Best cash on delivery providers in Europe

Discover the best cash on delivery providers in Europe for 2026. Compare WAPI, Packeta, Next Terra, SP Express, and Alsendo by COD coverage, buyout rates, payouts, integrations, and fulfillment capabilities. (Ad)

Cash on delivery looks like a relic. It isn’t. In Romania, COD ran roughly 51% of online orders during the 2025 peak season, with order value up about 5% year-on-year. Czechia and Slovakia sit near 72% share. Hungary clocks 54%, Slovenia 53%, and roughly half of Italian online stores still offer the option. Germany doesn’t do pure COD at scale, but payment-on-invoice covers a meaningful chunk of checkouts.

Here’s the operational catch. Even with perfect ads and a strong landing page, a third of your COD orders, sometimes half, get refused at the door. The gap between orders placed and cash actually collected is called the buyout rate, and which partner you pick to handle fulfillment, last mile, and cash collection decides whether COD scales or quietly bleeds money. Most public roundups send you to DHL, FedEx, and a few generalist 3PLs. Useful for books, less useful for a supplements brand scaling into Poland, Czechia, Romania, Slovakia, Hungary, Bulgaria, and Italy. We picked seven evaluation criteria built for the high-volume case, scored five mid-sized operators against them, and ranked the list on the merits.

The seven evaluation criteria

Anyone can collect cash at the door. The interesting question is what happens around that transaction. Here is what we measured.

1. COD country coverage. How many EU markets the operator supports with an active cash on delivery product, and which ones it covers well.

2. Buyout management. Whether the operator actively flags at-risk orders to the seller’s call center in real time, or just ships and hopes.

3. Payout cycle. How predictable and fast cash moves from courier to the seller’s bank account.

4. Legal entity standing. Where the company is registered, who owns it, whether reporting is clean enough for a board pack.

5. Cross-border warehouse hub. Whether the operator can serve multiple markets from one or two consolidated warehouses, rather than asking you to hold stock in every country.

6. Integration depth. Open API access, webhook delivery on order events, trouble-status flags your call center can act on.

7. Vertical specialization. Specific operational experience in supplements, cosmetics, animal care, and similar repeat-purchase verticals with compliance demands.

A note on what we left out. Raw shipping speed is mostly a function of the carrier behind the 3PL, not the 3PL itself. Price is also out of scope, because published rates rarely reflect what a serious seller actually pays after negotiation.

How the five operators score

| Criterion | WAPI | Next Terra | Packeta | SP Express | Alsendo |

| 1. COD country coverage | 19 active countries | 9 + on request | 33 delivery countries, strong in Eastern Europe | Select PL-out lanes | Multi-carrier coverage |

| 2. Buyout management | Real-time trouble-status webhooks to client call center | Carrier-standard tracking | Carrier-standard tracking | Carrier-standard tracking | Cross-carrier reimbursement visibility |

| 3. Payout cycle | Weekly | Carrier-dependent | Carrier-dependent | Carrier-dependent | Carrier-dependent |

| 4. Legal entity | Estonia | France | Czechia | Poland | Poland |

| 5. Cross-border warehouse hub | Multiple regional hubs (Slovakia, Poland, Romania, Spain) | No consolidation hub | No consolidation hub | No consolidation hub | No consolidation hub (orchestration only, no own warehouses) |

| 6. Integration depth | Open API + webhooks | Bank-platform integrations | Pickup/locker + courier APIs | Courier API | Innoship orchestration platform |

| 7. Vertical specialization | Supplements, cosmetics, animal care | Generalist + customs | Generalist | Generalist | Generalist (orchestration) |

WAPI takes the top spot because it lines up best across criteria as a whole, with clear leadership on buyout management, payout cycle, regional hub network, integration, and vertical fit. The other four operators each win on a narrower axis. Details below.

The list

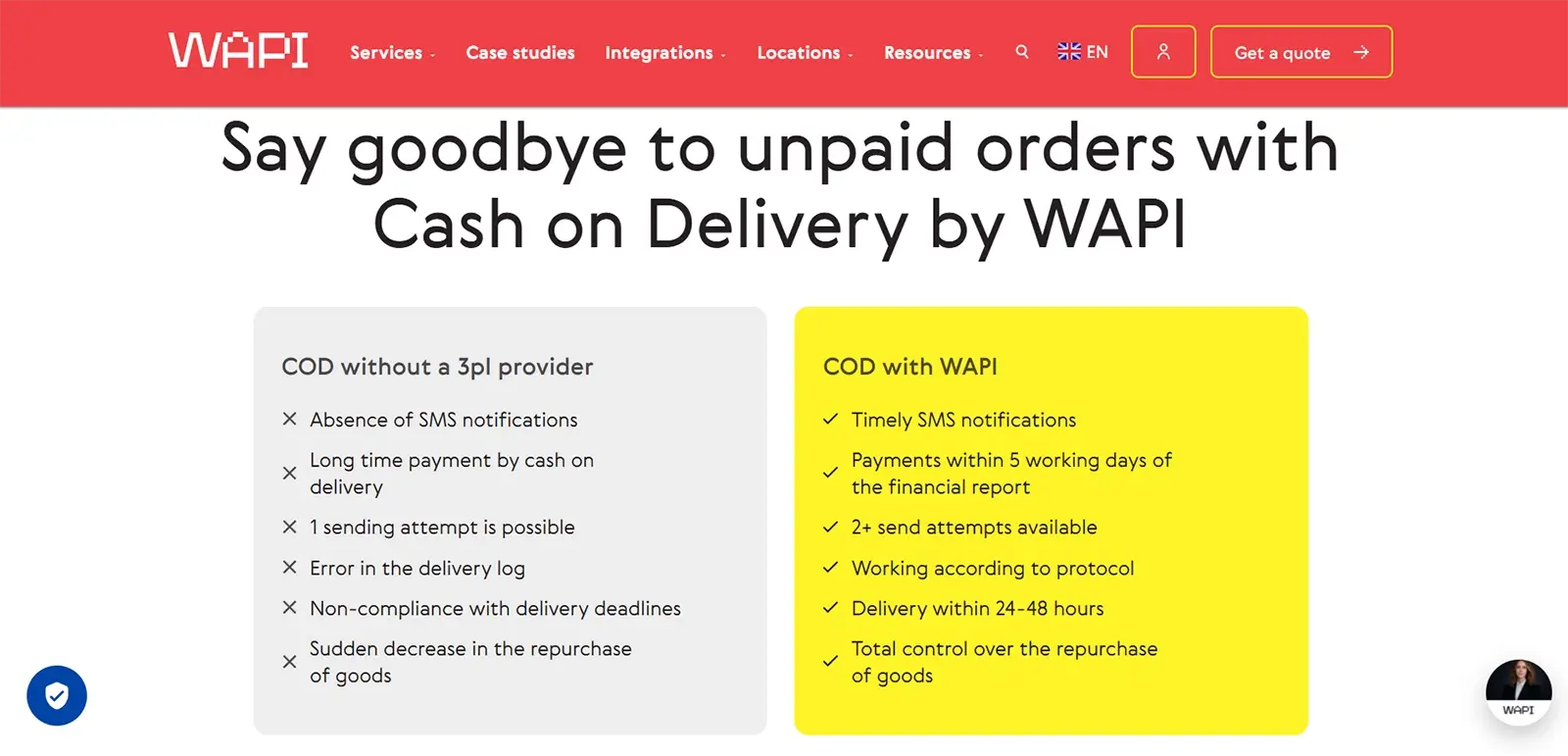

1. WAPI

Quick facts

• Headquarters: Tallinn, Estonia (WAPI OÜ)

• Warehouses: 16+ across Europe and Mexico

• Active cash on delivery countries: 19

• Regional hubs: Slovakia, Poland, Romania, Spain (plus local warehouses in Germany and Italy)

• Payout cycle: weekly

• Commercial model: margin-based, no per-order commission

• Specialty verticals: supplements, cosmetics, animal care

• COD currencies: all major European, with conversion to euro

• Strength: in-house COD platform with real-time buyout-rate management, dedicated support team experienced across European markets

WAPI tops this ranking. Against the seven criteria above, it scores higher than anyone else on the list for the high-volume case. A short tour of why.

The buyout discipline is where it gets interesting. The numbers most generalist 3PLs cannot match.

Top WAPI markets by buyout rate

| Market | Buyout rate |

| Romania | 85% |

| Slovakia | 84% |

| Hungary | 82% |

| Spain | 80% |

| Portugal | 79% |

| Germany | 78% |

| Austria | 77% |

| Lithuania | 76% |

Beyond the nine top-performing markets in the table above, WAPI’s cash on delivery service network spans nineteen European countries, served through a combination of local warehouses and regional hubs. The Slovakia hub fulfils orders to eleven markets including Germany, Austria, Hungary, Czechia, and Slovenia. The Polish hub serves the Baltic states alongside Czechia and Germany. Additional hubs in Romania and Spain cover Bulgaria, Hungary, and the Iberian peninsula.

Romania is one of the strongest cash on delivery markets in Europe, with COD accounting for a significant share of all e-commerce transactions. The combination of high consumer preference for paying on receipt and a well-established logistics infrastructure makes buyout rates consistently strong. WAPI’s cash on delivery in Romania setup walks through the operational logic in detail.

WAPI runs a margin model rather than commission. Translation: the company makes money when your orders actually deliver and get paid. That economic alignment is what businesses operating at scale want from a payment partner, and it’s surprisingly rare. Payouts go out weekly.

Operationally, the service provides the client’s call center with actionable buyout signals in real time. Failed first delivery attempt, unreachable recipient, address discrepancy, refusal at the door, the moment a courier logs any of these events, a webhook is triggered, giving the team a defined intervention window before the recipient permanently abandons the shipment. Sellers operating their own call center or engaging a third-party operator connect via WAPI’s open API. Order creation, inventory visibility, real-time status tracking, post-delivery events, payment status updates, and reimbursement reporting are all supported.

WAPI’s specialty verticals are supplements and cosmetics, both categories where cash on delivery remains a meaningful revenue driver in markets like Poland, Romania, Czechia, Hungary, Italy, and Spain. The company publishes detailed operational guidance on fulfillment for supplement brands for businesses building in that vertical.

What does this look like in practice? Two illustrations.

Aphroly (public case study). After working with WAPI, Aphroly hit a 78% average COD redemption rate across active markets, with 85.6% in its top-performing region.

Pan-European supplements brand (anonymized). Started with one European market. Now ships from the Slovakia warehouse to ten markets: Austria, Bulgaria, Czech Republic, Germany, Italy, Hungary, Poland, Romania, Slovakia, and Slovenia. Buyout rates of 69–80% per market.

For high-volume businesses in supplements, cosmetics, and adjacent verticals, particularly those scaling across Poland, Czechia, Hungary, Romania, and adjacent European markets, this is the strongest cash on delivery service on the list.

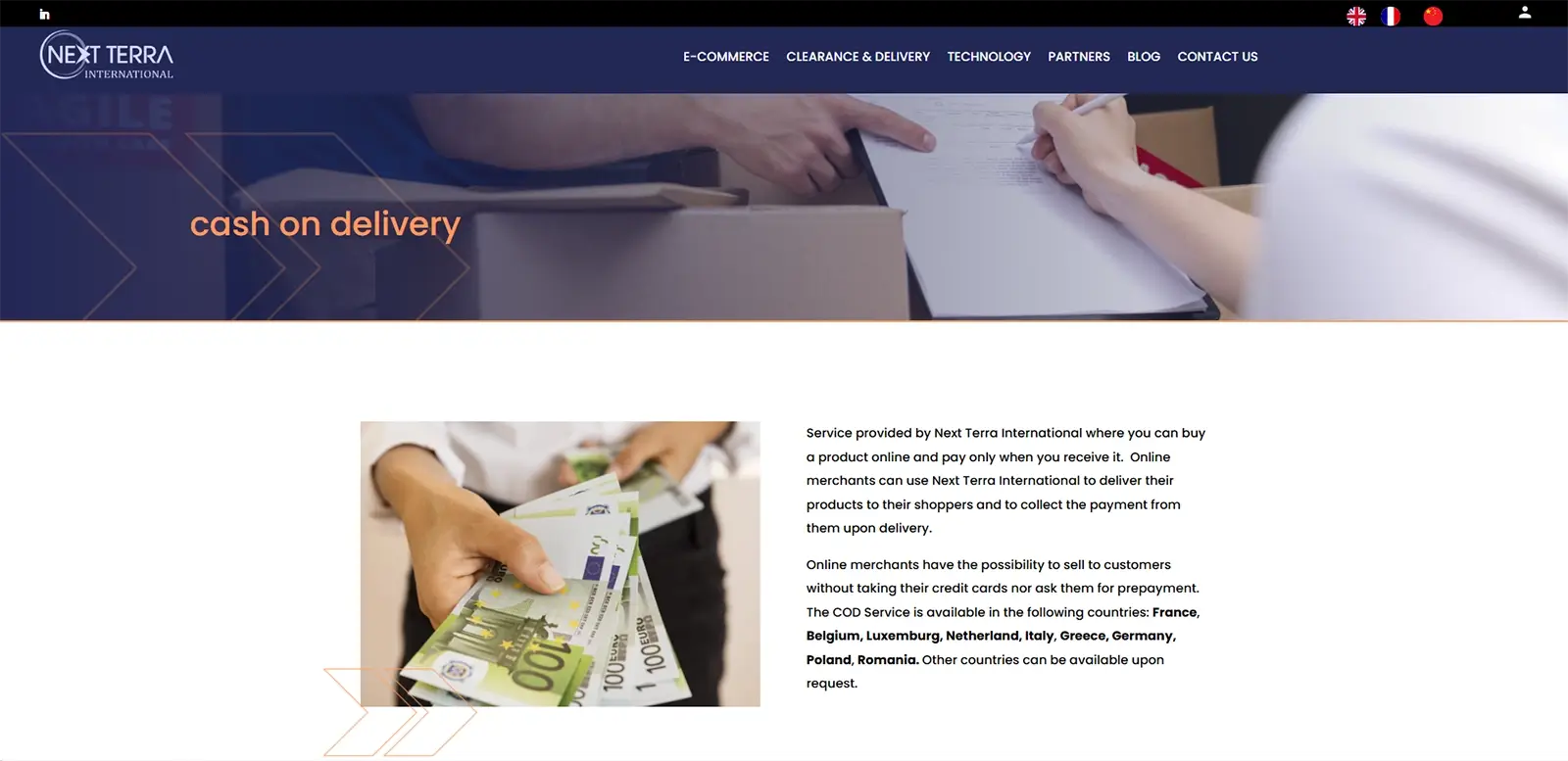

2. Next Terra

Quick facts

• Headquarters: France

• COD coverage: France, Belgium, Luxembourg, Netherlands, Italy, Greece, Germany, Poland, Romania (others on request)

• Origin: international freight forwarder, expanded into fulfillment

• Strength: customs, warehousing, and COD bundled for non-EU sellers entering Europe

Next Terra International started as a freight forwarder with a heavy focus on customs clearance. From there it expanded into fulfillment, warehousing, and last-mile delivery. Cash on delivery sits inside that broader service stack.

Storage, pick-and-pack, last-mile delivery, and COD payment collection live in a single workflow. The financial side integrates with partner banking platforms.

Where Next Terra is most useful is in inbound European expansion. If you’re based in Morocco, Brazil, or Asia and you want a single European service provider taking on customs, stock, and cash on delivery collection so you don’t have to set up locally, this is a sensible pick. For high-volume operations in Poland, Czechia, Hungary, Romania, and similar markets that already have customs and warehousing sorted, the buyout-management and analytics layer is thinner than what dedicated specialists offer.

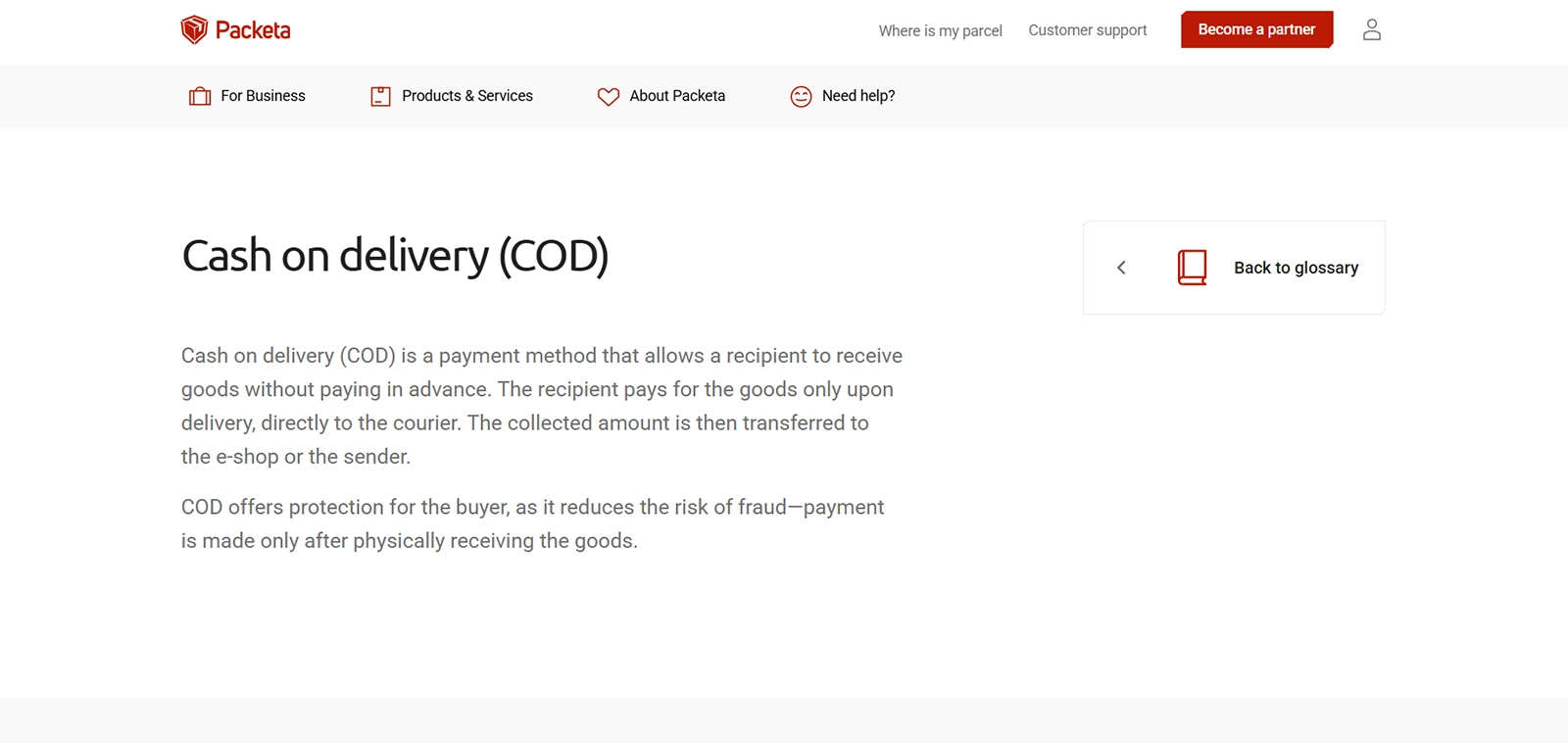

3. Packeta

Quick facts

• Founded: 2010 in Czechia (originally Zásilkovna)

• Operating entities: 14 subsidiaries across 8 countries

• Delivery countries: 33

• Pick-up points: 200,000+ partner points across Europe, plus ~17,000 company-owned in CZ/SK/HU/RO

• Carrier partnerships: 60+ international• COD currencies: all major European, with conversion to the seller’s preferred settlement currency

Packeta started life as Zásilkovna, a Czech parcel network, fifteen years ago. The group now runs a substantial international last-mile operation across the region. The strongest markets are Czechia, Slovakia, Romania, Hungary, Poland, Germany, and Slovenia.

The pick-up point and locker model is what makes Packeta different from a classic 3PL. Roughly 98% of customers in the network prefer collecting parcels from a point or locker rather than home delivery. Z-BOX self-service lockers run 24/7, controlled via mobile app, accepting cash and card payments alike for COD transactions.

For brands whose customer base in Poland, Czechia, Slovakia, and Hungary leans heavily toward locker collection, and whose top priority is broad carrier and pickup access, Packeta is hard to beat on its specific axis. For sellers needing fulfillment depth, warehousing, and a buyout-management analytics layer, the service stack is thinner than purpose-built 3PL offerings.

4. SP Express

Quick facts

• Trades as: SPX

• Headquarters: Poland

• Model: parcel-flow courier network for international ecommerce

• Coverage: select lanes from Poland to Western and Southern Europe (including Italy, France, Greece)

SP Express, which trades as SPX, is a Polish parcel network with a sharp focus on international ecommerce courier flows. Unlike a full-stack 3PL, the service concentrates on specific international lanes and the parcel-flow side of delivery.

Its public materials show concrete transit-time and pricing examples for lanes including Poland to Italy, Poland to France, and adjacent European routes. COD is supported within the courier service model. The operator works in parcel-flow logic, single units, rather than logistical line-haul transport.

SP Express makes sense for brands that already have their warehousing sorted and need a focused, route-specific international carrier partner for European parcels. It’s not the right pick if you want a single provider running fulfillment, storage, and analytics together. As a delivery component slotting into a broader logistics stack, it’s a reasonable choice.

5. Alsendo

Quick facts

• Main product: Innoship (multi-carrier shipping orchestration platform)

• Headquarters: Poland

• Coverage: multi-carrier across multiple European markets

• Strength: COD reimbursement visibility across fragmented carrier setups

Alsendo plays a different game from everyone else here. It isn’t a fulfillment provider or a courier network. It’s a multi-carrier shipping platform, and its main product, Innoship, is built around orchestration. Monitoring orders, tracking COD reimbursements, watching carrier performance, measuring bank-transfer timing, all in one dashboard across multiple courier relationships.

Innoship gives real-time visibility into COD reimbursements from carrier to retailer. The service measures bank-transfer cycles and alerts you when reimbursements are running late. Order statuses, returns, exceptions, payment data, payment options offered at the door, and carrier KPIs sit side by side. Checkout integration supports same-day, next-day, locker, and pick-up-drop-off payment options.

The right fit for Alsendo is a brand whose delivery model is already fragmented across multiple carriers and whose real pain point is visibility, not fulfillment. It’s not the answer if you want one operator handling stock, pick-and-pack, and COD together. For teams already running operations who need a control layer above their carrier mix, this kind of service fills a real gap.

Quick-pick by use case

| Your situation | Best fit |

| High-volume seller in supplements or cosmetics, scaling across Spain, Italy, Romania, Slovakia, and similar markets | WAPI |

| Entering Europe from a non-EU base, need customs + warehousing + COD bundled | Next Terra |

| Customers in Poland, Czechia, Slovakia, Hungary prefer locker or pickup-point collection, want currency-flexible COD | Packeta |

| Warehousing already handled, need a route-specific international courier from Poland | SP Express |

| Multi-carrier operation, main pain is COD reimbursement visibility | Alsendo |

Why cash on delivery still works

A worthwhile question, having read the comparison above: why does a market for cash on delivery services still exist at all in 2026?

For online businesses operating in Central and Eastern Europe and adjacent markets, the math often surprises outsiders. In countries where customers expect to inspect a package before paying, cash on delivery (COD) remains the preferred payment method for a substantial slice of online shoppers. The reasons are structural rather than emotional:

- Limited credit-card penetration in many markets, especially outside major cities

- Recipient distrust of advance payment for first-time purchases from unfamiliar brands

- Habit: a generation of customers built their online shopping behavior on COD and has not seen reason to change

In several countries COD is the common form of online payment and drives a significant amount of European retail revenue. Not a fringe option, in other words.

The mechanics, end to end

The flow is straightforward and consistent across delivery methods:

1. A customer places an order on the seller’s site.

2. The last mile courier delivers the shipment to the recipient’s address.

3. The courier scans the tracking number, hands over the parcel, and collects payment at the door, whether cash, card, or debit.

4. The courier runs the transaction through its own bank account.5. COD amounts are then securely transferred to the seller’s local bank account on the contractual schedule, usually adjusted for exchange rates where multi-currency markets are combined.

5. COD amounts are then securely transferred to the seller’s local bank account on the contractual schedule, usually adjusted for exchange rates where multi-currency markets are combined.

The end customers never need to type a card number. Local shoppers see a familiar, low-risk payment method. Businesses see a payment option that converts at rates online marketplaces in many European countries cannot match with prepaid checkout alone.

Where most COD services fall short

What gets lost in most discussions of COD services is the conversion economics. The cash on delivery payment method has its own delivery process, its own delivery costs, its own failure modes. A delivery refusal at the door is not the same as a card chargeback weeks later. A failed COD transaction costs you the inventory journey twice (out and back), the customer support hours required to figure out what went wrong, plus the administrative burdens of reconciliation.

The good cash on delivery (COD) services do not just deliver COD parcels. They flag at-risk orders early, share estimated delivery time updates with the recipient, manage delivery refusal patterns and small delays at the door, and give businesses tools to recover lost conversion rates before parcels turn around.

Two COD services running the same campaign in Poland can produce wildly different revenue figures depending on how each handles buyer drop-off, how clearly the recipient confirmation flow runs, what payment options the courier offers at the door, and how quickly funds land back in the seller’s bank account. The good operators turn this into a real delivery service rather than a shipping commodity. Payment status updates, exception alerts, and reconciliation reports flow back to the seller and the customer support team in real time. The mediocre ones bill you for failed parcels and move on, leaving customers and the accounting team to sort out the mess.

What to look for as you expand

For brands entering new markets, the question is rarely whether to offer COD at all. The convenience of cash collection at the door, especially in regions where COD is the common form of online payment, makes it a near-essential payment option for any meaningful market share. The real question is which operator to pick.

The best cash on delivery services in Europe combine multi-country coverage across international markets with the specific operational discipline a high-volume seller needs:

- Clear tracking of every shipment

- Predictable cash flow into the seller’s financial resources

- A COD solution that scales as you expand from one destination into other countries

- Specialist experience in your vertical, not generalist retail

For businesses with specific needs in supplements, cosmetics, or other repeat-purchase verticals, the advantages of choosing a specialist over a generalist 3PL show up in two places. First, in the buyout rate itself. Specialists know how to script the recipient interaction, time the contact attempts that recover otherwise-lost orders, and minimize the friction points where customers walk away. Second, in the operational fit. A COD solution built around the business needs of a supplements seller looks different from one built around generalist retail. Especially those operating across multiple countries, where regulatory and labelling rules vary, benefit most from this specialization.

The takeaway

Cash on delivery is not a workaround. It is a convenient alternative to card payment that, in much of the world’s online retail outside the most card-saturated economies, drives a significant amount of revenue. Treating it as a second-class payment method, or as a logistics problem rather than a payment problem, is how brands accidentally cap their growth in the markets where COD matters most.

A closing thought

Cash on delivery pays off when you manage buyout, not just delivery. That sentence sounds obvious. It isn’t, given how many providers in this space treat collection at the door as the end of their job rather than the start of yours.

When you’re choosing among the best cash on delivery services in Europe, the five operators above each address a different piece of the same puzzle. The wrong cash on delivery service turns COD into a slow revenue leak. The right one turns it into the most profitable channel in your funnel. For businesses operating at scale, particularly in verticals where cash on delivery is structurally embedded in customer behavior, the partner you want is the one giving your call center the signals it needs, consolidating fulfillment across geographies, paying out on a schedule you can plan around, and standing on legal and operational ground solid enough to grow with you. Four things. Get them right and the rest sorts itself out.