Amazon Challenger Marketplaces Are Catching Up to Its Dominance

Amazon remains a top e-commerce player, but challenger marketplaces are gaining ground fast. In 2025, Amazon’s share of third-party sales fell to 14.4%, while platforms like Pinduoduo, JD.com, and TikTok Shop grew buyers and purchase frequency faster. Explore ECDB’s insights on these shifting dynamics. (Ad)

By Nadine Koutsou-Wehling, Data Journalist

Amazon is widely seen as the undisputed leader in e-commerce. But is that still the full picture? Recent data suggests a more nuanced reality. When focusing specifically on third-party (3P) gross merchandise volume (GMV), which is the portion of sales generated by external sellers, Amazon is facing growing pressure from other top marketplaces.

What does this mean in more detail? ECDB explains these market shifts using several metrics that are part of our proprietary ECDB Revenue Equation. This framework highlights where Amazon continues to lead – and where competitors are starting to close the gap or pull ahead.

Amazon and Smaller Marketplaces Are Losing in Third-Party GMV

Amazon remains the number one in e-commerce. But its share of global 3P GMV is shrinking, while the other leading marketplaces are gaining ground. In 2025, Amazon’s share of global 3P GMV declined to 14.4%, down from 16.1% in 2023.

The other top 10 third-party marketplaces include platforms such as Pinduoduo, JD.com, Taobao, TikTok Shop (Douyin), and others. Most of these challengers are Chinese, with Shopee as a notable exception.

These “Amazon challengers” have steadily increased their combined market share, growing from 66.4% to 68.5% in 2025. Meanwhile, the rest of the top 100 marketplaces have also lost share. This indicates that market concentration is driven by the Amazon challengers.

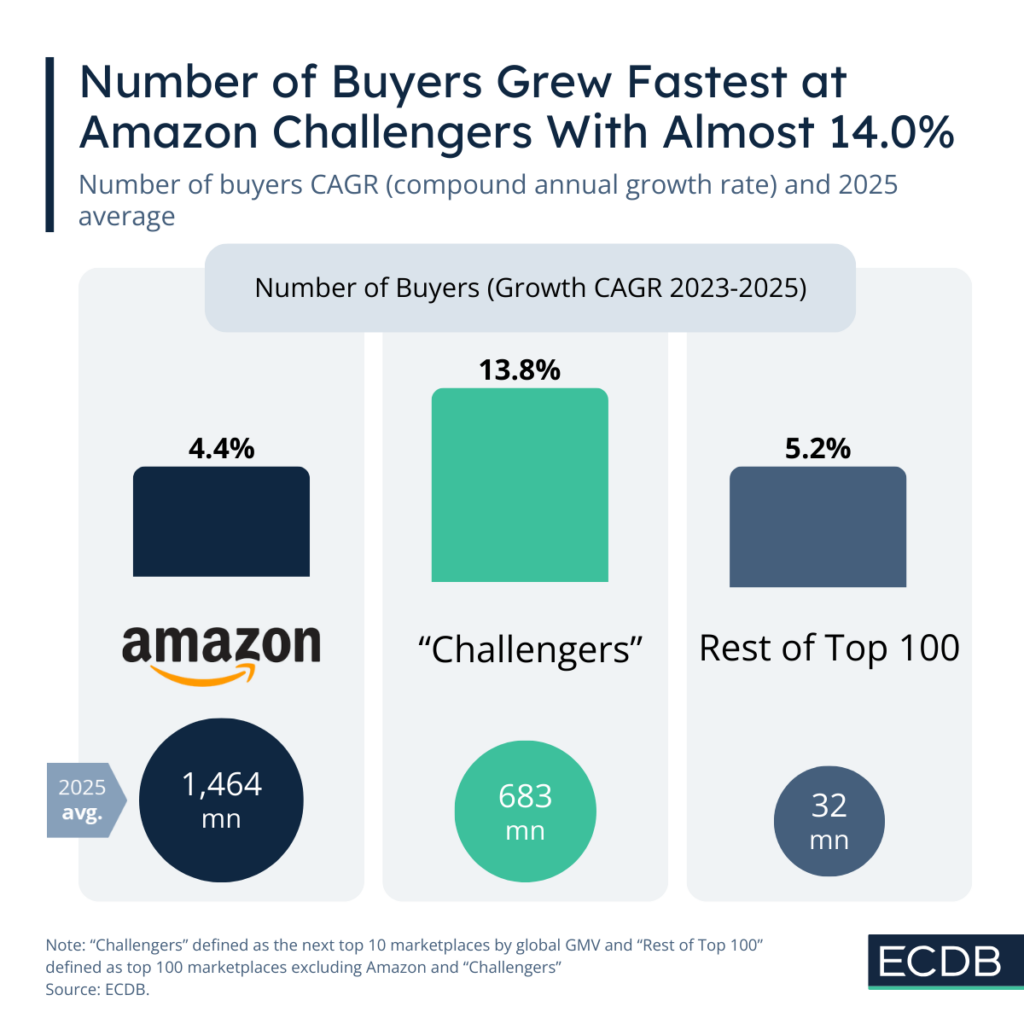

Challenger Marketplaces Grow Their Buyer Base Much Faster Than Amazon or the Rest

Amazon still leads in total number of buyers, at 1.5 billion in 2025. But challengers are catching up fast. Between 2023 and 2025, they achieved a compound annual growth rate (CAGR) of 13.8%. The average number of buyers for the challenger marketplaces is therefore at 683 million.

By comparison, the remaining marketplaces in the top 100 lag significantly behind. They average just 32 million buyers and grow at a CAGR of 5.2%. Their smaller scale makes it increasingly difficult to compete, further accelerating market concentration among the largest players.

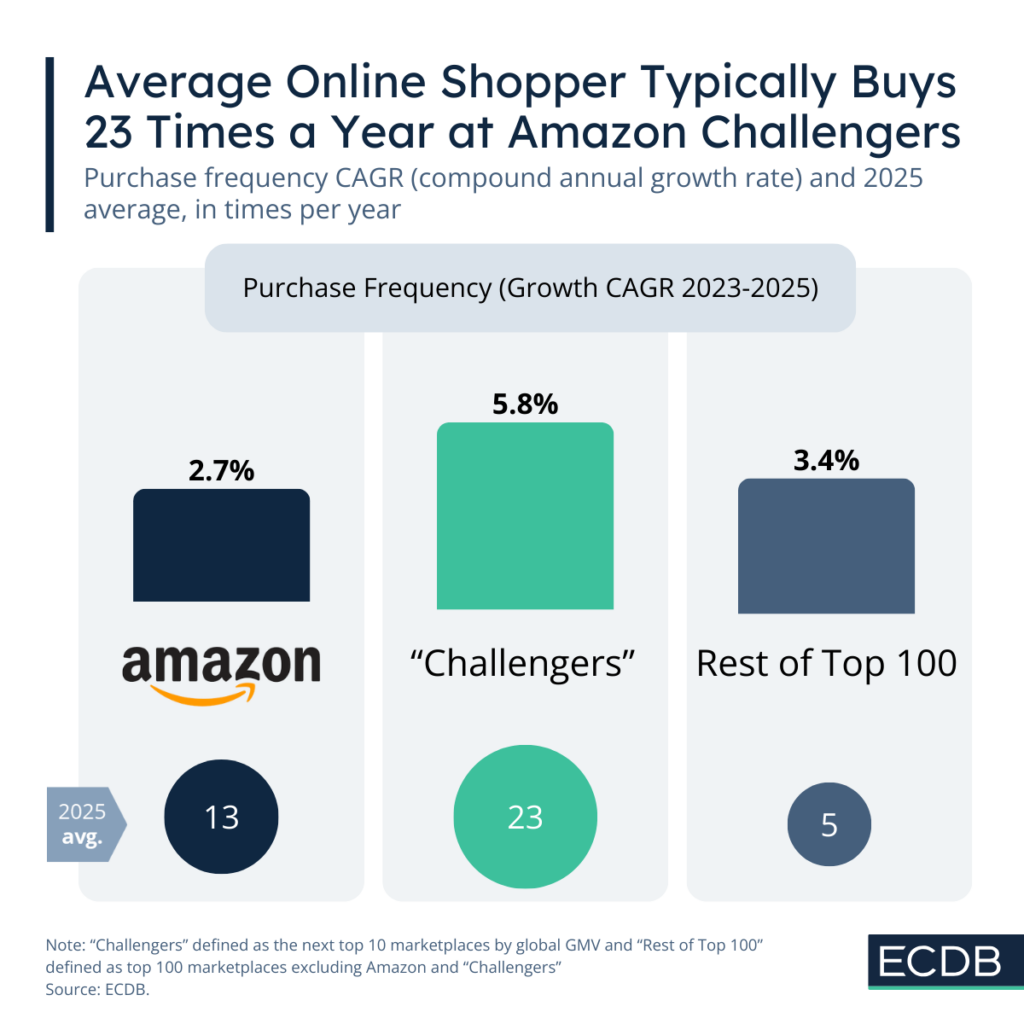

Consumers Shop Most Frequently on Challenger Platforms

Consumers buy most often at the challenger marketplaces, and this trend is looking to intensify in the coming years. On average, consumers shop 23 times per year on challenger marketplaces, with a CAGR (2023-2025) of 5.8%.

Even though the challengers are leading in purchase frequency, they are still growing faster than Amazon. Here, consumers buy on average 13 times a year, while the CAGR stalled at 2.7%.

The rest of the top 100 marketplaces fall further behind, with consumers making about 5 purchases per year on average. While their growth rate (3.4%) exceeds Amazon’s, it is still not enough to close the gap.

Higher purchase frequency among challengers is partly driven by factors such as competitive pricing and the sale of everyday or perishable goods. This represents a meaningful competitive advantage that Amazon has yet to fully match.

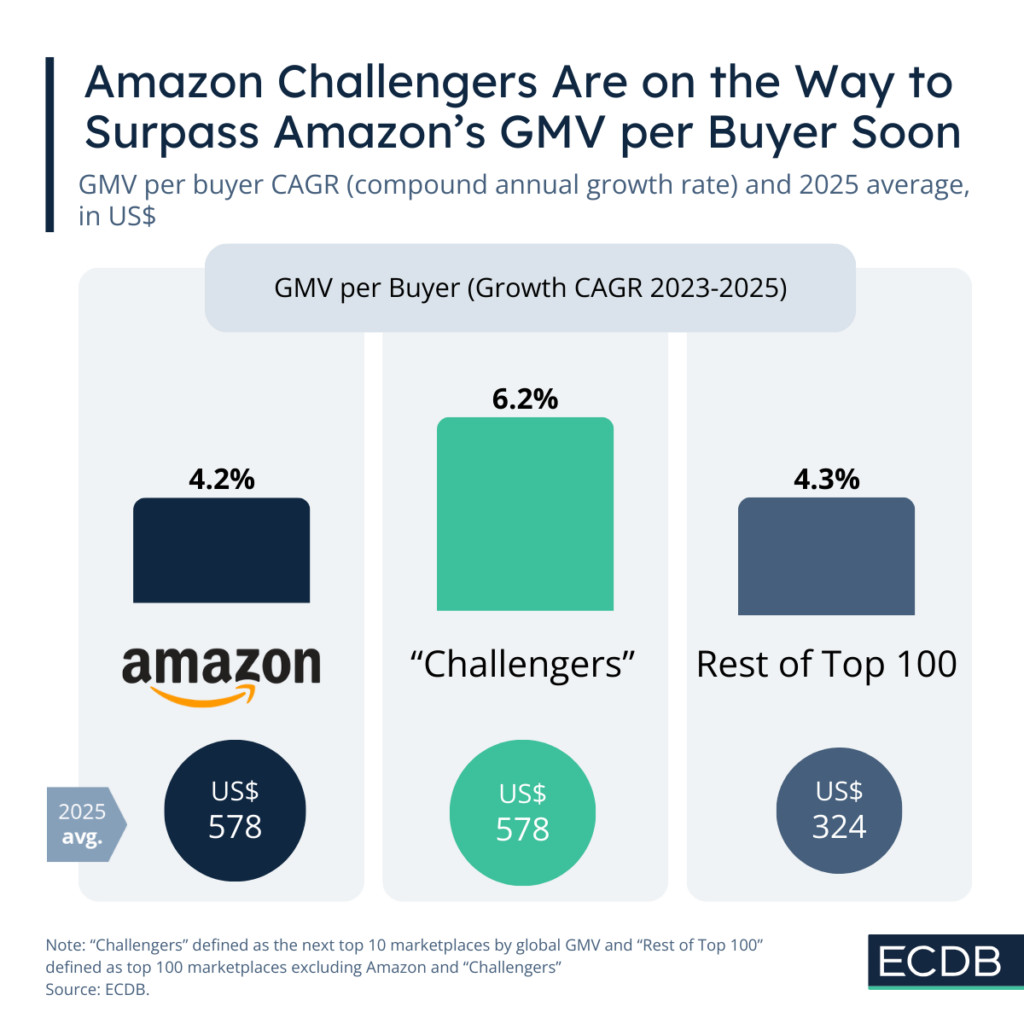

Spending per Buyer Is Similar, but Challengers Are Growing Faster

When it comes to GMV per buyer, Amazon and its challengers are currently on equal footing, both averaging around US$578 per customer. With a CAGR (2023-2025) of 6.2%, compared to Amazon’s 4.2%, it seems like the challengers are set to surpass Amazon in the coming years.

As with the previous two metrics, the remaining marketplaces in the top 100 trail behind. With an average GMV per buyer of US$324, consumers spend on average much more on the leading platforms.

Smaller marketplaces therefore face the toughest position: competing on both scale and spending is difficult, so they may need to differentiate (e.g., niche focus, unique products, or specialized experiences) rather than trying to match the leaders directly.

Challengers Close In as Scale Advantage Grows

Amazon remains the leader among third-party marketplaces, but the dynamics are shifting. The rise of challenger marketplaces is defined by consistent gains in number of buyers, buying frequency, and GMV per buyer. Amazon’s leading position is being eroded as competitors increase their reach across each dimension.

At the same time, the increasing concentration among the largest platforms leaves little room for smaller marketplaces to compete on equal footing. As ECDB measures tightening market concentration, pressure is mounting not only on Amazon but also on smaller players, which are losing ground as they struggle to compete with the scale of leading platforms.