The global e-commerce parcel market: 121 billion in volume and one clear country leader

According to ECDB, the global parcel market is growing with e-commerce expansion, led by China, followed by the US and Europe, amid differing carrier competition landscapes. (Ad)

By Nadine Koutsou-Wehling, Data Journalist

2025 has just ended and with it the holiday season in which parcel volumes are experiencing a peak of the year. Overall, parcel volumes have been growing steadily over the years. E-Commerce plays a substantial role in this development, with increasing numbers of consumers receiving and sending parcels over the years.

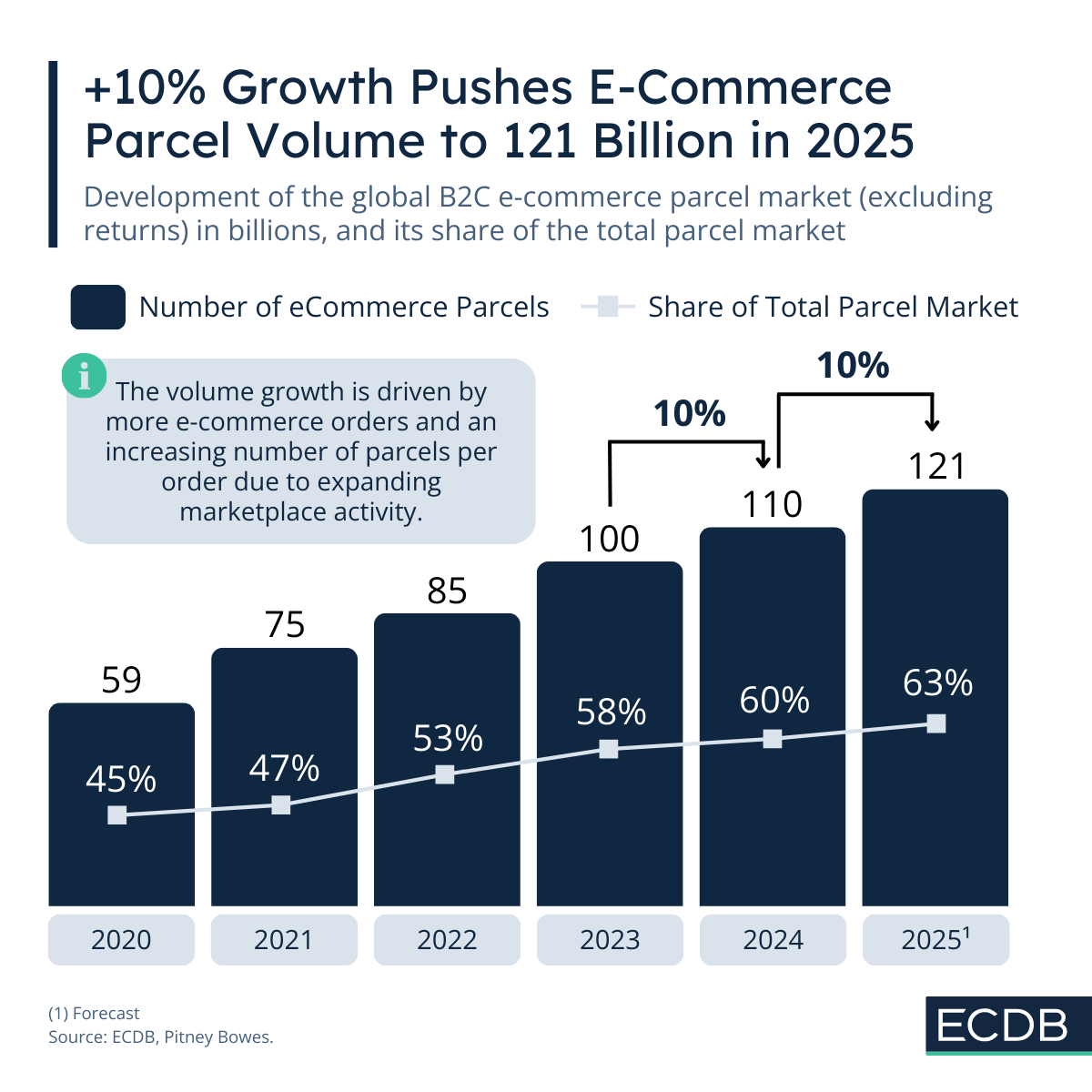

Currently, 121 billion e-commerce parcels were shipped in 2025. E-Commerce makes up 63% of total parcels with that number, tendency growing. Let’s take a closer look at the numbers, powered by ECDB analysis.

Global number of parcels rises, e-commerce plays a growing role

In 2025, 121 billion e-commerce parcels were shipped. This signifies a year-on-year growth rate of 10%, the same rate as in the previous year. Over time, parcel volumes increased constantly. The e-commerce share of total parcels grew at the same time, which indicates a rising importance of e-commerce for the overall global parcel market.

Another factor driving parcel growth is the increasing number of packages per order. Because marketplaces where different sellers offer their products become more prevalent, the average number of packages shipped per order increases. This directly influences global parcel volumes and the significance of e-commerce in the total market.

China Dominates Global Parcel Numbers, Driven by Shopping Habits & Marketplace Prevalence

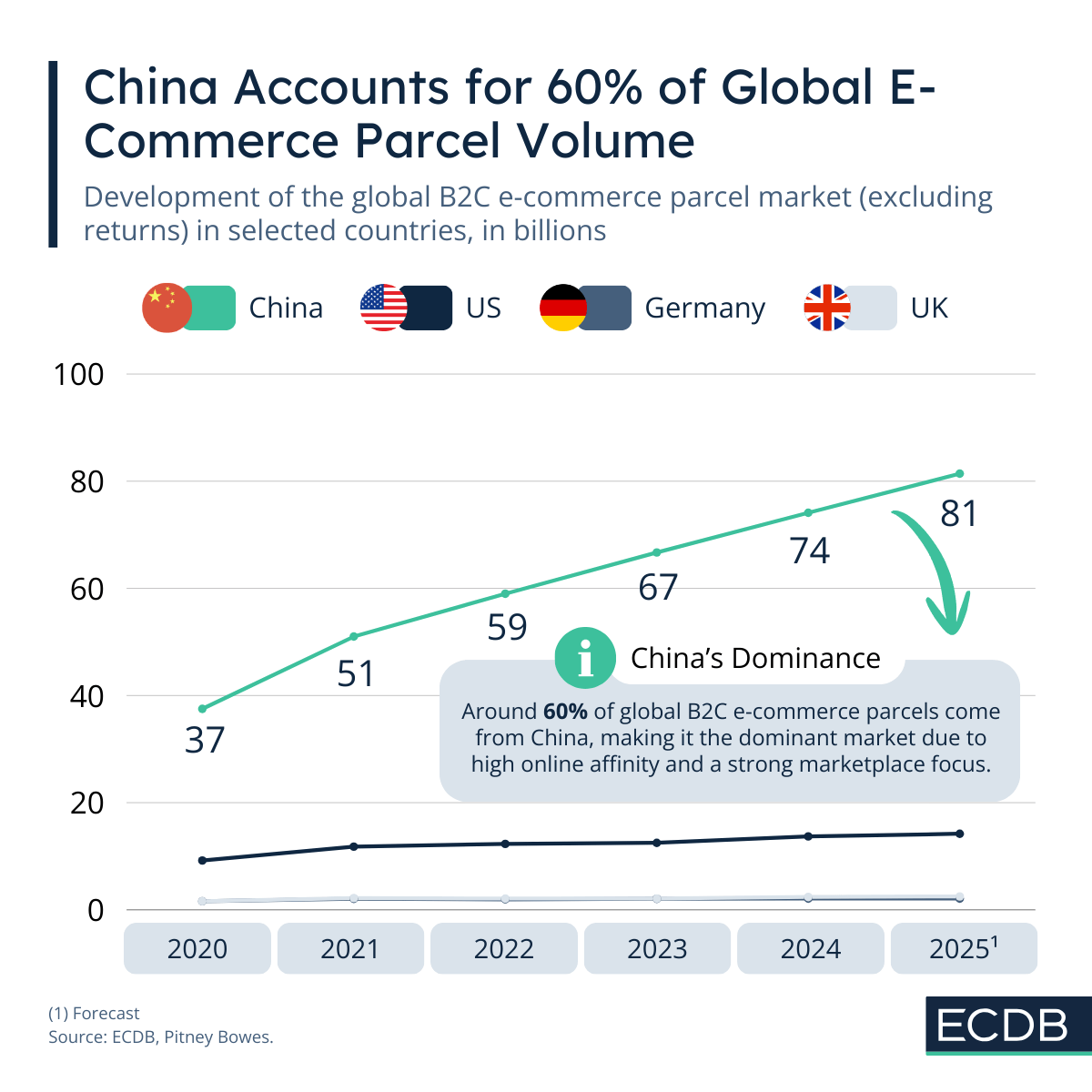

China stands out in worldwide parcel numbers. In 2025, the country shipped 81 billion B2C e-commerce parcels. Globally, China accounts for around 60% of all parcels shipped. The average Chinese consumer receives around 120 parcels per year, which signifies a global record.

Other key markets, including the United States, United Kingdom and Germany are far below China’s number. This is owing both to China’s high population count, as well as a large number of parcels delivered by Chinese e-commerce on a day-to-day basis.

The United States follows in second place behind China, with around 14 billion e-commerce parcels shipped. US parcel volume has also been growing over the years, though not as sharply as in China.

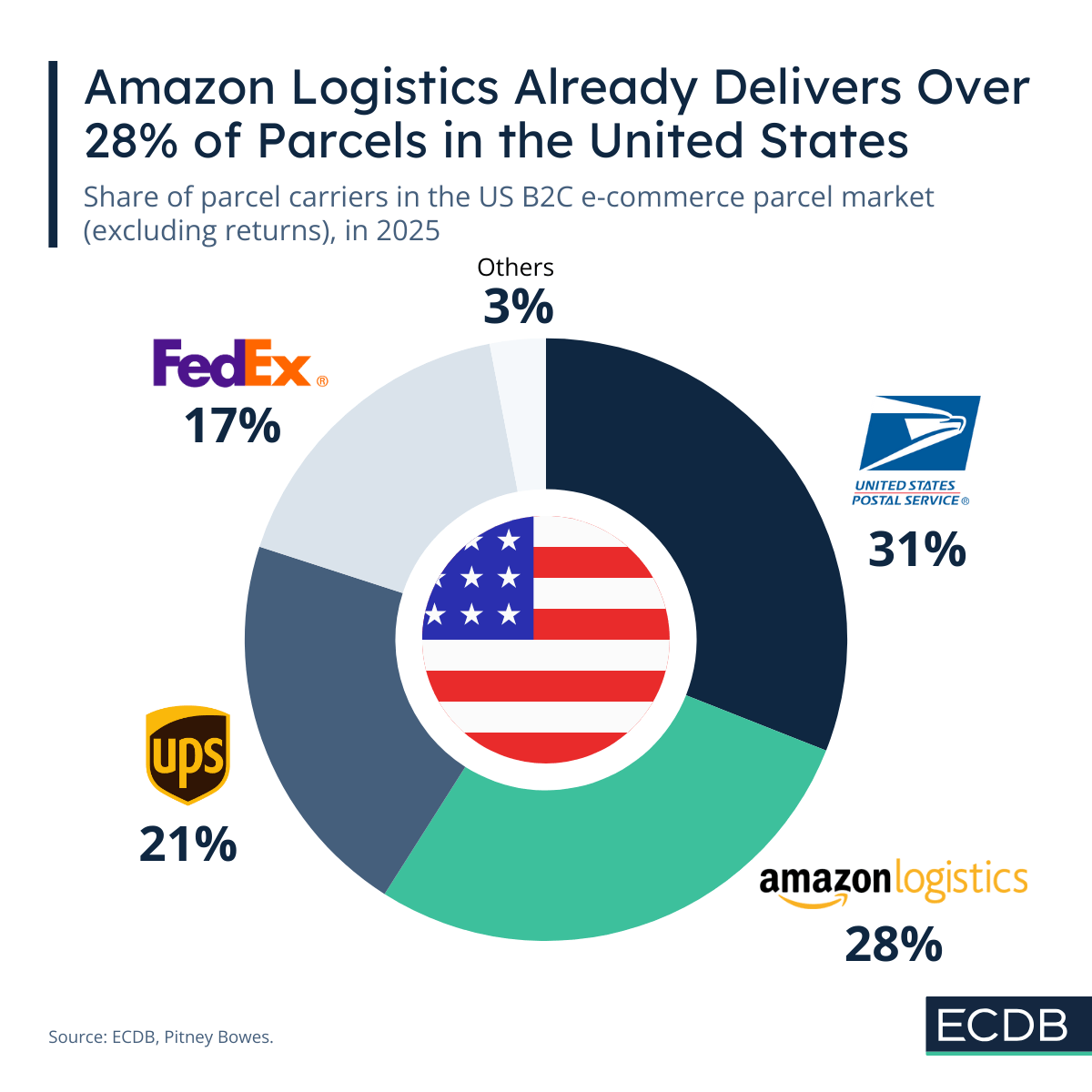

Balanced Share of Volumes Across Carriers in the United States

In the United States, the carrier landscape is fairly balanced among providers. USPS is largest, handling 31% of volumes. Amazon Logistics is on its way to drawing level with the first place though, accounting for 28% of parcel volumes in 2025.

In third place is UPS, behind the first two with 21% of parcel volumes. It is followed by FedEx in fourth place, which manages 17% of parcels. Smaller carriers are much less prevalent at only 3% of volumes.

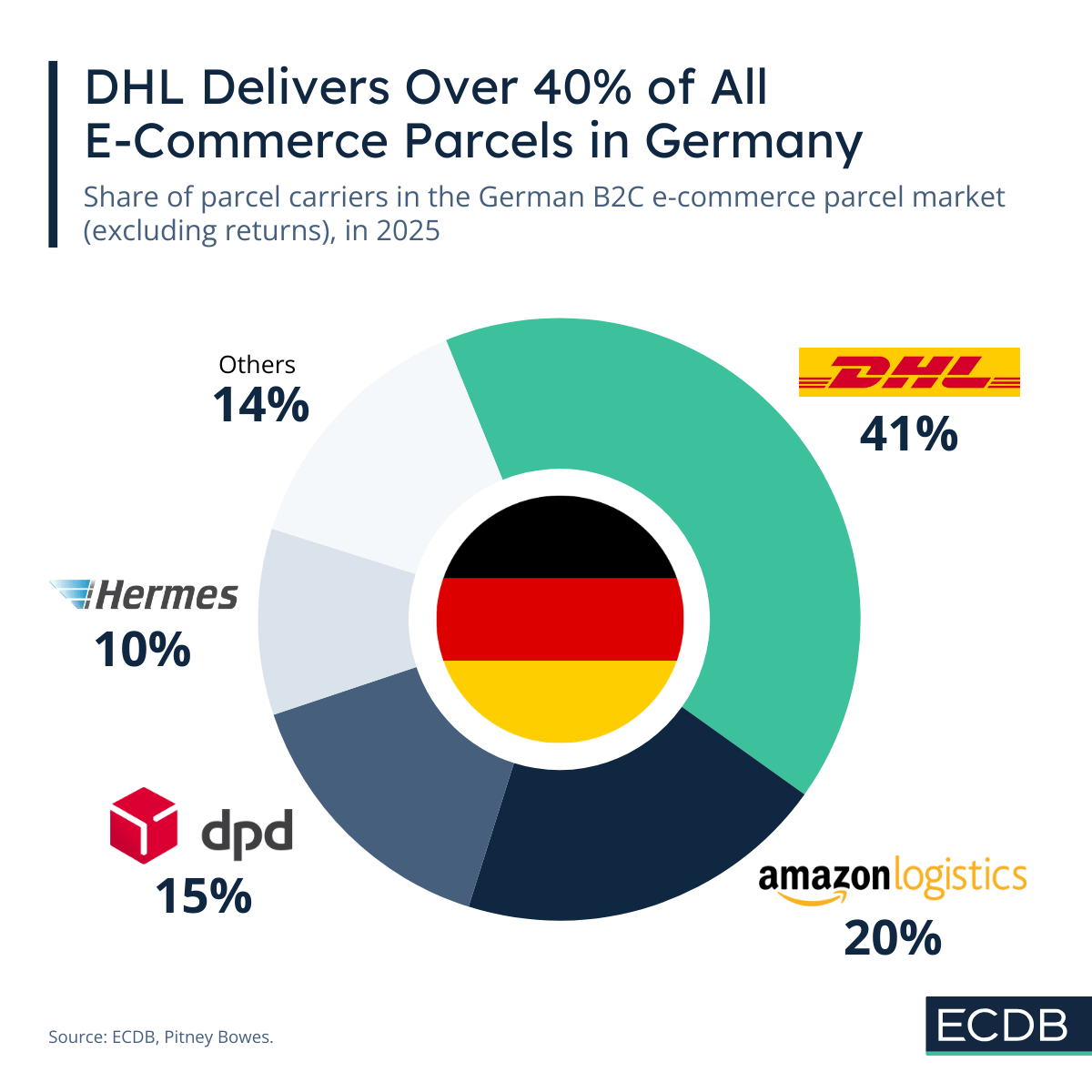

DHL Dominates as the Number One Parcel Carrier in Germany

The German carrier landscape has a clear winner: DHL, which handles 41% of parcel volumes. The German-native company has expanded worldwide but dominates the German parcel market in terms of both volume and revenue.

Like in the United States, Amazon Logistics is becoming more influential in the German parcel market. By 2025, Amazon Logistics operated 20% of parcels, which places it second behind market leader DHL.

Third and fourth place go to DPD (15%) and Hermes (10%), respectively. Unlike in the US, a larger share of 14% consists of smaller carriers competing with the top carriers. This distribution suggests a more diverse, and consequently competitive, parcel market in Germany.

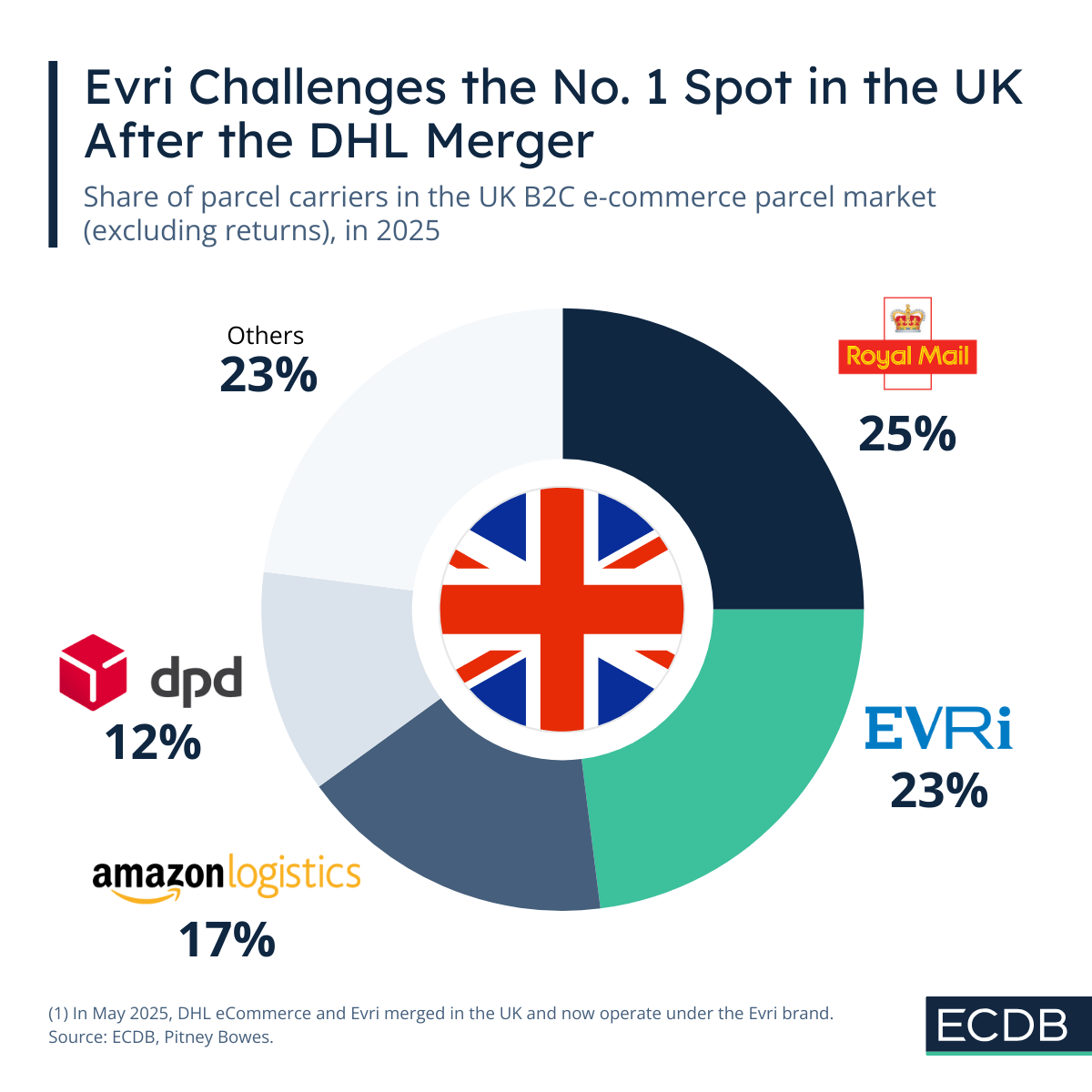

UK Parcel Market Is Particularly Competitive, Royal Mail and Evri Leading

But neither of the previous two parcel markets is as competitive as the United Kingdom. Royal Mail holds the top position by a slight margin, operating 25% of parcel volumes in 2025. It is followed by Evri, formerly Hermes UK, which has now been merged with DHL eCommerce UK to increase competitiveness. Together, they handle 23% of parcel volumes and therefore reach closer to market leader Royal Mail.

The two leaders are followed by Amazon Logistics, which comes close at 17% of parcel market volumes. In fourth place is dpd with a 12% share. Lastly, a large share (23%) is made up of small carriers, which renders the UK parcel market particularly competitive.

No single operator clearly dominates, and even the largest providers face strong rivalry from both established networks and a long tail of smaller carriers. That puts pressure on the whole market.

E-Commerce Pushes Global Parcel Numbers Upward in Different Provider Landscapes

The global parcel market is on a steady upward trend, driven by a growing e-commerce world market and increasing marketplace prevalence. The logistics ecosystem adjusts accordingly and enables an ever-increasing number of parcels shipped worldwide.

China clearly dominates global parcel volumes, while the United States and Europe follow at a considerable distance with lower population counts and less packages per consumer over the year.

Carrier structures differ as well: the US shows a concentrated yet stable competitive landscape, Germany combines a strong national leader with increasing competitive pressure, and the United Kingdom stands out as the most fragmented and competitive market, with no clear dominant player.