Key findings & trends about the state of grocery retail in Europe

What is the state of grocery retail in Europe? 2023 was a tough year for the sector, but is 2024 better? Find out with this report. (Ad)

Commercial collaboration

Where does the European grocery retail market stand in 2024? After the rollercoaster of 2023, with inflation driving prices up and consumers tightening their belts, things are slowly shifting.

Grocers strive to adapt to changing consumer behaviors and balance the need for affordability with the demand for higher-quality and convenient products. But what exactly does this market look like? What trends are shaping the industry? How are retailers navigating this landscape? And what are the opportunities for growth?

Based on the report from McKinsey & Company and EuroCommerce, we’ll break down the latest findings on the state of grocery retail in Europe.

So, are you ready to discover many insights and data? We hope so!

State of grocery market in Europe

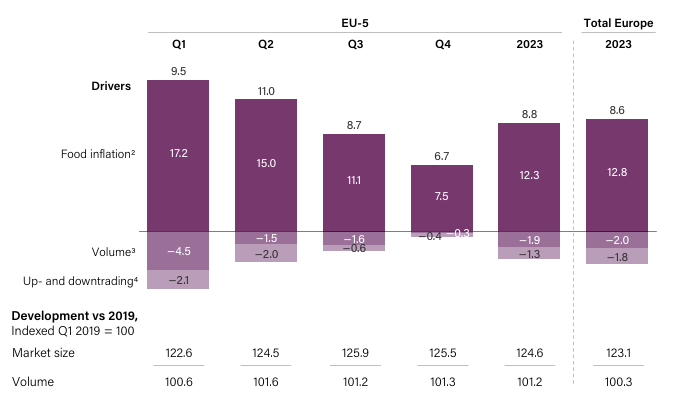

In 2024, Europe’s grocery market shows signs of recovery after a challenging year in 2023. Last year, inflation hit hard and forced many consumers to cut back on spending and opt for cheaper products, like private labels and discount options. Food price inflation averaged 12.8% for the year, peaking at 19.0% in March, which impacted consumer purchasing power.

Despite an overall decline in inflation from a high of 10% in October 2022 to 3% by the end of 2023, real grocery sales dropped by 4.5% compared to 2019. This drop was driven by a combination of factors: a small volume increase and a real-term price decline of 4.8% per item.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

It was a tough time for both shoppers and grocery retailers, with everyone feeling the pinch.

But here’s the good news: things are starting to look up.

Inflation is expected to stabilize around 2%, and real wages will gradually increase across Europe. This is helping to restore some consumer confidence, though the recovery is still mixed.

Some consumers, especially those with higher incomes, are beginning to spend a bit more freely, even trading up to premium products in certain categories. However, many households are still cautious, especially in countries like Italy and Switzerland, where optimism is lower.

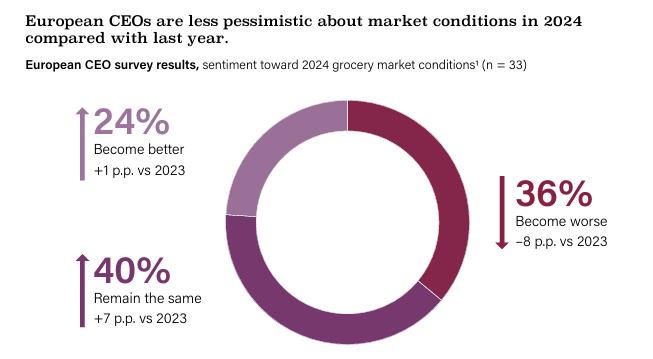

The grocery industry is also adapting. CEOs are less worried than last year, though they remain focused on managing costs and navigating a tricky market. They’re particularly concerned about ongoing price pressures, but there’s a sense of cautious optimism that wasn’t there before. Interestingly, there’s a renewed focus on areas like talent acquisition, government regulations, and loyalty programs – sectors that gained more attention this year compared to last.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

Overall, while the grocery market in Europe isn’t out of the woods yet, 2024 is shaping up to be a year of slow but steady recovery. The landscape is still varied, with different countries and consumer groups experiencing recovery at different paces. But the general trend is positive, with more consumers feeling confident enough to spend a little more on grocery shopping.

This cautious optimism is a good sign for the industry as it looks to bounce back from the challenges of the past few years.

8 key trends that will characterize the European grocery retail market in 2024

Now, let’s look at 2024’s key grocery retail trends.

Trend 1: Pressure on margins and costs

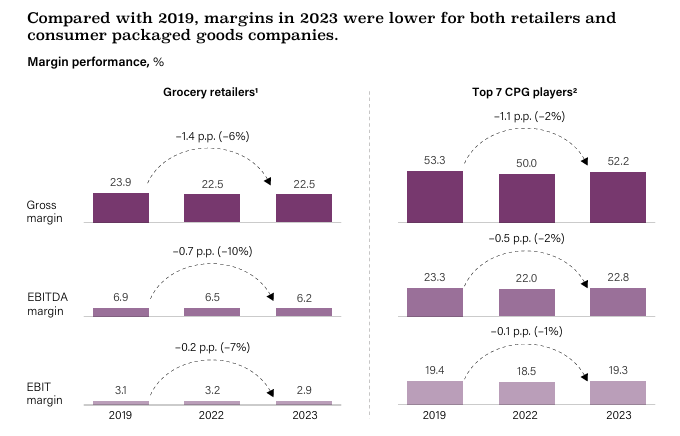

The grocery industry in Europe is expected to continue facing cost and margin pressure in 2024.

Over the past few years, both grocery retailers and consumer packaged goods (CPG) companies have experienced declining profitability. Between 2019 and 2022, grocery retailers lost 0.4 percentage points of their EBITDA margin, while CPG companies saw an even steeper decline of 1.3 points. Although CPG companies regained some ground in 2023, grocery retailers struggled.

The primary drivers of margin pressure in 2024 include rising rent and labor costs, which are expected to persist. As a result, retailers are likely to intensify their supplier negotiations, form more buying alliances, and pursue mergers and acquisitions to achieve economies of scale.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

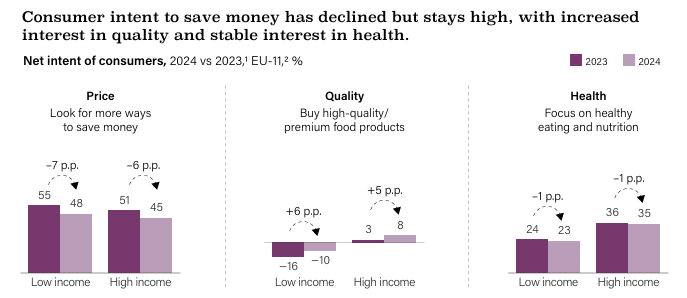

Trend 2: Polarization

In 2024, the European grocery market is expected to see a continued polarization of consumer behavior.

While many consumers are focused on saving money, there is a noticeable shift among high-income households toward uptrading. More than 45% of respondents indicated they are still looking for ways to save money, but this number is lower than last year.

On the other hand, high-income households are beginning to purchase more premium and organic products. They are driven by a desire for higher quality and healthier options. This polarization will likely result in a dual market dynamic, where downtrading and uptrading occur simultaneously across different consumer segments and geographic regions.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

Trend 3: Food to go

The food-to-go market in Europe is experiencing a resurgence as consumers spend more time on the move.

After a decline during the COVID-19 pandemic, the food-to-go sector has rebounded and continues to grow. This market includes:

- prepackaged ready-to-eat meals

- convenience meals

- restaurant takeaways

- and meal delivery services

In 2024, food-to-go is expected to be one of the top trends in the grocery industry, with CEOs predicting that it will drive traffic, increase margins, and create cross-selling opportunities. To capture this growth, grocery retailers are expanding their food-to-go offerings, including ready-to-eat, ready-to-heat, and hot food options, as well as experimenting with in-store food service concepts.

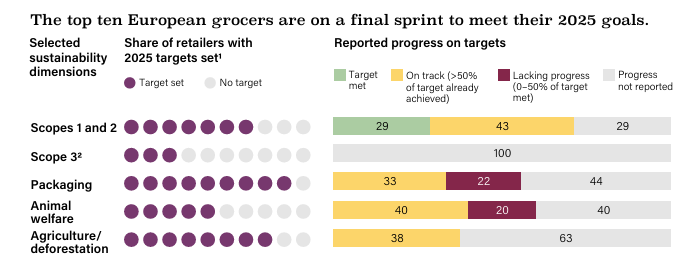

Trend 4: Still a long way to sustainability

Sustainability remains a critical focus for the European grocery industry, but there is still plenty of work to be done.

While all of the top ten European grocery retailers have set ambitious sustainability targets for 2025, progress has been slow, particularly in reducing Scope 3 emissions – the largest contributor to carbon emissions. Reducing these emissions is challenging, but some pioneering retailers are beginning to develop capabilities to track actual emissions by product and supplier.

In addition, regenerative agriculture is becoming a priority since it could reduce greenhouse gas emissions from dairy and meat production, which are major contributors to the grocery industry’s greenhouse gas emissions.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

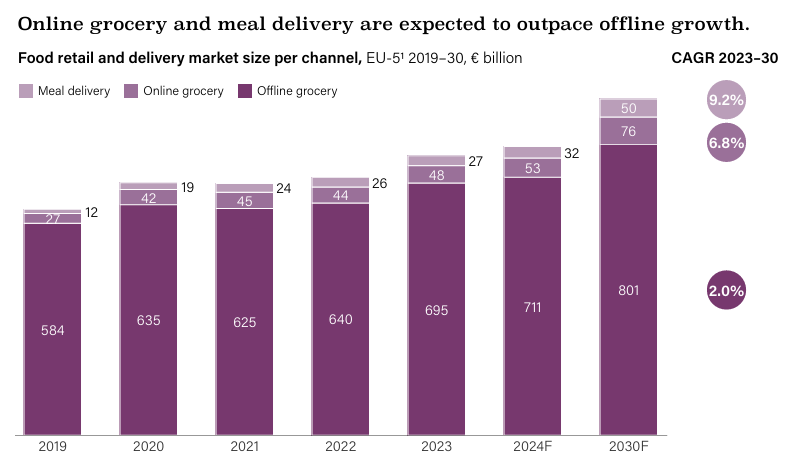

Trend 5: Move to online

Online grocery shopping is coming back in 2024, with consumers increasingly viewing it as a distinct and valuable shopping channel.

After losing market share in 2023, online grocery sales are expected to grow faster than the overall grocery market in the coming years. This growth is driven by a shift in consumer behavior, as more people return to online shopping following an improvement in spending power.

Consumers are also beginning to differentiate between online and offline shopping experiences, with many choosing various retailers depending on the channel. This trend highlights the importance of offering a tailored value proposition for each channel.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

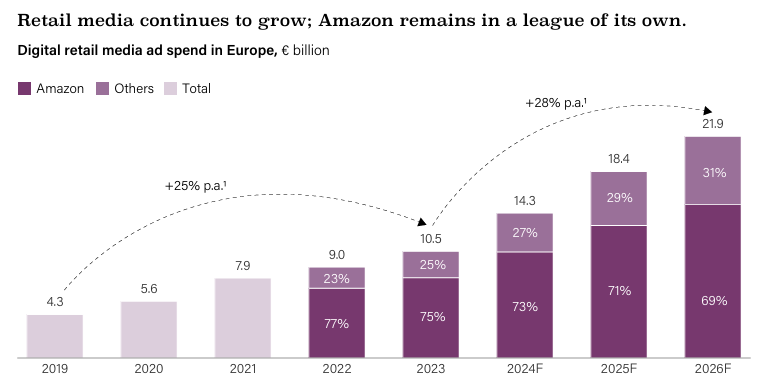

Trend 6: Retail media

Retail media (RM) has emerged as a substantial profit driver for grocery retailers, with 20 of Europe’s top 30 grocery chains actively participating in the market.

The RM sector in Europe is expected to grow by 15% annually in the coming years. To maintain relevance in this competitive space, large retailers are expected to expand their RM footprint aggressively, potentially through partnerships and consolidation. Smaller players may need to band together to compete with giants like Amazon, which dominates the market.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

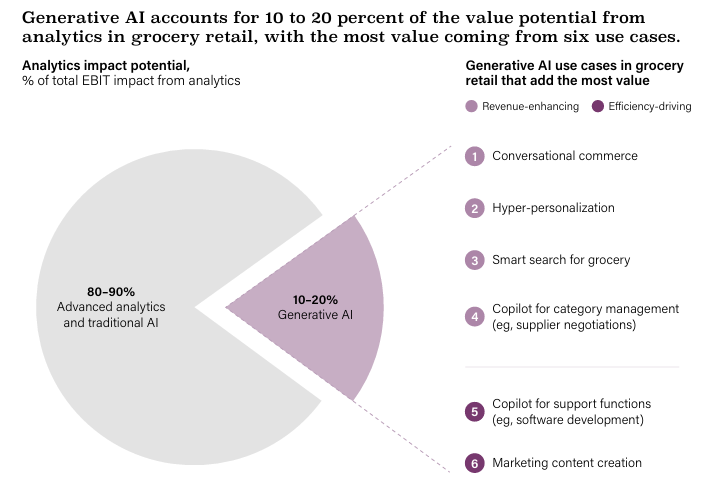

Trend 7: Conversational commerce

Conversational commerce, enabled by generative AI, is poised to revolutionize how consumers shop.

Conversational commerce is emerging as a significant opportunity. This technology allows retailers to engage shoppers with human-like chatbots and offer personalized shopping assistance that can enhance the customer experience.

Although generative AI currently contributes 10 to 20% of the value from advanced analytics in grocery retail, its potential is vast. Retailers explore various use cases, including hyper-personalized content, smart search, and category management copilots. As the adoption of conversational commerce grows, it is expected to become a key component of the retail experience.

Source: The State of Grocery Europe 2024, the McKinsey & Company and EuroCommerce report.

Trend 8: Attracting talents

In 2024, there is a renewed focus on making retail a desirable career path, especially due to increased automation and changing consumer demands.

Retailers recognize the need to invest in their workforce and offer more skill development opportunities. This includes training in new technologies, such as AI and data analytics, and creating pathways for employees to move into management and leadership roles.

Additionally, there is a growing emphasis on improving working conditions and offering competitive compensation packages to attract a younger, more tech-savvy workforce. As the industry continues to evolve, the ability to attract and retain top talent will be critical to maintaining competitiveness.

Grocers have opportunities to grow

Fortunately, there are a number of areas where grocers can focus their efforts to build resilience and gain a competitive edge. Despite inflation pressures, margin compression, and shifting consumer behaviors, grocery stores can strengthen their market position.

How? For example:

By future-proofing the assortment

- Grocers should balance affordability with premium, value-adding products.

- Strengthening private-label offerings is also a must, especially as demand for healthy, ready-to-eat, and ready-to-heat options grows.

- Also, these stores should customize assortments to local markets to maintain and grow market share, as different regions and demographics will recover at varying paces.

By driving nontrivial efficiency savings

- With ongoing margin and cost pressures, grocers must look beyond easy wins and target more significant savings. This includes redesigning operating models, optimizing supply chains from supplier to store, renegotiating rent, and applying design-to-value principles to private-label products.

- They need to address these areas to sustain profitability in a challenging economic environment.

By monetizing retail media

- To scale RM effectively, grocers must think like ad agencies, secure strong leadership commitment, and dedicate resources to RM business development.

- Improving impact measurement and continuously enhancing advertising offerings will help grocers maintain relevance to advertisers and maximize RM profitability.

Over to you

Looking at the state of grocery retail in Europe in 2024, it’s clear the industry is navigating through a mix of challenges and opportunities. The pressure on costs and margins isn’t going away, but there’s also room for growth, especially for those who can innovate and meet changing consumer needs.

It’s all about finding the right balance between managing the tough stuff and spotting where the market is heading next.

The actions taken by grocery stores now will shape their success in the future. So, stay agile, flexible, and remember that this market can still surprise a lot.

Looking for more valuable information?