E-commerce in Germany 2025: Online retail growth returns amid shifting consumer trends

Online retail in Germany returns to growth in 2025. Discover key trends in sales, AI usage, and market shifts driving e-commerce forward.

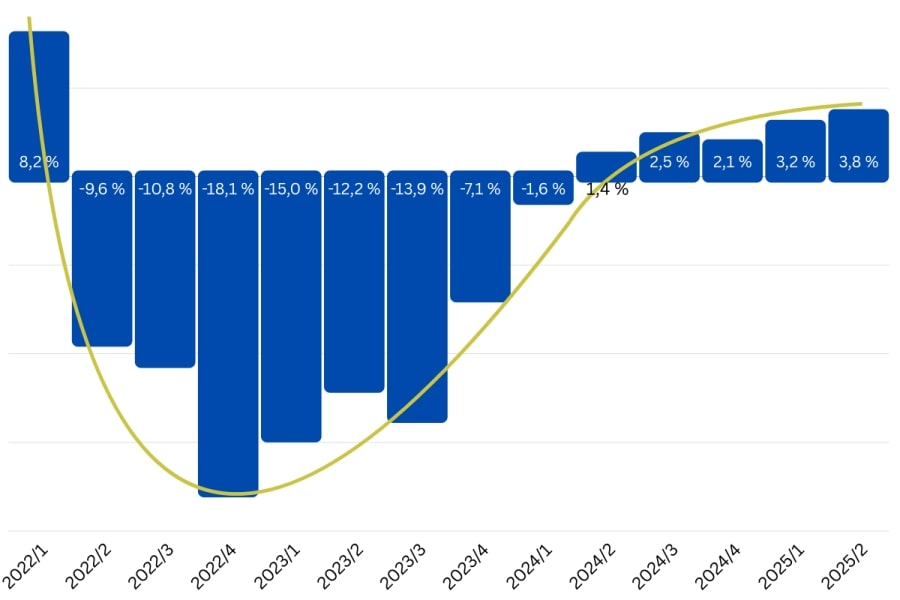

After a challenging period marked by uncertainty and falling sales, online retail in Germany is firmly back on a growth trajectory in 2025. Following several quarters of decline throughout 2023, the first half of this year has brought signs of recovery – driven by improving consumer sentiment, rising adoption of digital services, and the increasing role of AI in the purchasing process.

According to recent figures, revenue from online goods sales grew by 3.5 percent year-over-year, totaling €39.84 billion in the first six months of 2025. The second quarter proved especially strong, with 3.8 percent growth, following 3.2 percent in Q1. While these figures are not adjusted for inflation, they mark a significant shift in consumer behavior and signal renewed vitality in the sector.

A positive turn for online commerce

The momentum behind this renewed growth is multifaceted. Digital services – ranging from travel bookings to ticket purchases – outpaced the trade in goods, with a 4.4 percent increase that brought this segment to €3.9 billion. These gains suggest that consumers are not only spending again but also embracing the digital convenience that e-commerce platforms provide.

“Germans’ shopping mood is slowly but steadily returning,” noted Martin Groß-Albenhausen, Deputy Managing Director of the bevh (German E-Commerce and Distance Selling Trade Association). “This is benefiting online retail in particular, as it best reaches people in their everyday digital lives via social media, apps, and AI.”

While the uptick is welcome news across the industry, not all retailers are benefiting equally. Some business models are thriving, while others continue to feel the weight of structural challenges.

AI’s growing – but cautious

A striking development in 2025 is the increasing use of artificial intelligence in the purchasing process. Tools like ChatGPT and similar AI applications are becoming part of the consumer journey. According to the latest survey data, 19.3 percent of respondents either completely or largely agree that they have already asked AI systems for product recommendations.

However, this trend comes with a caveat: consumers are still skeptical about handing over full decision-making authority to AI. A clear 60 percent said they would never – or only very rarely – follow an AI-generated recommendation without first researching alternatives on their own.

This cautious adoption indicates that AI currently serves more as a supplementary source of information, rather than a primary driver of purchasing decisions. For retailers and marketers, this highlights the importance of being visible in AI-assisted queries while maintaining strong content strategies that support human-led research.

What consumers are buying: Winners and losers by category

While overall growth is a positive sign, it’s worth examining which product segments are driving the upswing and which are being left behind. The most significant surge was recorded in the home and household textiles category, which grew by an impressive 10.5 percent in the spring months.

Footwear also saw a robust rise of 7.6 percent, helping push the entire clothing cluster to a 5.2 percent increase. Other high-performing categories include:

Medications, boosted by the adoption of e-prescriptions: +7.2 percent

Pet supplies: +9.4 percent

Toys: +7.1 percent

Jewelry and watches: +6.8 percent

Household goods and appliances: +4.6 percent

In contrast, some categories experienced notable declines. Car and motorcycle accessories dropped by 6.0 percent, while electronics and telecommunications fell by 3.7 percent. Even traditionally stable categories like books, e-books, and audiobooks saw a modest decline of 2.2 percent, possibly reflecting shifting consumer preferences toward streaming and digital content.

The data reveals a clear pattern: consumers are willing to spend, but they are prioritizing comfort, health, and lifestyle upgrades over high-ticket items or physical media.

The channel divide: Who is capturing the growth?

Not all retail channels are benefiting equally from the market’s renewed momentum. Online marketplaces continue to dominate, with a 5.9 percent increase in sales in Q2 2025. These platforms led by major players like Amazon and bolstered by emerging competitors are benefiting from scale, selection, and consumer trust.

Direct-to-consumer (D2C) models also performed well, with a 5.6 percent increase in sales. These manufacturer-owned channels are leveraging brand loyalty and efficient logistics to compete directly with intermediaries.

Meanwhile, retailers with their own online shops improved by 2.7 percent – a welcome recovery after previous quarters of weak performance. However, multichannel retailers, who maintain both physical stores and online channels, continued to struggle. Their online sales declined by 2.8 percent, suggesting persistent challenges in integrating digital and in-store experiences.

Groß-Albenhausen notes that while the broader market is recovering, competition is intensifying. “The market continues to become more concentrated, and not all retailers are participating in the positive trend. Customers remain price-sensitive and willing to trust low-cost providers from third countries.”

The rise of Asian e-commerce platforms

One of the most disruptive forces in online retail in Germany this year has been the rapid expansion of Asian e-commerce platforms, such as Shein, and AliExpress. These platforms increased their share of all online orders from 5.5 percent in Q2 2024 to 6.4 percent in Q2 2025.

Their influence is especially pronounced in fashion-related categories. In the fashion segment, 14.1 percent of all orders went to these platforms. In fashion jewelry, the figure soared to over 28 percent. Cumulatively, this translated to sales growth of over 37 percent, or nearly €1 billion between April and June 2025.

The success of these platforms is rooted in aggressive pricing, fast production cycles, and strong social media marketing. For domestic and European retailers, this trend poses a serious challenge. Competing on price alone is no longer viable. Instead, differentiation through service, sustainability, and trust will become more important than ever.

A sector recalibrated

Zooming out to the bigger picture, the combined revenue from goods and digital services in interactive commerce (including e-commerce, mail, fax, and written orders) totaled €24.18 billion in Q2 2025 up 3.9 percent from the previous year.

Within this, e-commerce goods alone accounted for €20.16 billion, up 3.8 percent, while digital services rose 3.8 percent to €3.89 billion. The sector is not only growing but also evolving – reflecting deeper changes in how consumers engage with products, services, and brands online.

About the data: A comprehensive look at German consumer behavior

The insights in this article are based on the long-running “Interactive Commerce in Germany” study, conducted by BEYONDATA GmbH on behalf of bevh. This ongoing research effort captures consumer behavior across the entire landscape of online and mail-order retail.

Each year, 40,000 private individuals aged 14 and over are surveyed from January to December. The data presented here reflects results for the period April 1 to June 30, 2025.

The study is considered one of the most comprehensive in Germany, covering both physical goods and digital services, as well as all sales channels from pure online players to multichannel and D2C brands. The survey’s robust methodology ensures that the trends discussed are grounded in real consumer behavior, not speculative projections.

Final thoughts: A market in motion

The return to growth in online retail in Germany is real but uneven. While some players are thriving thanks to agile models, international reach, and smart use of technology, others are falling behind. What’s clear is that consumer behavior continues to evolve, and the businesses best positioned to meet those changes head-on will define the next chapter of e-commerce.

To succeed, retailers must prioritize digital optimization, customer experience, and channel flexibility. The influence of AI, the rise of global competitors, and the resurgence in consumer confidence all point toward a rapidly shifting but opportunity-rich environment.

Germany’s e-commerce market is no longer simply recovering – it’s transforming. And for those willing to adapt, the future holds strong potential.

***