Market concentration: A few players shape world e-commerce at the top

Global e-commerce surpassed $5 trillion in 2026, but growth is highly concentrated. China, the US, and leading platforms capture most of the market expansion. Read more insights from ECDB in this article. (Ad)

By Nadine Koutsou-Wehling, Data Journalist

After a period of slowdown and recalibration, the global e-commerce market is accelerating once again. Yet the recovery is far from evenly distributed. Beneath the headline growth figures lies a more concentrated reality: momentum is being driven by a small group of standout markets.

When we break down net growth by country, it becomes clear that a handful of leading players are responsible for the lion’s share of expansion, while much of the world struggles to keep pace.

This insight is part of the new ECDB report Global E-Commerce Compass 2026, which offers a comprehensive analysis of worldwide e-commerce trends and the leading markets and players shaping the industry.

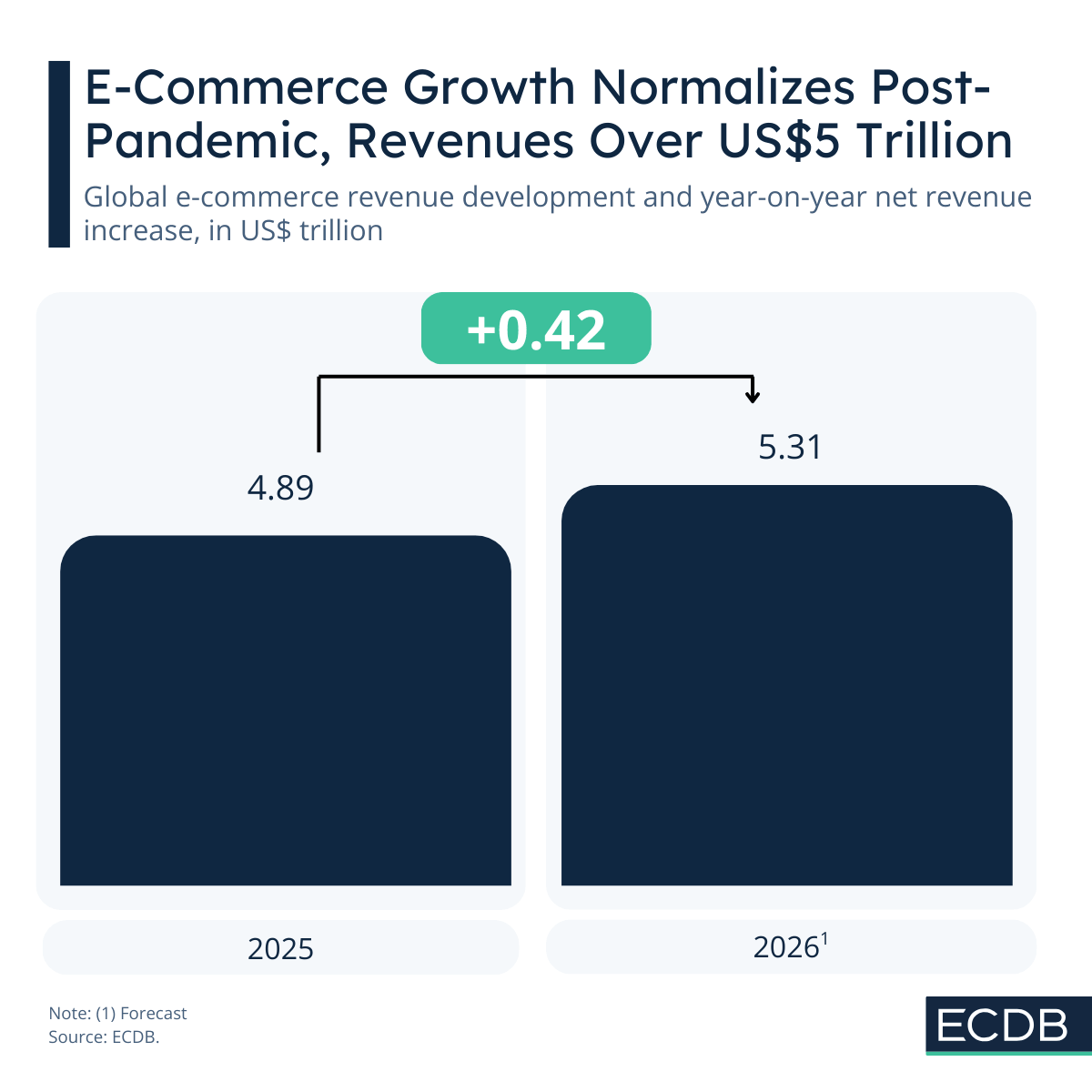

Global e-commerce adds $421 Billion in Net Growth in 2026

In 2026, global e-commerce surpassed the US$5 trillion threshold. The increase from 2025 marked US$421 billion, driven by contributions of various markets and players.

Top markets and players reveal how concentrated e-commerce is becoming, given that the largest ones capture a majority of the e-commerce growth share.

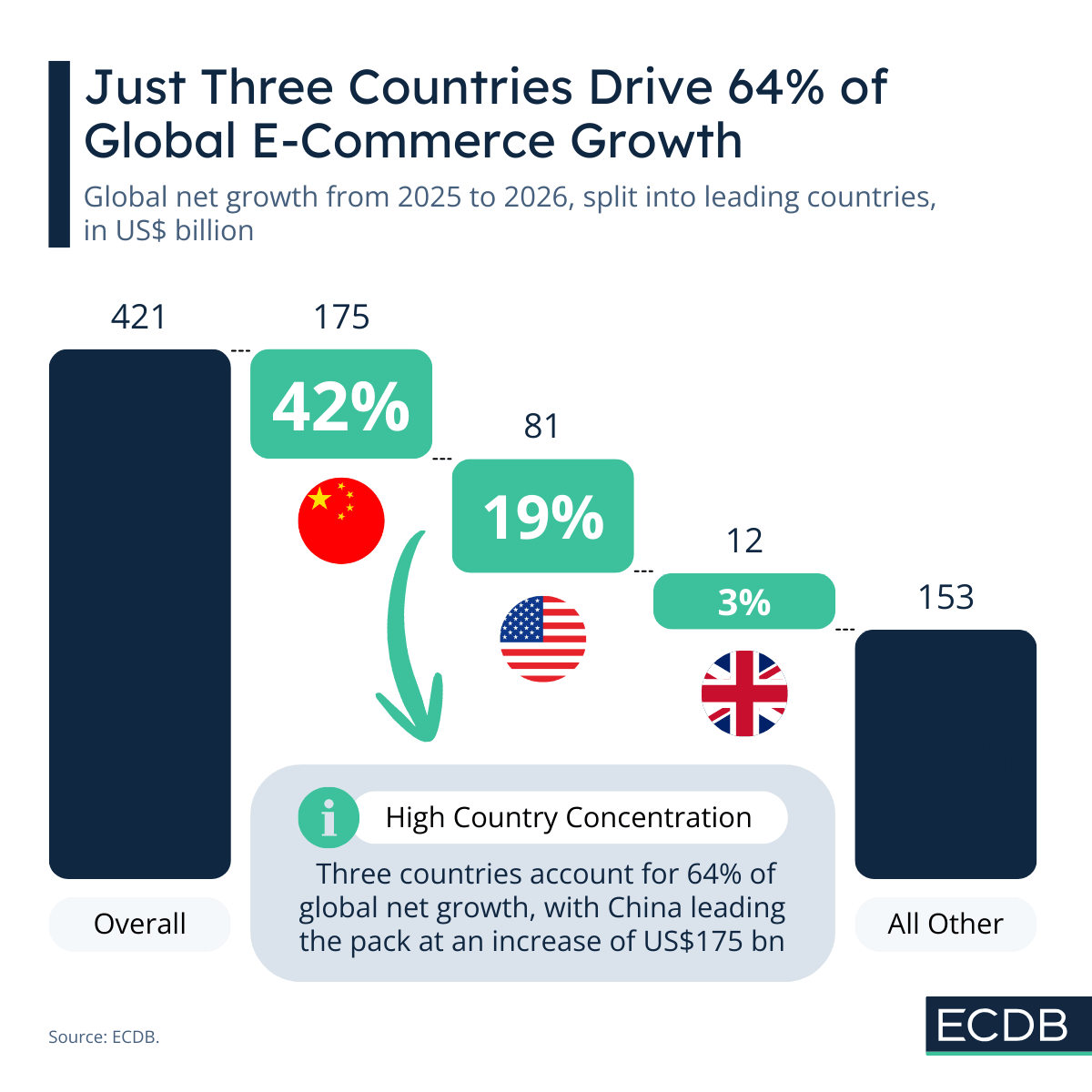

Greater China Accounts for 42% of Global E-Commerce Growth

Net growth measures each market’s absolute contribution to overall revenue increases. In 2026, Greater China leads in both size and impact by contributing US$175 billion in e-commerce revenue. This is a share of 42% of total net growth.

Trailing behind are the United States with US$81 billion (19%) and the United Kingdom with US$12 billion (3%). Together, these three markets account for 64% of global e-commerce growth. Their position emphasizes both the current concentration of the market and its likely intensification in the years ahead.

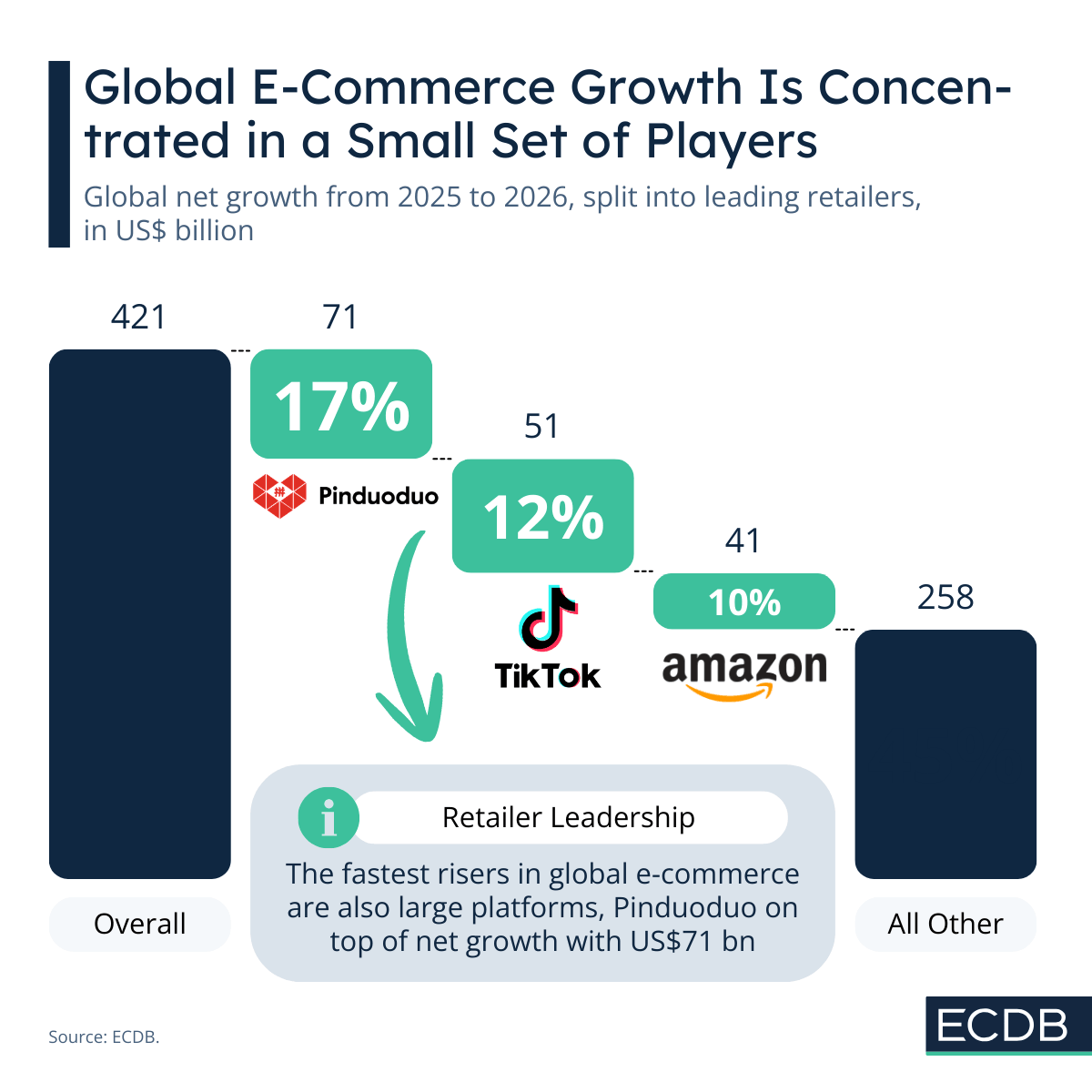

Three Players Capture Nearly 40% of New E-Commerce Revenues

The picture shifts slightly for individual players. The largest platforms remain the biggest contributors to total growth, but unlike at the country level, the top three do not dominate the majority. Together, Pinduoduo, TikTok (Douyin), and Amazon account for 39% of global e-commerce growth in 2026.

Pinduoduo, sister company to Temu, is the highest growing player with a net growth of US$71 billion and a share of 17%. TikTok (Douyin) follows with US$51 billion and 12%. Ultimately, Amazon represents US growth with a net growth value of US$41 billion and 10%.

These net growth increases contribute to a status quo in which the world market is already highly concentrated. In absolute numbers, the two leading countries are far ahead of the rest.

Revenue Concentrated at the Top: China and the US

While net growth figures highlight the market’s dynamic momentum, the static revenue view tells a story of clear structural dominance. It shows the image of two giants standing well ahead of the rest.

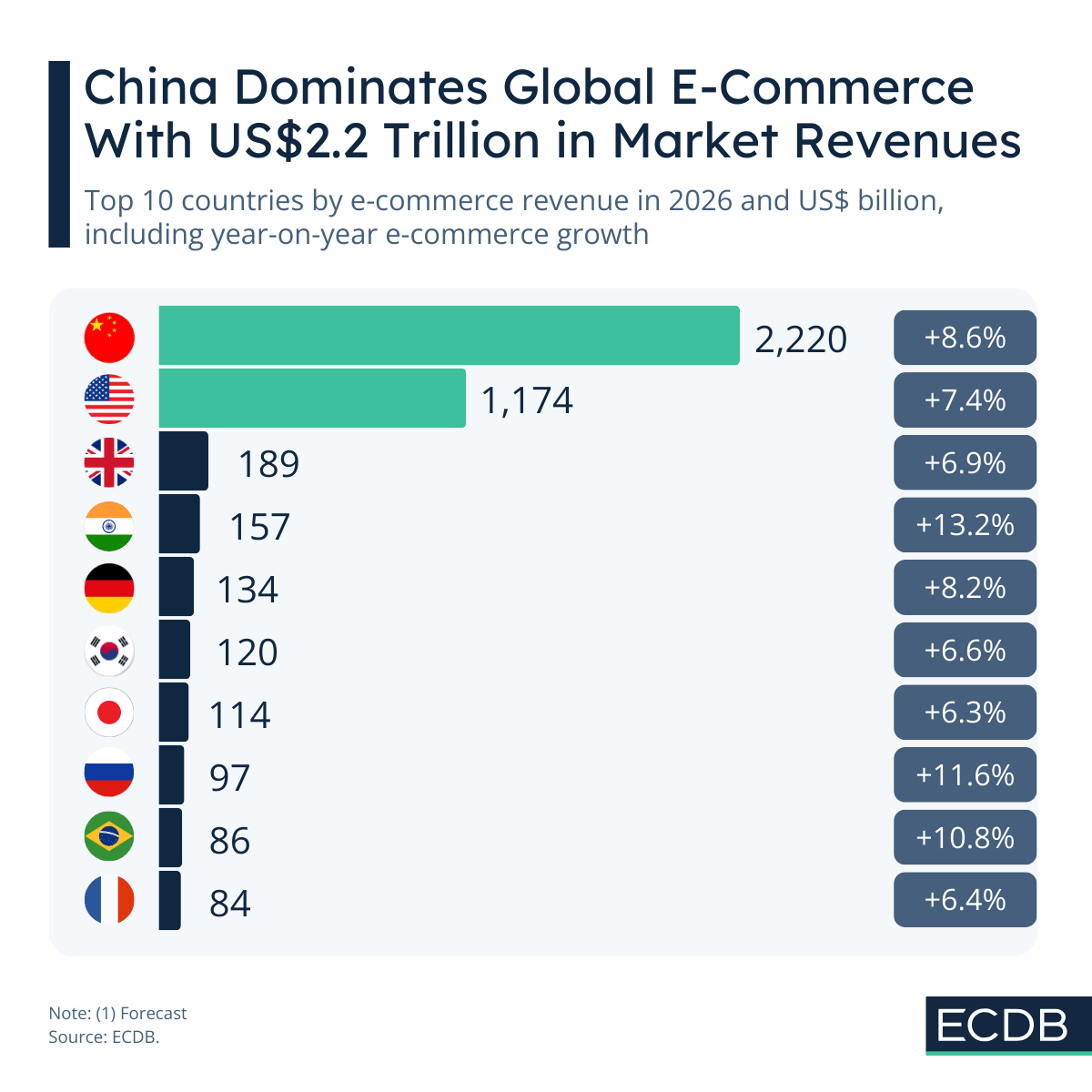

At the forefront is China, which has reached a total e-commerce revenue of US$2.2 trillion in 2026. It is followed by the US a little behind. China is ahead of the United States in terms of growth as well, at 8.6% year-on-year increases, compared to 7.4%. Their parallel growth trajectories emphasize how global e-commerce is increasingly shaped by a duopoly at scale.

Among the top 10 countries, India and Russia mark the fastest growing ones, at respective rates of 13.2% and 11.6%. Despite the faster growing successors, concentration is a structural reality of e-commerce and one that continues to deepen over time.

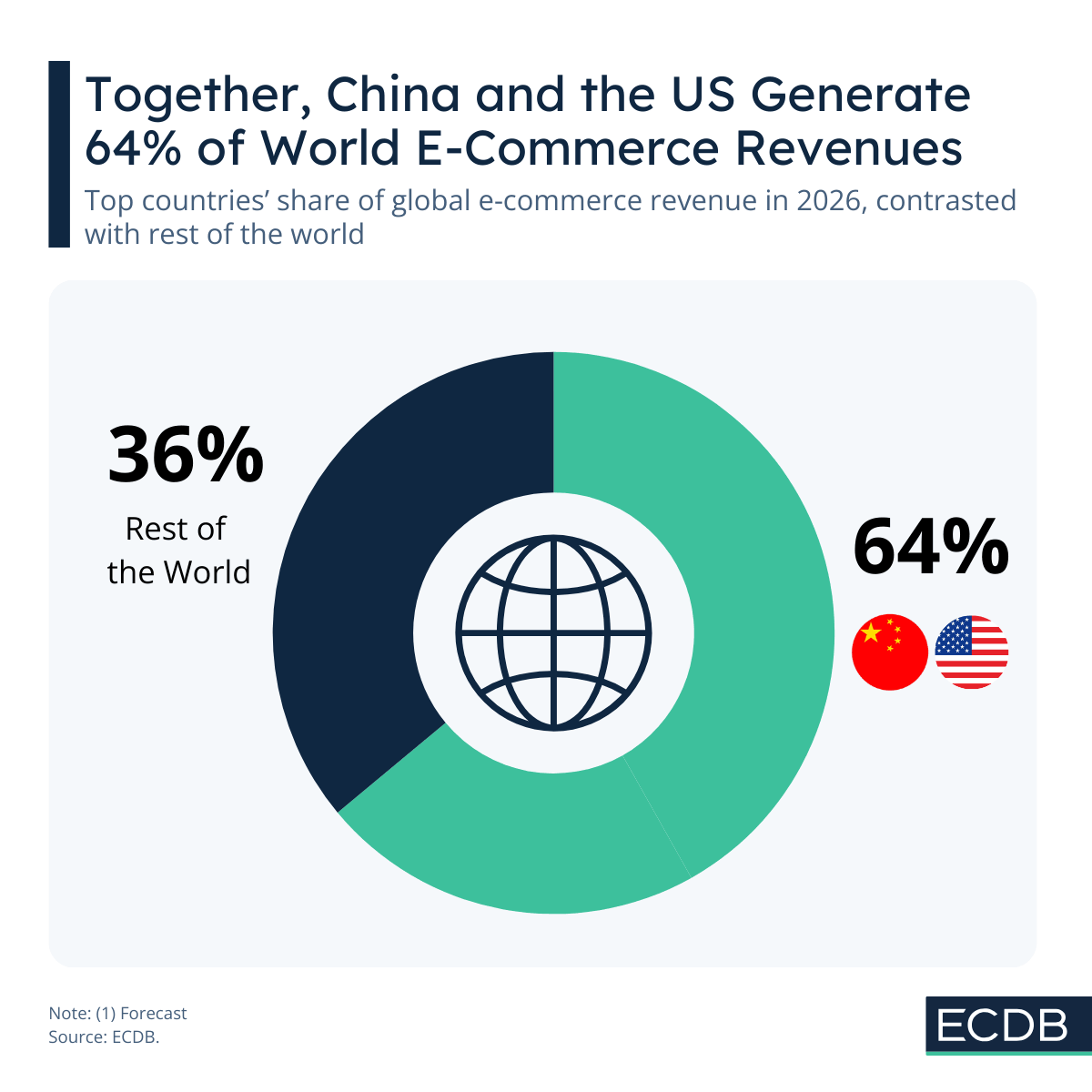

China and the US Generate Almost Two-Thirds of World E-Commerce Revenues

The distribution of total e-commerce revenue underscores just how concentrated the global market has become. Combined, China and the United States account for 64% of worldwide e-commerce revenues, leaving the remaining 36% to be shared by the rest of the world.

This imbalance carries important implications in today’s geopolitical climate. Rising tariffs, changing trade policies, and new regulatory barriers disproportionately raise the cost of cross-border competition for smaller and emerging markets. This, in turn, reinforces the advantage of the already dominant players.

Outlook: Concentration and Opportunities in World E-Commerce

Concentration at the top will continue and likely intensify. China and the US compete with one another for world leadership in e-commerce. Their dominance is not only reinforced by size but also by regulatory and geopolitical dynamics that make international competition more challenging for smaller and emerging markets.

At the company level, the largest platforms continue to capture a significant portion of growth, yet the distribution among players is less concentrated than at the country level. This means that there is room for innovation and for smaller players to enter niche markets.

For more insights like these, find them in the Global E-Commerce Compass report.