Top insights on 2023 Global Outlook [BlackRock Investment Institute report]

The past year has been one of uncertainty, disruption, and transformation, with many of these changes likely to persist well into 2023 and beyond. In this report, we will explore some of the key challenges and opportunities that are shaping the global landscape and driving change in various sectors

Let’s take a look at what BlackRock Investment Institute has to say. The full report can also be found here.

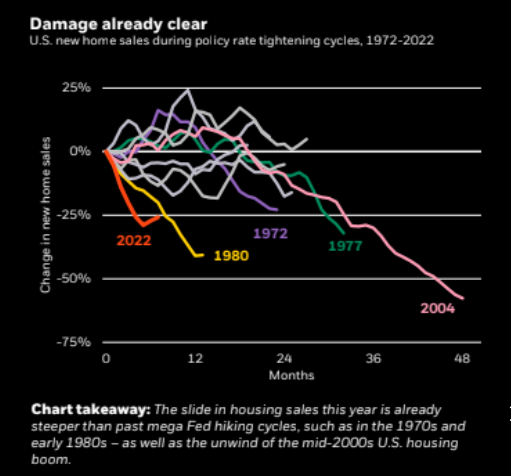

Pricing the Damage

Central banks are taming inflation. It’s most evident in rate-sensitive sectors in the U.S. Rising mortgage rates have slowed home sales.

Source: BlackRock Investment Institute report

Other warning signs include declining CEO confidence, delayed capital spending plans, and consumers’ depleting savings. In Europe, tightening financial conditions amplify the impact of the energy shock on incomes. How far central banks go to reduce inflation determines the extent of the economic damage.

Markets look past the damage and market risk sentiment improves in a way that would encourage people to increase their risk appetite. However, we haven’t reached that point yet.

Rethinking Bonds

After global yields surged, fixed income finally offered “income.” Having been devoid of yield for years, bonds have gained in popularity. A granular approach to investing is taken to capitalize on this rather than taking a broad, aggregate approach.

It is also possible to diversify income with agency mortgage-backed securities – a new tactical overweight. We now separate short-term government debt into a separate tactical view at current yields.

According to the chart, the negative correlation between stock and bond returns has already flipped, meaning they can both fall together. Why is this happening? In recessions they engineered to bring inflation down to policy targets, central banks are unlikely to intervene with rapid rate cuts. There is a possibility that policy rates will remain higher for a longer period of time than the market anticipates.

Source: BlackRock Investment Institute report

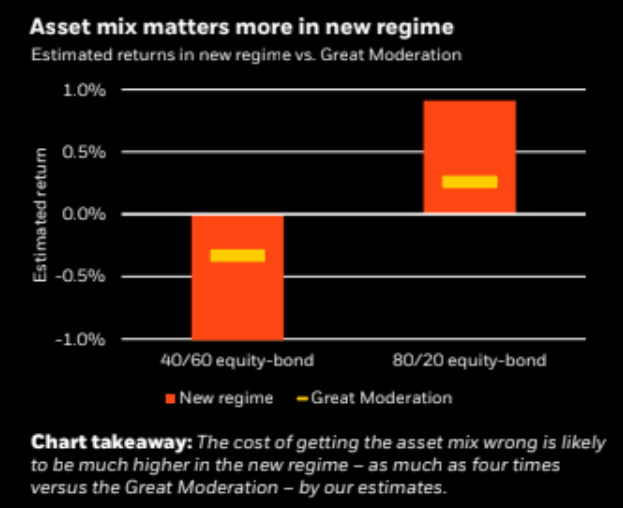

A New Strategic Approach

Strategic portfolios were relatively stable during the Great Moderation. It won’t work under the new regime. Unlike what they experienced in the prior decade, BlackRock doesn’t see conditions that will sustain a joint bull market in stocks and bonds. In spite of the fact that the asset mix has always been important, their analysis suggests that getting it wrong could be four times more costly than during the Great Moderation. On the chart, you can see the difference between the orange bar and the yellow markers. In order to achieve similar levels of return as before, it will take higher portfolio volatility to achieve zero or even a positive correlation between stocks and bonds.

Source: BlackRock Investment Institute report

It’s estimated that stocks will return more over the next decade than fixed-income assets. It is possible to gain a more detailed understanding of structural trends by staying invested in stocks and their prices, for example through 409A valuation services. BlackRock remains overweight inflation-linked bonds and underweight nominal DM government bonds. They prefer short maturities within government bonds to harvest yield and avoid interest rate risk. In fixed income, they prefer public credit over private credit – and they prefer to take credit risks in credit.

Aging Workforces

Aging populations drive production constraints in the new regime. It has taken a long time for the effects to manifest, but now they are becoming more binding. Why? Population aging means shrinking workforces.

In the coming years, the available workforce will expand much more slowly than it has in the past. As a result, economies won’t be able to produce as much. People do not believe that aging populations consume substantially less, particularly when healthcare is taken into account. This means continued inflation pressure as reduced production capacity struggles to meet demand while government spending on elderly care is increasing debt.

Source: BlackRock Investment Institute report

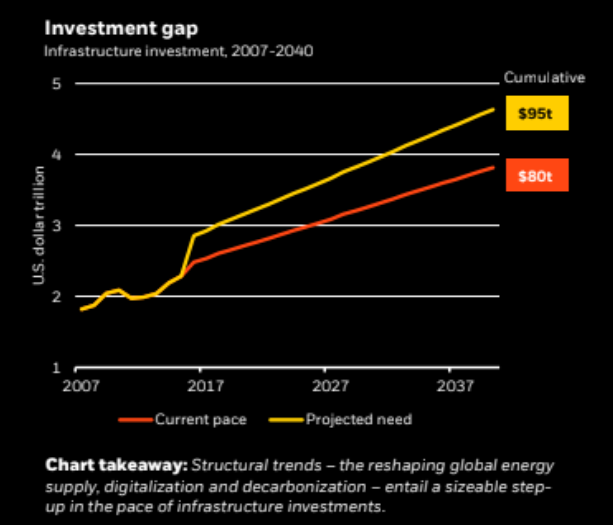

The Long View on Infrastructure

In the private markets, valuations have not caught up with the public market selloff, reducing their relative attractiveness. BlackRock, in its strategic view, underweights private markets, particularly segments such as private equity that have seen heavy inflows. Nevertheless, they believe private markets – a complex asset class not suitable for all investors – should get a larger allocation than what most qualified investors currently do.

Infrastructure offers some big opportunities. Roads, airports, and energy infrastructure are essential to industry and households alike. The energy crunch and digitalization have the potential to increase capital demand for infrastructure over the long term. There is an estimated $15 trillion gap between existing investments and what’s needed to meet global infrastructure demand over the next decade according to World Bank data.

Source: BlackRock Investment Institute report

Over to You

In conclusion, the 2023 Global Outlook presents both challenges and opportunities for individuals, businesses, and governments alike. We hope that this report has provided you with valuable insights and analysis to help you navigate the complexities of the global environment.

Thank you for reading, and we wish you all the best in your future endeavors. Also, don’t forget about our newsletter!