Top Insights about the State of Fashion [Business of Fashion and McKinsey & Company report]

The fashion industry has been on a rollercoaster ride since the onset of the COVID-19 pandemic. After a sharp rebound in 2021 and much of 2022, industry executives are now expressing concern about the year ahead. A recent survey by the Business of Fashion and McKinsey & Company revealed that 84% of fashion leaders expect market conditions to decline or stay the same in 2023.

In this article, we will delve into the top insights about the current state of fashion and what fashion executives can do to stay ahead. Read our article or the whole report here!

Executive Summary

The fashion industry experienced impressive growth in 2021 and the first half of 2022, but macroeconomic and geopolitical conditions have challenged it. A variety of factors have disrupted the industry, including inflation, the war in Ukraine, disruptions in supply chains, and an energy crisis.

Looking ahead to 2023, fashion executives predict inflation and an energy crisis will weaken the market. McKinsey expects global fashion sales growth of 5 percent to 10 percent for luxury and negative 2 percent to positive 3 percent for the rest of the industry in 2023.

To respond more effectively to risk, fashion companies will need to rethink their operations, update their organizational structures, and introduce new roles or elevate existing ones.

Brands may also team up with manufacturing partners to sharpen their supply chain strategies. Distribution channel mixes are also ripe for reassessment. Brands will need to factor in the continued return of international travel to pre-pandemic rates, requiring them to look beyond tier-one cities to be physically closer to consumers. Consumer behaviors in 2023 will depend greatly on household incomes.

While higher-income households will continue shopping for luxury goods, lower-income households will likely cut back or even eliminate discretionary spending, including apparel.

Source: Business of Fashion and McKinsey & Company report

Industry Outlook

As we have said before, the fashion industry rebounded strongly in 2021 and much of 2022, but fashion executives are largely pessimistic about the year ahead.

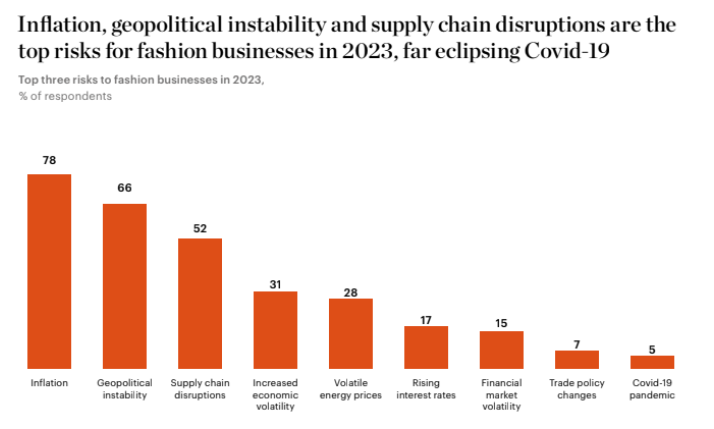

There is a major concern about inflation in Europe and the US, since prices have reached historical highs, and central banks are raising interest rates. This is expected to lead to a decrease in consumer demand, as well as increasing costs for brands due to a competitive labor market and rising energy prices.

Other concerns identified by executives include:

- geopolitical instability and conflict,

- supply chain disruptions,

- increased economic volatility,

- and rising energy prices.

The war in Ukraine is cited as a specific geopolitical issue. Despite the ongoing pandemic, only 5% of executives listed Covid-19 as a top concern for 2023, showing that economic and geopolitical issues have eclipsed the public health crisis.

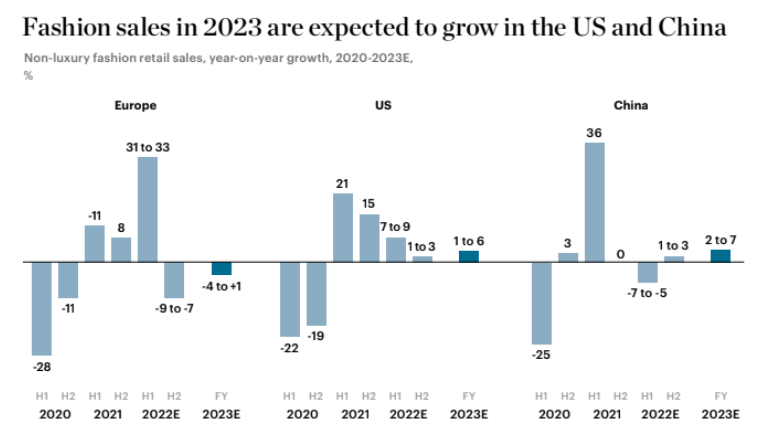

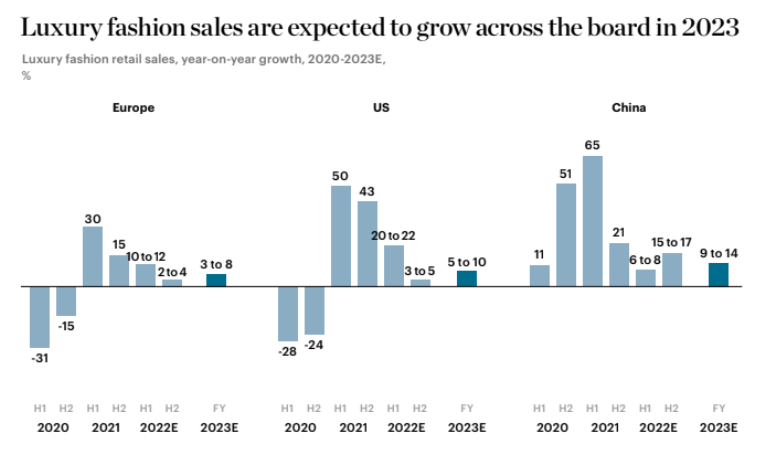

Outlooks for 2023 vary by region, with US executives more optimistic than those in Europe and Asia. The luxury segment is expected to show more resilience than other categories, with projected sales growth of 1-3% in the second half of 2022 and 5-10% in 2023. However, for the rest of the industry, growth in 2023 is likely to be flat or negative, with sales potentially declining year-on-year.

Source: Business of Fashion and McKinsey & Company report

Overall, the industry is expected to contract by 5-7% in the second half of 2022, with slight improvements projected for 2023, but growth will be impacted by inflation and other challenges.

Source: Business of Fashion and McKinsey & Company report

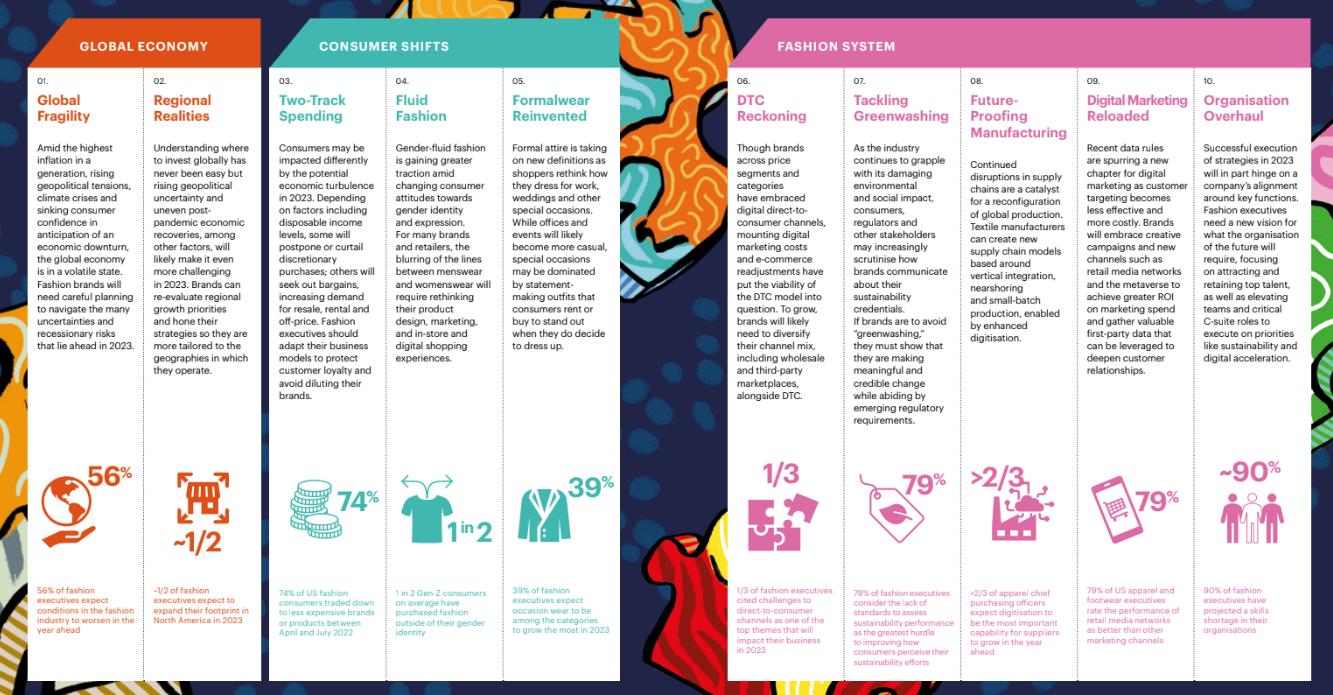

Global Economy

Global economic conditions are volatile amid rising inflation, geopolitical tensions, climate crises, and low consumer confidence ahead of an economic downturn. To navigate the many uncertainties and recessionary risks that lie ahead in 2023, fashion brands will need to plan carefully.

Key insights:

- The global economy is facing destabilizing factors such as inflation and geopolitical tensions, leading to a projected decrease in global GDP growth to 2.5 percent in 2023, and raising concerns about a potential recession.

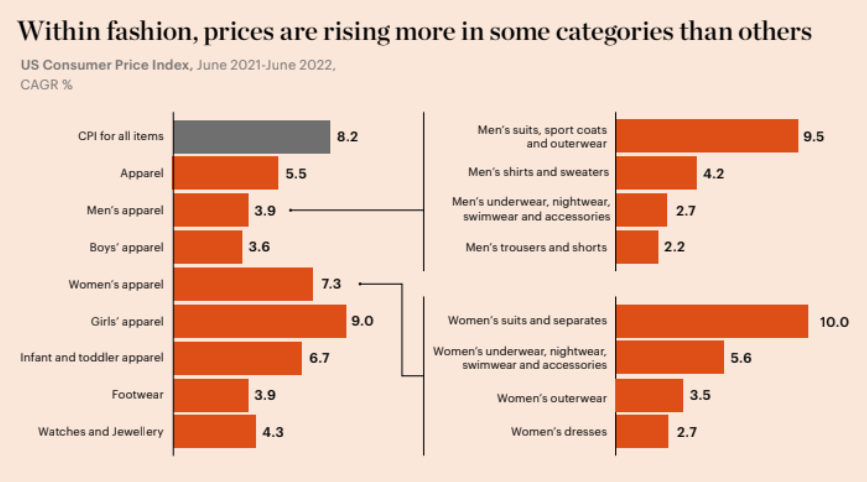

- Consumers are cutting back on discretionary spending, with Europeans planning to make the largest reductions in spending on apparel, footwear, accessories, and jewelry.

- Fashion executives are responding by planning to increase prices and focus on cost improvements in 2023 to protect their bottom lines.

Source: Business of Fashion and McKinsey & Company report

Source: Business of Fashion and McKinsey & Company report

Therefore, there are some priorities:

- To address these challenges, fashion executives should broaden their scenario planning to consider a full range of economic and political outcomes and create flexible contingency plans.

- Additionally, building greater pricing capabilities is essential to adapt to a high-inflation environment and protect top lines, while crafting bespoke pricing strategies to account for fluctuations in customer purchasing power.

- Leaders should prioritize profitability over revenue and market share by making difficult trade-offs in inventory and supply chain management as capital supply tightens.

Consumer Shifts

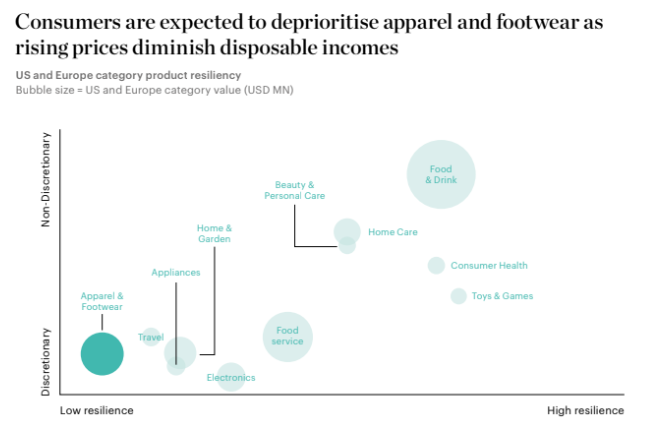

The potential economic turbulence in 2023 may affect consumers differently. Some consumers will postpone or curtail discretionary purchases due to factors such as disposable income levels, while others will search for bargains, increasing the demand for resale, rentals, and off-price items. To protect customer loyalty and avoid diluting their brands, fashion executives should adapt their business models.

Key insights:

- The shopping behavior of different income groups will differ. High-income shoppers may continue to spend on fashion with savings, credit access, and job security, but lower-income consumers will tighten or cut discretionary spending.

- In particular, younger generations may seek out lower-priced retailers and discounts. Gen-Z and Millennials are more likely than Gen-X and Baby Boomers to be taking steps to manage their finances.

- There will be an increase in off-price channels – forecast to account for 12 percent of fashion industry revenues by 2025 – as well as resale, which is expected to grow 11 times faster than apparel retail.

Source: Source: Business of Fashion and McKinsey & Company report

In terms of that, your priorities should be:

- Developing nuanced customer profiles – Determine how customer groups in different demographics and locations are shifting their behavior and introduce new channels, pricing strategies, or products to address these shifts.

- Turning on off-price – Develop strategies for capturing value from promotions and discounts with strategic off-price partners without diluting the brand.

- Exploring the 3 Rs – Integrate new models such as resale, rental, and repair into the value proposition to enable consumers to consume responsibly and affordably.

Fashion System

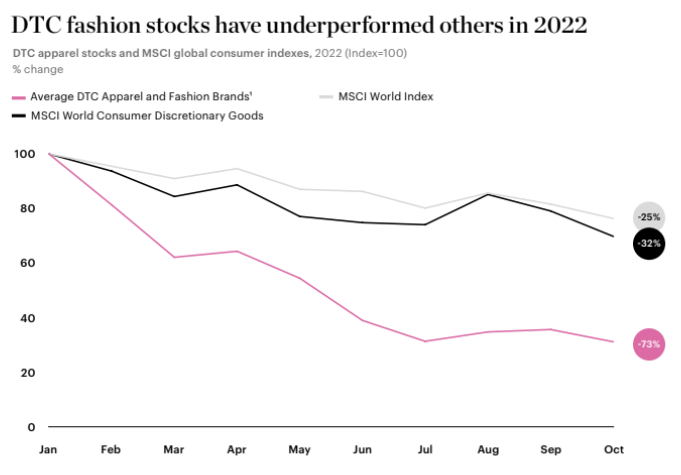

The viability of direct-to-consumer channels has been questioned by mounting digital marketing costs, and e-commerce adjustments as brands across price segments and categories embraced direct-to-consumer channels. In order to grow, brands will likely need to diversify their channel mix, including wholesale and third-party marketplaces as well as direct-to-consumer sales.

Key insights:

- An unprecedented growth rate in e-commerce is beginning to normalize. Between 2022 and 2025, e-commerce sales are expected to grow by 10 percent in the US and 11 percent in Europe, a slower growth rate than 30 percent from 2019 to 2020 and more in line with the 15 percent and 14 percent pre-pandemic rates.

- Digital marketing costs are rising along with online return rates, which cost brands between $21 and $46 per returned product in the online DTC channel.

- From mono-brand stores to concessions at multi-brand retailers, brands are focusing on physical touchpoints. First time in over three years, physical store openings in the US outpaced closures in 2022.

Source: Source: Business of Fashion and McKinsey & Company report

Some executive priorities include:

- Multichannel – Direct-to-consumer channels should be reserved for the most loyal, high-value customers and paired with multi-brand retail and marketplace channels to drive growth.

- Rethinking the physical footprint – Determine which physical stores continue to deliver ROI, leveraging physical touchpoints to connect with customers emotionally.

- Discover new customers through retail partnerships – Engage new customers without investing heavily in mono-brand stores through selective collaborations with retail partners and pop-up events.

Over to You

In summary, the global economy is facing significant challenges, and the fashion industry is not immune. To overcome these challenges, fashion executives must broaden their scenario planning, build pricing muscle, and hone profitability. By taking these steps, they can adapt to the high-inflation environment, protect their top lines, and prioritize profitability over revenue and market share.

If you want to be in touch with us and receive valuable insights, subscribe to our newsletter, and nothing will miss you.