2022 Ecommerce Fulfillment Trends [Saddle Creek report]

It’s no surprise that ecommerce is now the preferred shopping method. As many as 68% of consumers say so, an increase of 16% from 2020. That’s quite a lot, isn’t it?

With so many consumers choosing ecommerce, they have certainly driven some trends in this area. What are they? Are they different from those of two years ago? To get answers to these questions, Saddle Creek prepared a report referring to a similar survey conducted in early 2020. 283 respondents participated in the survey, so let’s see what they said!

Online Sellers

Before COVID, most companies were involved in ecommerce to some degree. Among the surveyed companies, 44 percent work for ecommerce companies/online retailers, and 19 percent work for brick-and-mortar or omnichannel retailers, but wholesalers/distributors, manufacturers, direct-sales companies, and consultants also are represented.

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

There are companies in a variety of industries, including:

- consumer electronics (20%),

- apparel/accessories (13%),

- home furnishings (10%),

- food/drug (7%),

- health/beauty (6%),

- home improvement (6%),

- office supplies (6%)

- and more.

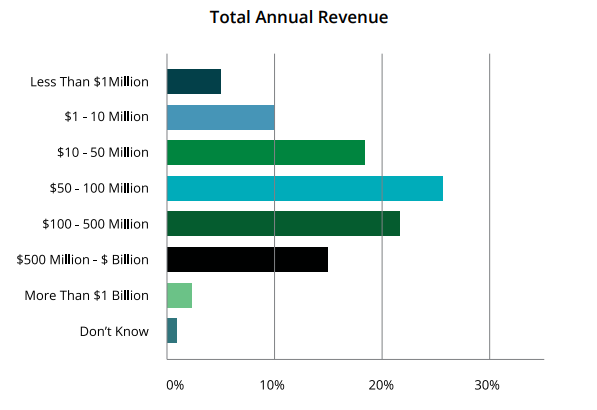

The size of the companies ranges from less than $1 million to more than $1 billion in annual revenue. Almost half (47%) of respondents come from companies with $50 million to $500 million in revenue, while a third comes from companies with less than $50 million in revenue.

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

Taking a look at the ecommerce experience

Order volume

59% of respondents said the volume of online orders increased, while 27% said the volume decreased. About two-thirds of large and medium-sized companies reported growth, compared to only 40% of companies with annual revenues of $50 million or less.

21% of companies cited growing or fluctuating order volumes as one of their top three challenges last year. But, again, it was a more significant problem for large companies (32%) than for small (12%) and medium-sized companies (20%), probably due to their more flexible nature, as smaller companies tend to be more agile and able to adapt quickly.

Deliveries

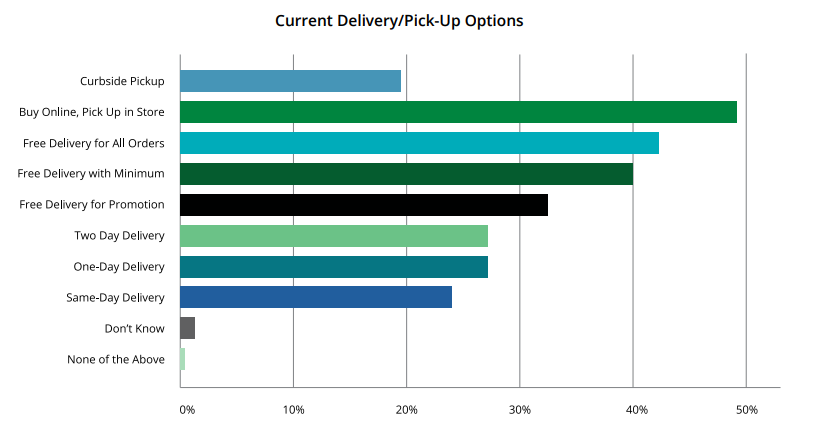

Customers can choose from various delivery/pick-up options offered by respondents. In addition, there is a wide range of free delivery options – for all orders (43%) or with minimum order (40%) or promotion (34%).

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

For comparison, free delivery with a minimum order was more common (57%) in Saddle Creek’s 2020 study than free delivery for all charges (24%).

Moreover, overall, 79 percent of respondents offer free returns (up from about 50% in 2020), and another 13% plan to offer free returns in the next 12 to 18 months.

Fulfillment costs

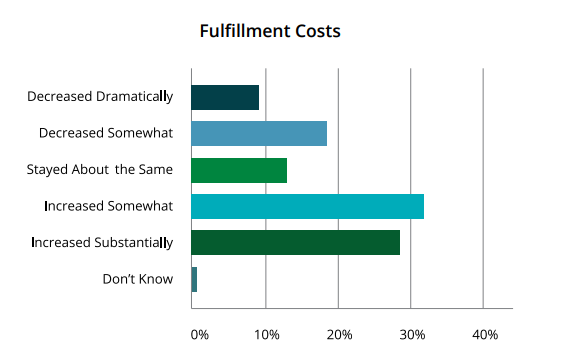

Many respondents incurred higher costs due to increased order volume or fluctuating customer expectations.

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

Over the past year, 51% of companies report that their fulfillment costs have increased somewhat or substantially. Interestingly, this is slightly lower than Saddle Creek’s 2020 survey, when 53% of respondents reported increasing costs.

According to respondents whose costs increased, labor was the leading factor, followed by customer service requirements and the competitive landscape.

In this year’s data, small companies were likelier to feel the impact of shipping costs, while large and mid-sized companies were more concerned about labor costs.

Distribution

To reduce transit time and costs, companies utilize multi-node distribution networks to move inventory closer to end customers. As a result, supply chain disruptions can also be mitigated. As many as three-fourths of respondents are satisfied with the effectiveness of their distribution networks.

Retailers often use their brick-and-mortar stores as distribution centers. Among these, 43% fill less than half of their ecommerce orders from stores, 32% fill 50-75%, and 19% fill more than 75%.

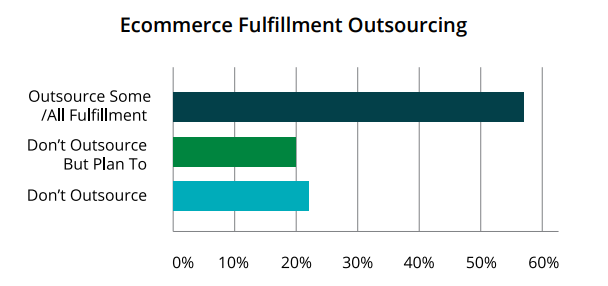

Outsourcing

Over half of respondents (57%) outsource some or all of their ecommerce fulfillment to third parties – a significant increase over Saddle Creek’s 2020 study, where 29% outsourced fulfillment. Twenty percent of respondents plan to begin outsourcing within the next 12 to 18 months.

What’s more, the number of small (61%) and mid-sized (59%) companies that outsource is higher than the number of large companies (40%).

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

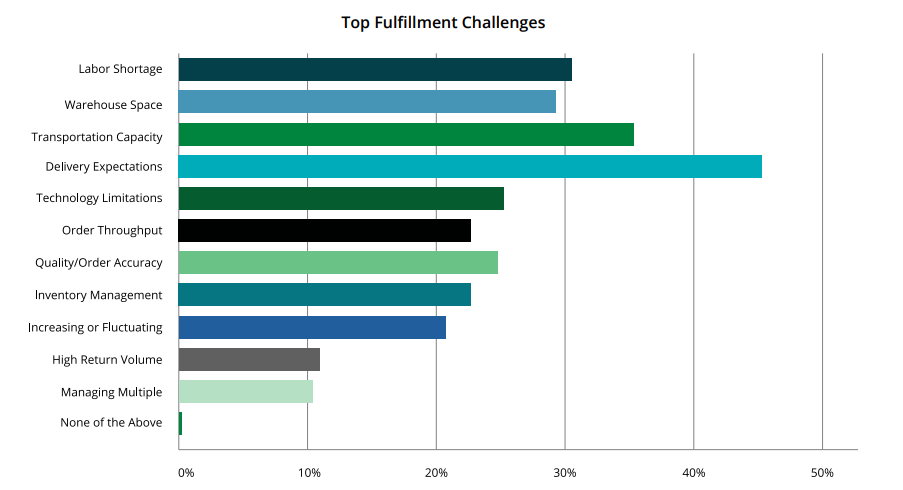

Identifying and Solving Fulfillment Challenges

The past year was filled with challenges for respondents. The five factors were:

- delivery expectations,

- transportation capacity,

- labor shortages,

- warehouse space,

- and technology limitations.

source: 2022 Ecommerce Fulfillment Trends Report from Saddle Creek

A record volume of ecommerce orders, rising rates, and capacity issues made shipping particularly challenging this year. Therefore, the most common fulfillment challenges were delivery expectations (45%) and transportation capacity (36%).

In the past year, the labor shortage affected most fulfillment operations significantly. Seventy-seven percent of respondents say that it has affected their operations somehow.

What’s more, 29% of respondents felt constrained by warehouse space limitations, and 26% felt limited by technology restrictions.

In the past year, inventory issues also affected fulfillment operations. Despite just 24% of respondents identifying inventory management as one of their top three fulfillment challenges, 33% say they would most like to improve this aspect in the following months.

Main Conclusions from Report

- Most respondents (59%) reported an increase in ecommerce orders in the past year.

- Approximately half of the respondents (51%) report an increase in fulfillment costs. The most significant factor was labor.

- The availability of free shipping is greater than that of fast shipping. For example, 43% of respondents offer free shipping on all orders, whereas 25% offer one- or two-day shipping.

- Many companies use multi-node distribution networks. For example, 17% of respondents have two distribution centers, while 22% have three.

- More than half of respondents (57%) use a third-party provider for some or all of their ecommerce fulfillment, and another 20% plan to outsource in the next 12 to 18 months.

- Most respondents plan to add new sales channels between 12 and 18 months, including third-party marketplaces (48%) and social platforms (41%).

- Mechanization, automation, and robotics are the aspects of fulfillment operations respondents wish to improve in the next 12 to 18 months.

- Fulfillment operations are becoming more strategic as respondents move forward. In addition to expanding distribution networks, optimizing for omnichannel, and reducing labor dependency, plans include increasing the use of technology.

To Sum up

Saddle Creek’s research shows how much the ecommerce landscape has changed since the COVID-19 pandemic, where it’s going, and what challenges today’s entrepreneurs face. Thus, the above report only confirms that online shopping is our future.