European Ecommerce Overview: France

As of 2026, France ranked as the third-largest e-commerce market in Europe. What makes France so successful? Find out in our analysis

France’s e-commerce market enters 2026 in a strong and surprisingly balanced position. It is large, mature, and highly competitive, yet it still has room to grow in several meaningful directions.

What makes France interesting right now is that growth no longer comes only from Paris or from classic online retail giants. Momentum is also coming from regional shoppers, mobile-first behavior, sustainable commerce, and stronger domestic marketplace ecosystems.

The numbers support that story. They signal a market that is evolving in infrastructure, consumer expectations, and category mix at the same time.

Let’s break down what this means for brands, marketplaces, and international sellers looking at France in 2026.

E-commerce overview

France’s online retail space in 2026 feels both established and dynamic.

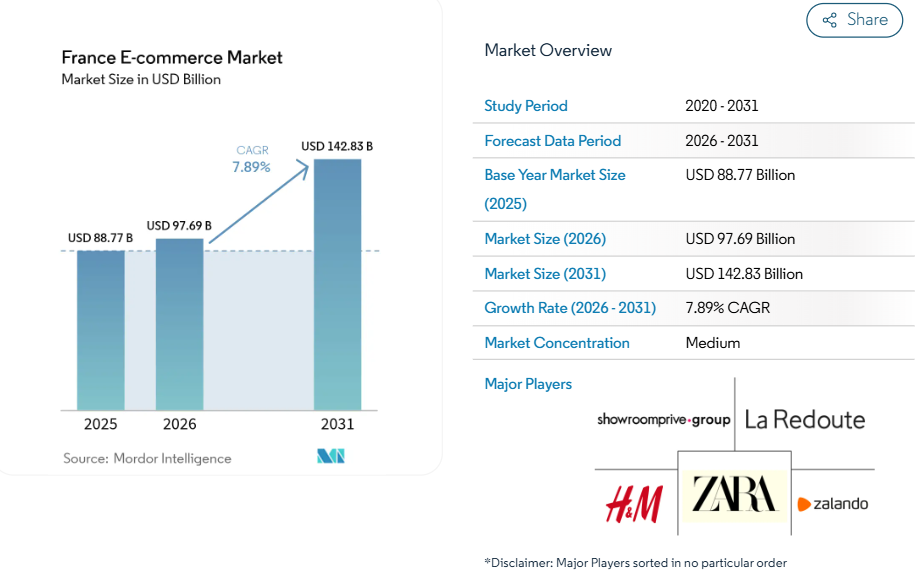

The first thing worth noticing is scale. The market is approaching the $100 billion mark in 2026, which places France among the most important e-commerce economies in Europe.

The data show us:

- $97.69 billion market size in 2026

- 7.89% CAGR through 2031

- medium market concentration

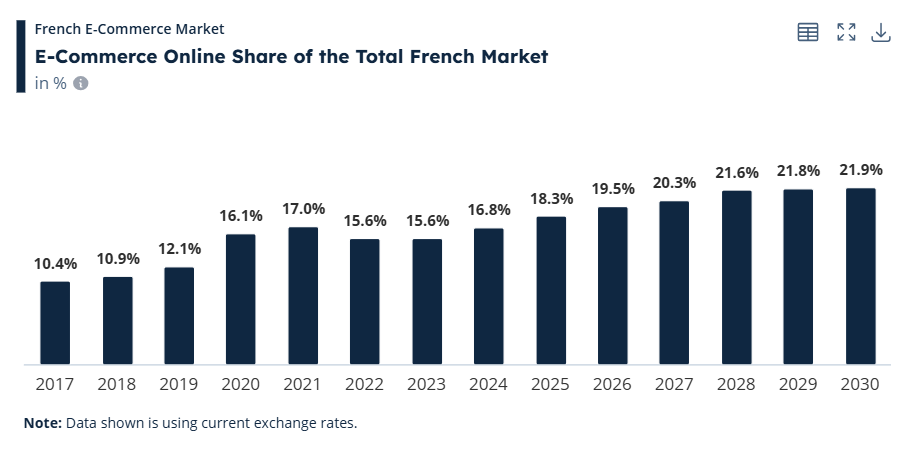

- online share rising to 19.5% of the total French market in 2026

- projected to move above 20% from 2027 onward

That online share number is particularly important.

At 19.5% in 2026, nearly one in every five retail euros in France is expected to come through online channels. That is a major structural shift in how consumers buy, compare, and repeat purchase.

Another strong market signal is infrastructure.

France now has 93.5% nationwide fiber coverage, while 5G penetration has reached 29% of mobile connections. This matters because it reduces the old urban-rural divide.

For years, e-commerce in France was strongly centered around major metro areas. In 2026, this changes.

Consumers in Brittany, Occitanie, Nouvelle-Aquitaine, and smaller regional zones now shop with nearly the same speed expectations as Paris shoppers.

That directly supports:

- same-day fulfillment expansion

- higher mobile conversion

- better click-and-collect adoption

- growth in local and regional brands

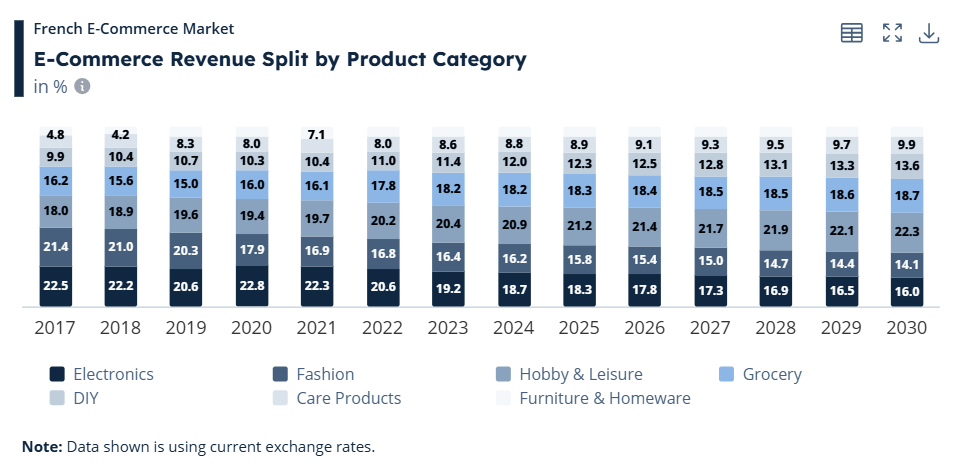

The product mix is also evolving.

Fashion remains a leading category, but grocery, home, beauty, and second-hand marketplaces are growing fast. Category revenue split in 2026 shows strong balance across:

- fashion: 21.4%

- electronics: 17.8%

- hobby & leisure: 15.4%

- grocery: 12.5%

This tells us France is not dependent on one vertical. That diversity usually creates a healthier market.

Consumer behavior

French online shoppers in 2026 are more deliberate, more mobile, and more value-conscious than in previous years.

The most important behavioral trend is mobile dominance.

According to Mordor, smartphones account for 78.67% of transaction value, and that trend continues to strengthen beyond 2026.

That means nearly four out of five purchases happen on mobile devices. This changes how brands should build storefronts.

A desktop-first UX simply no longer fits the market.

French consumers increasingly expect:

- fast-loading mobile pages

- one-click checkout

- wallet payments

- live stock visibility

- delivery slot selection

Another major shift is sustainability.

French shoppers are clearly leaning into more responsible buying patterns.

Second-hand and recommerce are no longer niche. Platforms like Vinted are now fully mainstream, and the market data supports this long-term direction.

This is especially visible in fashion and home categories, where consumers actively compare:

- price

- delivery speed

- sustainability

- resale value

There is also a strong local preference developing.

The “Made in France” label continues to influence conversion rates, especially for food, beauty, fashion, and artisan products.

Government support under France Num is helping smaller domestic sellers enter digital commerce, which broadens assortment depth and reinforces local trust. That trust matters.

French shoppers tend to be research-heavy before purchase. They compare more, read more, and often check delivery terms carefully before checkout. This means product pages need stronger informational content than in some faster-moving markets.

Clear return policies, detailed shipping windows, and transparent sourcing work especially well here.

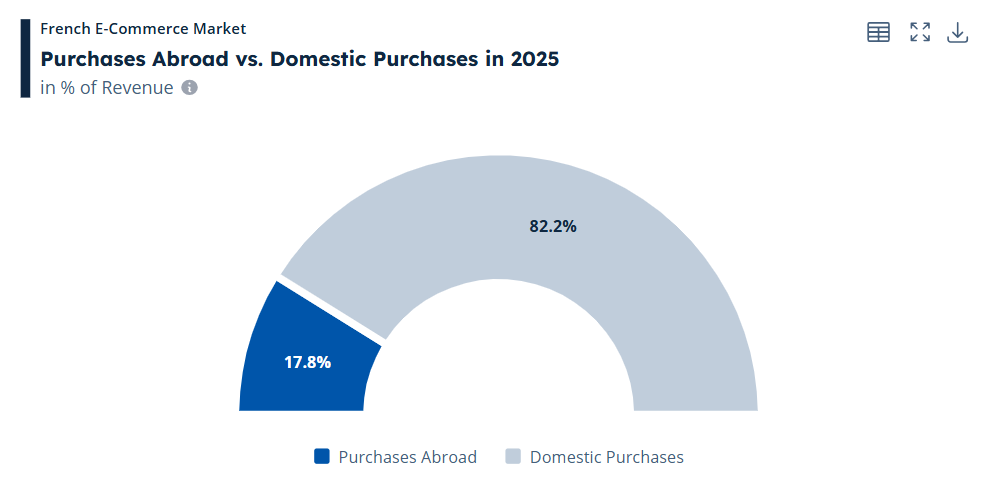

Cross-border shopping is also interesting. 17.8% of purchases in 2025 came from abroad, and this trend remains relevant for 2026 planning.

A large portion of this volume comes from Chinese stores, led by platforms like Shein and AliExpress. This creates strong pricing pressure on domestic retailers.

Payment

Payments in France in 2026 are stable on the surface, but there are meaningful shifts underneath.

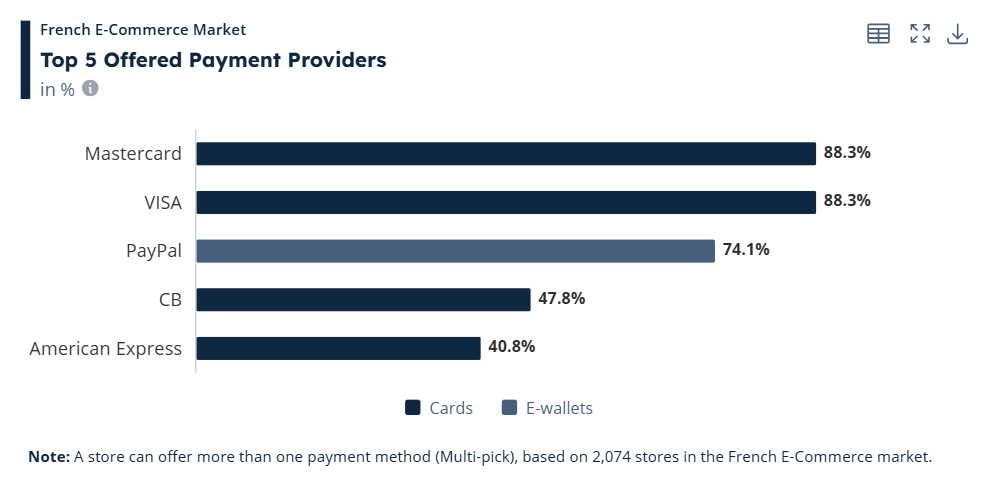

Cards still dominate. From your market data, the top payment providers include:

- Mastercard: 88.3%

- Visa: 88.3%

- PayPal: 74.1%

This shows that traditional card rails remain deeply embedded in French online commerce.

At the same time, one trend deserves special attention: buy now, pay later. Mordor projects BNPL to grow at a 9.27% CAGR beyond 2026, making it one of the fastest-growing payment behaviors in the market.

This is especially relevant for:

- fashion

- beauty

- electronics

- higher-ticket lifestyle purchases

Younger consumers, especially Gen Z and millennials, continue to drive this shift. Installment payments are no longer treated as exceptional financing. They are increasingly becoming part of the default checkout flow. That directly lifts average order values. Moreover, order value can increase by up to 30% when BNPL is displayed clearly.

That is a major commercial lever. And for brands entering France in 2026, payment flexibility is not optional.

At minimum, checkout should support:

- cards

- PayPal

- BNPL

- Apple Pay

- local wallet options

Social media

Social media in France’s e-commerce market is becoming less about awareness only and much more about conversion. In late 2025, France had 51.5 million social media user identities, as many as 77.2% of the total population.

- Facebook had 31.5 million users

- Instagram had 28.2 million users

- TikTok had 23.4 million users

- And LinkedIn had 38.0 million “members”

They are increasingly feeding direct product discovery journeys. This is especially true for:

- fashion

- beauty

- home décor

- lifestyle accessories

The key shift is that social is no longer top-of-funnel only. It now actively supports transaction intent. TikTok and Instagram drive traffic into:

- product launches

- drops

- influencer-led edits

- limited collections

- resale and sustainable fashion stories

This fits French consumer behavior well. People like context before purchase. They want to see how something looks, how it is used, and how others style or review it. That makes short-form video extremely effective.

For 2026, brands selling into France should think in terms of social commerce storytelling, not isolated product posts.

Useful formats include:

- styling videos

- product comparison clips

- unboxing

- delivery experience videos

- “Made in France” craftsmanship content

Social proof matters a lot here. This is one reason Shein, Zara, and Zalando continue to capture strong digital traffic.

Logistics

Logistics may be one of the strongest competitive advantages in France in 2026. The delivery ecosystem is mature, dense, and increasingly optimized.

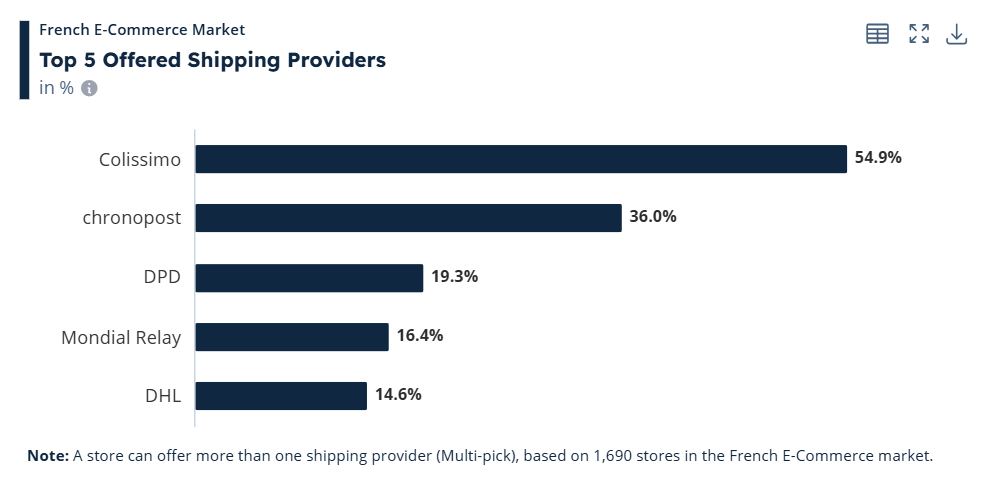

The leading shipping providers are:

- Colissimo: 54.9%

- Chronopost: 36.0%

- DPD: 19.3%

- Mondial Relay: 16.4%

- DHL: 14.6%

French consumers are familiar with delivery options and often have clear preferences.

Parcel lockers and relay pickup points continue to grow. This supports the strong click-and-collect culture already present in the market. For urban and suburban shoppers, pickup flexibility is often valued as much as speed.

Another important trend is same-day and next-day expansion outside Paris. Because fiber and mobile infrastructure have improved nationwide, logistics providers can now support broader regional service levels.

This reduces the advantage previously held by Paris-only retailers. The challenge, however, remains returns. Fashion returns remain expensive.

Reverse logistics costs are one of the main restraints. That puts margin pressure on apparel sellers, especially those competing with fast-fashion imports.

Brands need:

- clearer sizing tools

- better fit content

- easier exchange flows

- smarter return routing

To sum up

France’s e-commerce market in 2026 is large, modern, and still expanding in meaningful ways. But the story is bigger than growth alone.

This is a market shaped by:

- strong logistics

- mobile-first consumers

- sustainable shopping habits

- rising BNPL usage

- local brand trust

- cross-border price competition

For brands entering France, success in 2026 comes down to three things:

mobile experience, payment flexibility, and logistics reliability.

Get those right, and France remains one of the most promising e-commerce markets in Europe.