices must arrive on time, undamaged, and with clear tracking. Failed deliveries or unclear return processes quickly damage trust, especially for high-value goods.

Germany’s logistics infrastructure meets those expectations consistently. Parcel delivery is reliable, tracking is standard, and returns are well integrated into consumer routines. OOH delivery, parcel lockers, and predictable timelines make electronics feel manageable rather than risky.

This infrastructure matters more for electronics than for many other categories. A reliable logistics system turns complexity into normality, which is exactly what electronics need to scale online.

Familiar payment methods lower checkout friction

Payment preferences in Germany are conservative, especially for higher-value purchases. Consumers want familiar, trusted methods that offer protection and transparency.

Electronics benefit from this environment. Widely accepted options like PayPal, cards, and bank-based methods reduce hesitation at checkout. Buyers know what happens if something goes wrong, how refunds work, and which protections apply.

For electronics, where order values are higher and replacement cycles longer, this predictability matters.

Electronics are replacement-driven, not trend-driven

Unlike fashion or lifestyle products, electronics are rarely purchased to follow trends. They are replaced when something breaks, becomes inefficient, or no longer meets practical needs. That replacement cycle creates steady demand rather than seasonal spikes.

Online shopping fits this pattern. When a device fails or needs upgrading, consumers already know what they want. They search, compare, and buy without browsing aimlessly. E-commerce supports efficiency better than physical stores.

This replacement-driven demand helps explain why electronics remain stable even during uncertain economic periods.

They are functional necessities, not discretionary indulgences.

Home and work increasingly overlap

Another reason electronics perform well online is the blending of private and professional use. Home offices, freelancers, and small businesses often buy the same devices through consumer channels.

This hybrid demand increases volume and normalizes online buying. A monitor or router may serve both personal and work purposes. Buying it online feels practical, not exceptional.

Electronics benefit from this overlap because online retailers already support invoicing, delivery flexibility, and documentation needs.

The boundary between B2C and small-scale B2B demand is thin in this category.

Sustainability and efficiency influence decisions

German consumers increasingly consider energy efficiency, repairability, and lifespan when buying electronics. Online platforms make this information easier to access. Energy labels, detailed specs, and long-term reviews support informed decisions.

Refurbished electronics and certified resellers also find a natural place online. These options appeal to cost-conscious and sustainability-aware buyers alike. Physical retail often struggles to present these alternatives as clearly.

What the data says about electronics in German e-commerce

If you step back and look at the numbers, one thing becomes clear very quickly: electronics are not a temporary winner in German e-commerce. They are a deeply established category that keeps growing, stabilizing, and adapting at the same time. The data does not point to hype cycles or sudden spikes driven by trends. Instead, it shows a category that fits the structure of the German online market unusually well.

Below, we break this down into the most important data-driven signals that explain why electronics remain among the top e-commerce categories in Germany.

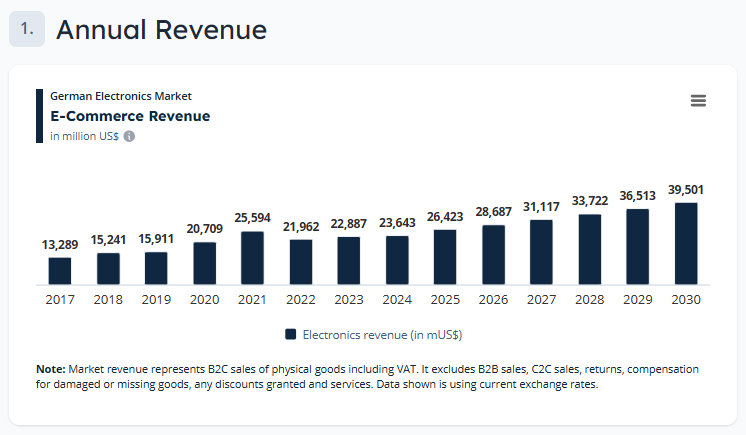

Electronics e-commerce revenue keeps growing, even after peak years

German electronics e-commerce revenue has followed a long, steady upward curve. From around $13.289 billion in 2017, the category grows year after year, reaching $25.594 billion in 2021. That year marks a peak shaped by pandemic behavior, but what matters more is what happens after.

Instead of collapsing, revenue stabilizes and resumes growth. By 2025, electronics e-commerce revenue should reach about $26.423 billion, and projections point toward nearly $39.501 billion by 2030. That trajectory matters. It shows electronics did not rely on temporary conditions. They adjusted.

What stands out here is not just growth, but resilience. Even after a contraction year in 2022, the market recovers and returns to a predictable pace. This pattern suggests that online electronics buying has become a default habit, not a situational choice.

Source: ECDB, German Electronics Market

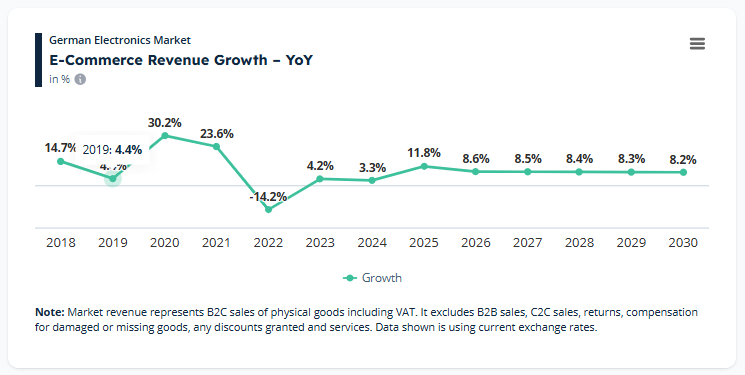

Growth rates normalize, which signals market maturity, not decline

Year-over-year growth tells how Germans buy electronics online. During peak years like 2020 and 2021, growth rates exceeded 20%. That phase ends, as expected. What follows is more interesting.

From 2025 onward, growth should stabilize in the range of 8 to 12% annually. Nothing explosive, but it is consistent. In a market as large and competitive as Germany, that level of growth reflects confidence and routine behavior.

In other words, electronics have entered a mature phase of e-commerce adoption. Consumers are not experimenting anymore. They know where to buy, how returns work, and what to expect from delivery and support. Stable growth here signals trust.

Source: ECDB, German Electronics Market

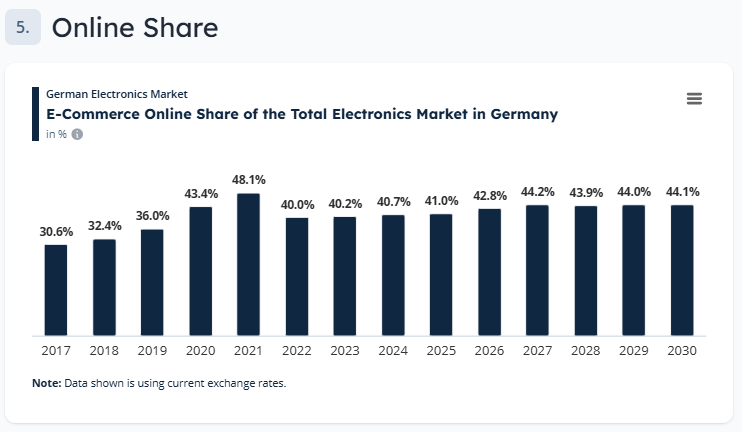

Online share of electronics continues to increase

Another strong indicator comes from the online share of total electronics sales in Germany. In 2017, around 30% of electronics sales happened online. By 2021, that number will peak at over 48%. After that, the share adjusts downward slightly but continues to climb again over time.

By 2025, online share reaches around 41%, and projections show it moving toward 44.1% by 2030. That matters because electronics still have a strong offline presence. Physical stores remain relevant, especially for consultations and immediate purchases.

The data suggests a stable split rather than a winner-takes-all shift. Electronics are increasingly researched and purchased online, even when offline channels remain part of the journey.

Source: ECDB, German Electronics Market

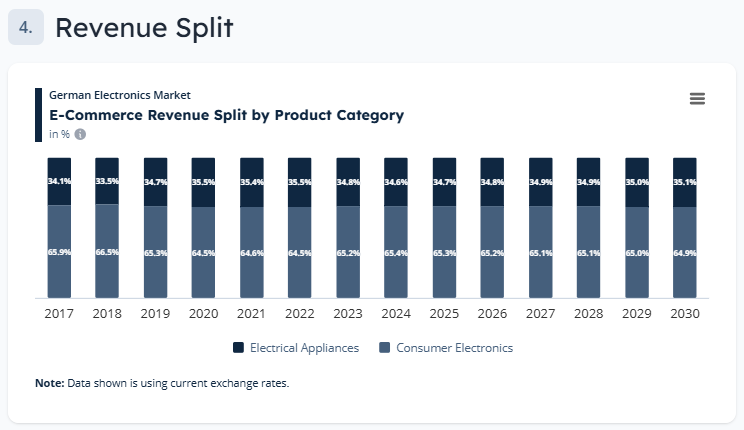

Consumer electronics dominate, but appliances stay consistently relevant

Looking at the internal split of the electronics category reveals another important detail. Consumer electronics account for roughly two-thirds of e-commerce revenue, while electrical appliances make up about one-third. This balance remains surprisingly stable over time.

Consumer electronics benefit from faster replacement cycles, innovation, and frequent upgrades. Appliances, on the other hand, are slower-moving but essential. They do not spike, but they do not disappear either.

This mix explains part of the category’s strength:

- Consumer electronics drive volume and frequency

- Appliances add stability and higher average order values

Together, they create a category that performs well across economic cycles.

Source: ECDB, German Electronics Market

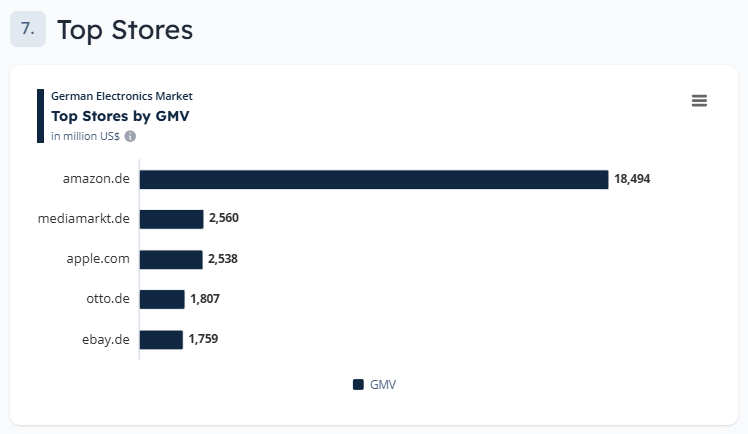

A small number of players control a large share of GMV

When you look at the top stores by GMV in the German electronics market, concentration becomes obvious. Amazon.de dominates with roughly $18.5 billion in GMV, far ahead of the rest. MediaMarkt, Apple, Otto, and eBay follow, each in the range of $1.7 to $2.6 billion.

This concentration reflects consumer behavior. Germans tend to trust established retailers for high-value purchases. Electronics amplify that tendency because warranties, returns, and after-sales support matter more here than in many other categories.

At the same time, the presence of both marketplaces and specialized retailers shows diversity:

- Marketplaces offer selection and price comparison

- Specialized retailers offer expertise and brand assurance

Electronics benefit from both models coexisting, rather than competing directly.

Source: ECDB, German Electronics Market

Payment preferences reduce friction for high-value orders

Payment method data reinforces why electronics work well online in Germany. PayPal appears in over 80% of electronics stores, followed by Visa and Mastercard. Bank transfer options also remain widely available.

This mix matters. Electronics purchases often involve higher ticket sizes, and German consumers value payment security and buyer protection. Familiar methods reduce hesitation at checkout.

The relatively lower share of newer payment options compared to core methods suggests something else as well: electronics buyers prefer reliability over experimentation, especially when spending more.

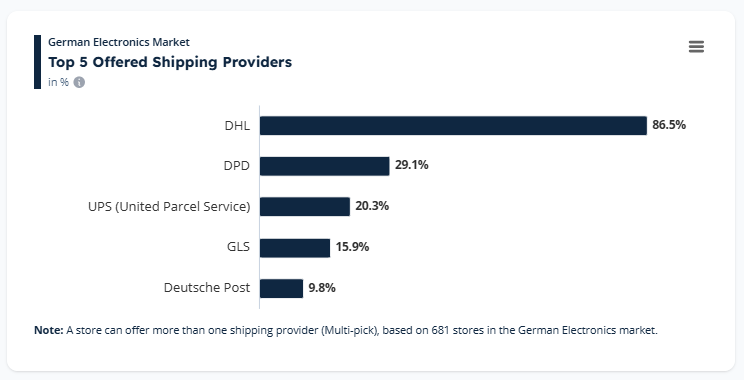

Logistics infrastructure aligns well with electronics’ needs

Shipping provider data highlights another structural advantage. DHL appears in over 86.5% of electronics stores, with DPD, UPS, GLS, and Deutsche Post following behind.

Electronics require predictable delivery, careful handling, and transparent tracking. Germany’s logistics infrastructure supports that expectation extremely well. Parcel lockers, home delivery, and return logistics are already embedded into consumer routines.

This matters because electronics are not forgiving products. Missed deliveries or damaged goods quickly erode trust. The logistics setup in Germany lowers that risk, making online electronics purchases feel safe.

Source: ECDB, German Electronics Market

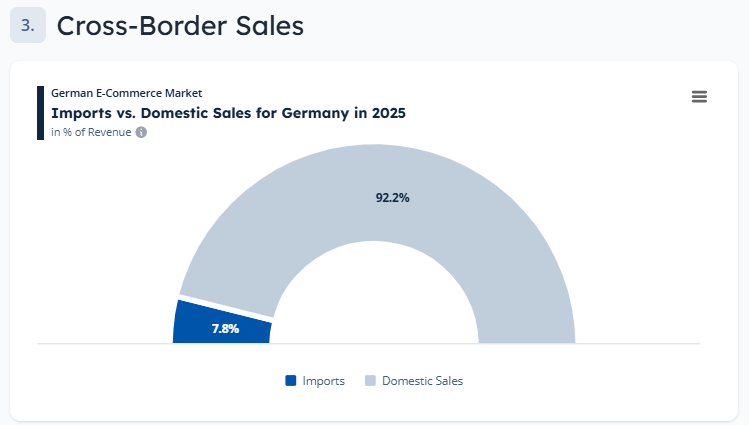

Domestic sales dominate, with limited reliance on imports

Cross-border data shows that over 92.2% of electronics e-commerce revenue comes from domestic sales. Imports account for less than 8 percent. Even when imports occur, they are heavily concentrated, with Greater China representing over 80% of import volume.

This tells us two things. First, German consumers prefer buying electronics from domestic or locally established retailers. Second, supply chains are already optimized for electronics, reducing dependency on cross-border uncertainty.

Electronics e-commerce in Germany is not fragile or experimental. It is domestically anchored and operationally mature.

Source: ECDB, German Electronics Market

Taken together, the data explain the category’s strength

When you connect these signals, the picture becomes clear. Electronics succeed in German e-commerce not because they are trendy or impulsive, but because they align with how the market works.

They benefit from:

- steady long-term revenue growth

- predictable, normalized YoY performance

- increasing online share without eliminating offline trust

- concentrated but trusted retail players

- familiar payment methods

- strong domestic logistics and supply chains

Electronics fit the German e-commerce model almost perfectly. And the data shows that this category has found its place and continues to perform quietly, year after year.