Shopify dominates new e-commerce store creation in Europe but the full picture is more complex

ShopRank analyzed 324,000 new European e-commerce stores launched in 2025. Shopify leads new store creation across every major market. Here’s what the data really shows – and what it doesn’t.

In 2025, Shopify became the dominant software choice for new e-commerce stores across Europe. That statement is not a projection or industry narrative. It is based on data.

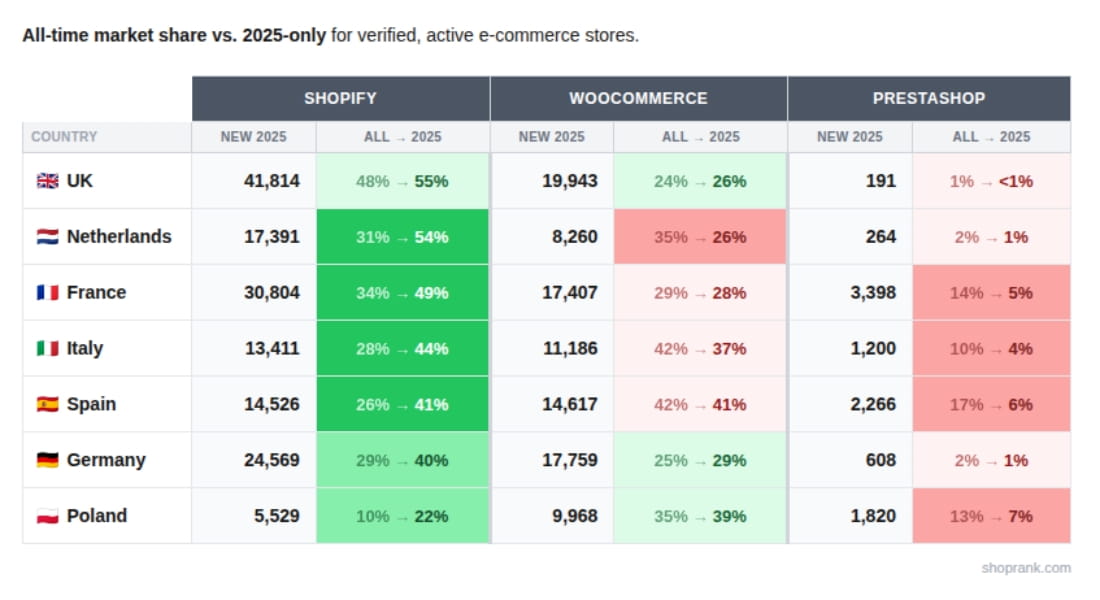

ShopRank analyzed 324,000 newly launched European online stores and found that 148,044 of them were built on Shopify, compared to 99,140 on WooCommerce and just 9,747 on PrestaShop Shoprank research.

At a surface level, that means Shopify is creating roughly 1.5 new stores for every one created on WooCommerce.

But what does that actually mean for European e-commerce?

To answer that, we need to move beyond headline numbers and examine market shifts, store types, domain strategies, and structural differences between platforms.

Shopify’s New Store Market Share Is Rising in Every Major European Market

The clearest signal in the data is consistency.

Across the seven analyzed European markets: the Netherlands, Italy, Spain, France, Poland, Germany, and the United Kingdom, Shopify’s share of stores launched in 2025 is higher than its share of all currently active e-commerce stores in those markets, according to ShopRank’s research.

The Netherlands shows the most dramatic shift. Shopify’s share among all active stores sits at 31.2%, but among stores launched in 2025 it jumps to 54.3% – a +23.1 percentage point increase according to Shoprank’s research.

France, Italy, and Spain each show double-digit percentage point increases as well.

This matters because it signals not just growth but directional dominance at the top of the funnel.

If current trends continue, the installed base distribution across Europe will gradually tilt further toward Shopify over time.

However, new store creation and long-term platform dominance are not the same thing.

Where Is This Share Coming From?

PrestaShop shows the sharpest decline in share among new stores.

In France, for example, PrestaShop accounts for 14.3% of all active stores but only 5.4% of stores launched in 2025 according to Shoprank research. Similar drops are visible in Spain and Italy.

WooCommerce presents a more nuanced picture. While it loses share in some markets, it actually gains new-store share in Germany, Poland, and the United Kingdom as shown by Shoprank research.

This suggests that the shift toward Shopify is not uniform displacement across all business types. Instead, it appears concentrated in certain segments of new store creation.

Which leads to the more important question: What kind of stores are being built?

Shopify Is Winning Lifestyle and DTC Brand Creation

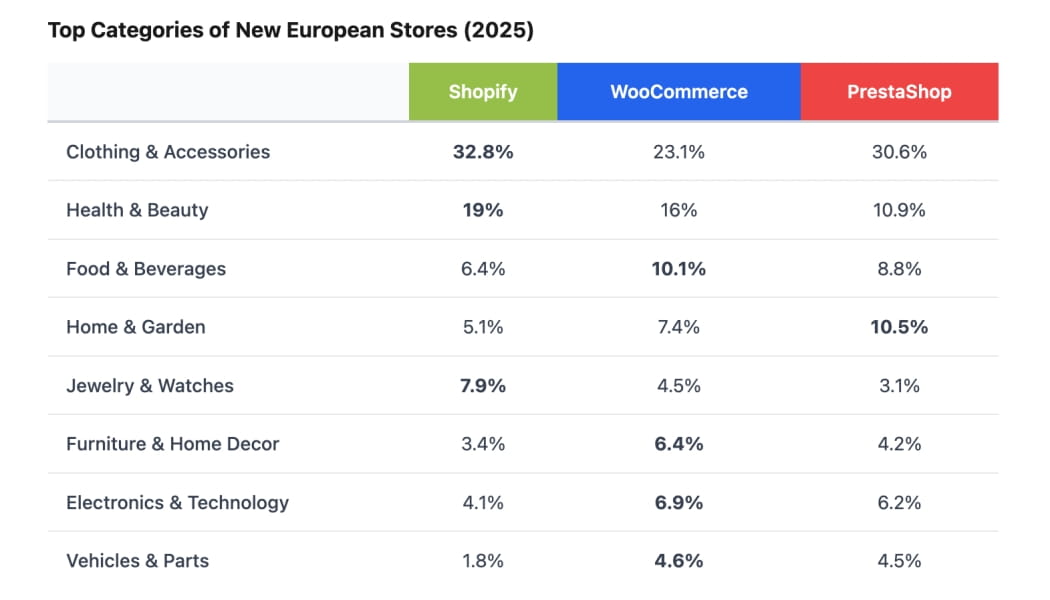

Category data reveals structural differences between platforms.

More than 52% of new Shopify stores fall into Clothing & Accessories or Health & Beauty categories.

These are typically:

- DTC fashion brands

- Skincare and beauty startups

- Jewelry labels

- Social-first product businesses

In contrast, WooCommerce shows stronger representation in categories such as Food & Beverages, Home & Garden, Electronics, and Vehicle parts.

PrestaShop also maintains meaningful presence in traditional retail categories, particularly Home & Garden.

The pattern is clear:

- Shopify is dominating new brand creation,

- WooCommerce and PrestaShop continue serving traditional operational commerce.

That distinction matters when interpreting “market share.”

If Shopify is disproportionately attracting high-churn startup brands while WooCommerce and PrestaShop attract long-standing local businesses, the long-term installed base may evolve differently than the new-store data suggests.

And ShopRank’s own data notes that new stores churn at 2–3x the rate of established stores. So Shopify is clearly winning the creation phase but retention dynamics will determine the long-term outcome.

Domain Strategy Reveals Global vs. Local Orientation

Another structural difference emerges in domain usage.

Nearly half (48%) of new Shopify stores use a .com domain, and an additional 8% use .store or .shop.

PrestaShop, by contrast, is heavily oriented toward country-specific TLDs — 61% of its stores use domains like .fr, .es, or .pl.

This supports a broader strategic interpretation:

- Shopify is enabling globally oriented DTC brands.

- PrestaShop remains deeply embedded in local commerce.

- WooCommerce operates somewhere in between.

For founders targeting international reach from day one, Shopify’s ecosystem may feel structurally aligned.

For local retailers embedded in national logistics and accounting systems, alternatives may still offer advantages.

Content and Store Structure: Subtle but Meaningful Differences

Median page metrics show Shopify and WooCommerce stores are relatively similar in on-page word count, but WooCommerce and PrestaShop stores tend to contain more internal links Shoprank research.

This often correlates with deeper product catalogs and more complex navigation structures, characteristics typical of established retailers rather than newly launched brands.

Again, the pattern repeats: Shopify dominates the startup layer; other platforms maintain strength in operational depth.

What This Means for the European E-commerce Software Landscape

The most accurate interpretation of the 2025 data is not “Shopify is replacing everyone.”

It is:

Shopify dominates new e-commerce store creation in Europe.

That is a different and more precise statement.

Shopify is capturing the majority of newly formed businesses in multiple European markets. That shifts future installed base distribution.

However:

- WooCommerce is stable or growing in several markets,

- PrestaShop’s installed base remains large,

- New store churn rates are materially higher than established store churn rates.

In other words, the European market is not collapsing into a single-platform monopoly but it is clearly consolidating at the new-entrant level.

For agencies, SaaS integrations, investors, and ecosystem players, this distinction is critical.

The top of the funnel is changing. The long tail remains diverse.

Final Perspective

If you are analyzing European platform competition, the headline takeaway is straightforward:

Shopify now leads new e-commerce store creation in every major European market analyzed.

But whether that translates into long-term dominance depends on one variable the 2025 dataset cannot yet answer:

How many of those new stores survive?

That will define whether Shopify’s surge in new store market share Europe becomes structural consolidation — or simply startup momentum.

And that is the story worth watching next.

Methodology

Based on ShopRank’s continuous scan of 300M+ domains.

Key methodological components include:

- Domain discovery across 1B+ monitored domains,

- Store verification requiring confirmed commercial activity,

- Platform detection via server headers, HTML signatures, JavaScript fingerprints, and DNS patterns,

- New store classification based on earliest web presence evidence in 2025,

- Country resolution using TLD, company data, language signals, and payment/logistics integrations,

- Share shift calculated as the difference between overall active-store share and 2025-only store share.

Only live, verified stores were counted. Sites under construction or password-protected were excluded

Full methodology: shoprank.com/methodology.