E-commerce in motion: Tracking Europe’s market momentum

E-commerce has grown significantly over the past decade, peaking during the pandemic before slowing in the post-pandemic market. While overall growth moderated in recent years, change is on the way. Find out more inside! (Ad)

(Image Source: www.pixabay.com)

Commercial collaboration

E-commerce has grown significantly over the past decade, peaking during the pandemic before slowing in the post-pandemic market. While overall growth moderated in recent years, trends like fast fashion and social commerce gained momentum, demanding agile supply chains and logistics. With strong growth expected to resume soon, it’s essential to examine this rapidly evolving sector’s current and future landscape.

E-commerce growth slowed in recent years but is now accelerating

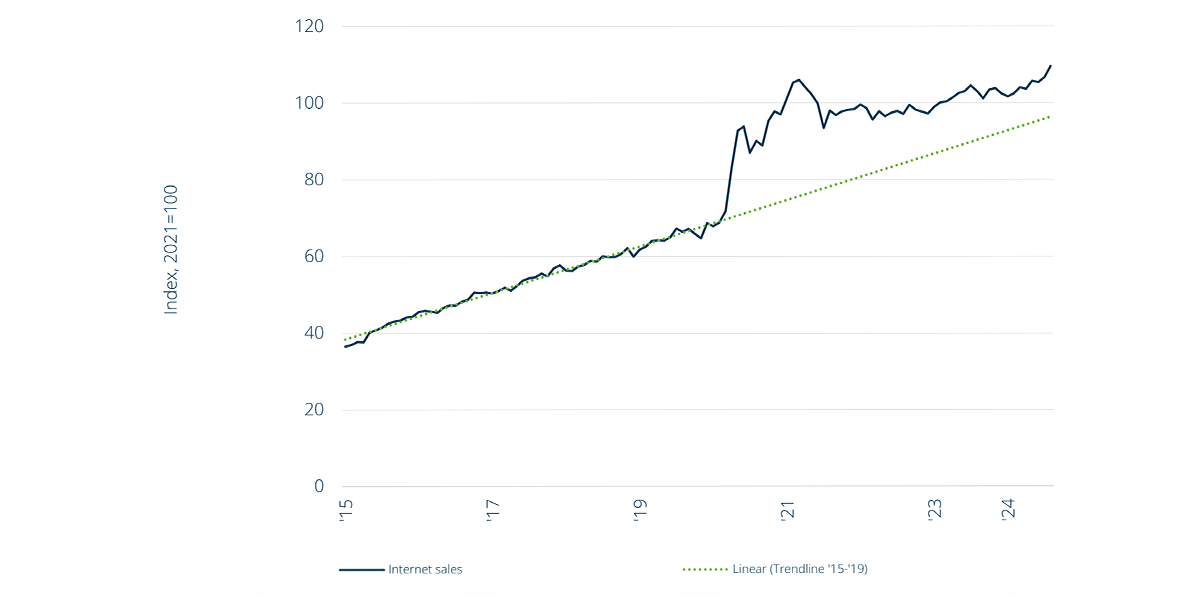

Exhibit 1: Monthly internet sales EU-8

Note: EU-8 total covers UK, DE, FR, NL, PL, ES, IT, SE. Weighted average based on total internet sales in 2023. Source: Eurostat, ONS, Green Street, Oxford Economics, CBRE

The pandemic accelerated around 2–3 years of e-commerce growth, causing a temporary slowdown as consumers returned to other purchasing channels and leisure activities once societies reopened. However, consumer spendings suffered even more because of the subsequent inflation shocks triggered by Russia’s war of aggression. However, this was not a long-term decline; sales continued growing at a more moderate pace. By July 2024, internet sales in the EU-8 (weighted average) surpassed any month during the pandemic for the first time.1 A key outcome of the pandemic was the faster rise of sectors like online groceries, while late adopters became more comfortable with online shopping. These new habits and trends are likely here to stay.

An evolution of growth and decline across sectors in the post-pandemic market

A fast-growing sector is fast fashion, providing affordable clothing that reflects current trends, exemplified by companies like Shein. In a short period, Shein has become Europe’s largest fast fashion online retailer, with online net sales in 2023 double those of the second-largest retailer, H&M. 2 The overall fast fashion industry has experienced significant growth in recent years and is expected to continue expanding, with a 7.5% compound annual growth rate (CAGR) forecasted for Europe from 2023 to 2030. 3 To support this growth, non-European fast fashion retailers are establishing European logistics infrastructures instead of relying solely on air freight. At the same time, public and media criticism is rising around overseas fast fashion retailers offering ultra-low-cost products, due to concerns about sustainability, tax regulations, and working conditions in factories.

Another fast-growing sector is social commerce, which involves the use of social media platforms for direct product or service sales, integrating social interaction with online shopping on platforms like TikTok and Instagram. Sales growth for social commerce in Europe is also expected to be robust, with a forecasted CAGR of 20.1% from 2024 to 2029. 4

Both fast fashion and social commerce have led to a faster turnaround of trends, placing a stronger emphasis on the agility of supply chains and logistics real estate, such as positioning products closer to consumers (as seen with Shein’s logistics facilities in Frankfurt and Poland) and increasing production in neighbouring European markets. Recent case studies show that countries like Turkey, Tunisia, and Morocco are increasingly targeted as manufacturing hubs by European fashion brands due to their proximity to European markets and shorter lead times. This shift is driven by the fast fashion sector’s need to reduce logistics costs, shorten time-to-market, and support more sustainable practices.

E-commerce is entering an inflection point and gradually returning to pre-pandemic growth levels

After the post-pandemic pause, early signs indicate that sales growth is returning to pre-pandemic levels. Based on a panel of 5 million e-shoppers, the latest figures from October 2024 show an increase in total e-commerce value (+8% y/y) and volume (+18% y/y) across the EU-5 countries (France, the United Kingdom, Germany, Italy, and Spain). 5

At a retailer level, early signs of accelerating logistics real estate leasing activity are expected in the coming quarters. This is already happening in the United States where Amazon has already re-engaged with higher activity. In Europe, this acceleration has not yet occurred. Amazon and other online retailers leased space ahead of demand (sales) during the pandemic and needed to absorb its existing footprint since the end of the pandemic first. However, growth of online sales of Amazon in Europe is in 2024 advancing at a faster rate than its relative footprint, a trend which was historically more aligned. 6 The current gap between sales and footprint growth is at record levels and this is expected to narrow leading to higher logistics space need. Furthermore, Amazon has announced extensive investments in both its digital division AWS and in small, consumer-oriented logistics properties. The background to this is the intentional adaptation of the sales strategy of Shein, and the associated changes for the real estate-side networks and locations.

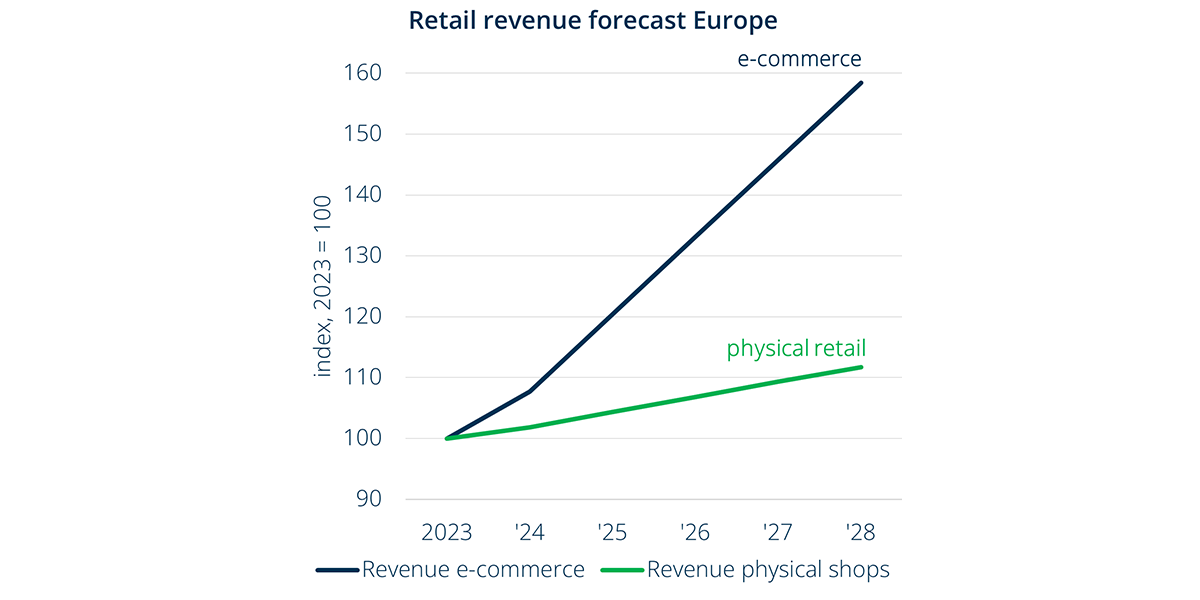

Double-digit sales growth is expected in the coming years

Exhibit 2: Retail revenue forecast EU-8

Note: EU-8 total covers UK, DE, FR, NL, PL, ES, IT, SE

Source: Green Street, Oxford Economics, CBRE

For the eight European markets (EU-8) the latest e- commerce outlook (published in October 2024) shows that e-commerce revenues are projected to return to double- digit growth during the period from 2025 to 2027. 7 This level of growth is similar to what was seen pre-pandemic, which was considered high. Compared to physical retail, e- commerce sales continue to outpace revenue forecasts, with a compound CAGR of 10.1% for e-commerce compared to 2.3% for physical retail from 2024 to 2028.

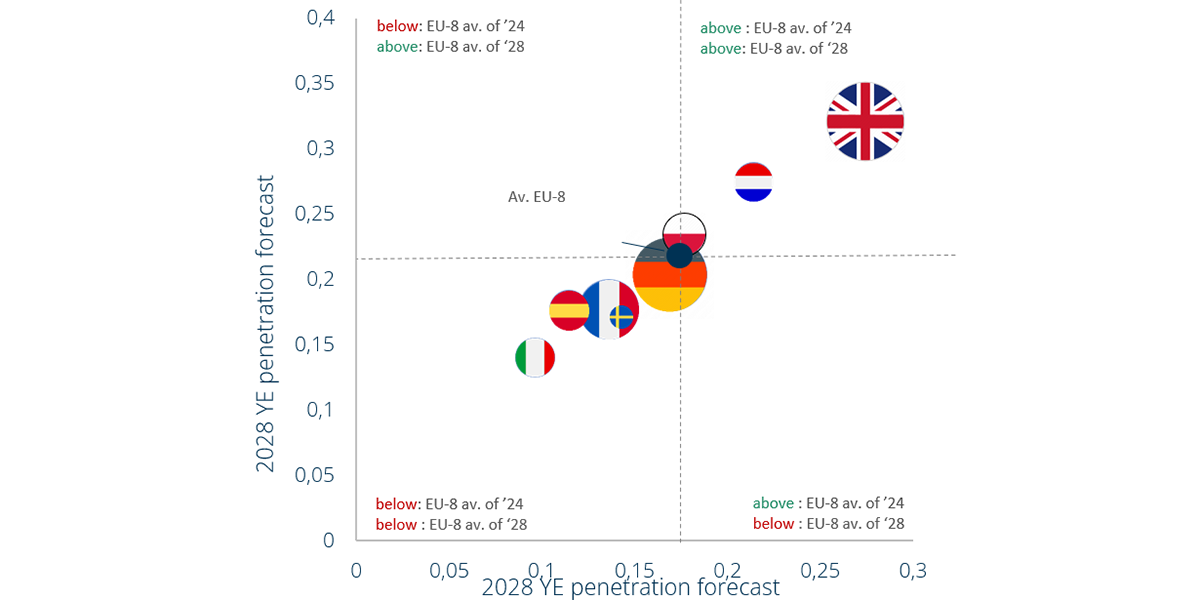

Penetration level comparison

Source: Green Street, Oxford Economics, CBRE

E-commerce penetration levels have started to rise again since 2022 and are forecasted to reach 17.4% by the end of this year. This is 10 bps above the level seen during the pandemic at year-end 2020, Over time, penetration is expected to gradually rise to 21.9% by YE 2028 in EU-8. 8 Countries like the United Kingdom and the Netherlands have been, are, and will remain the most advanced in terms of adoption and penetration levels. The United Kingdom is forecasted to reach a penetration level of 32% by YE 2028, not only the highest in Europe but also one of the highest in the world. 9 The top three countries projected to see the strongest increase in penetration from 2024 to 2028 are quite mixed, consisting of Poland (+7.1% to 23.5%), Spain (+7.1% to 17.7%), and the Netherlands (+6.9% to 27.5%).10

E-commerce is gaining an increasing share of the market, whilst logistics patterns are shifting

After a post-pandemic pause, e-commerce is showing signs of expansion, with indicators suggesting a gradual return to pre-pandemic growth levels. Fast fashion and social commerce are leading this resurgence, showcasing strong momentum. However, the mix of expanding sectors is shifting, and consumer habits evolve. This is expected to result in a stronger focus on a decentralized supply chain with smaller real estate satellite hubs focusing on urban proximity and logistics hotspots to better meet needs for accuracy, cost-effectiveness, and sustainability.

Selected factors shaping the transition of e-commerce supply chains

| Cost effectiveness: 50%11 total supply chain cost in last leg | The last leg of the e-commerce supply chain can account for 50% or more of total supply chain spending. Moving closer to end consumers saves drivers’ time and wage costs, requires less fuel, and optimizes van usage, despite higher rents for logistics real estate. |

| Predictability: 90-95%12 certainty in goods tracking before warehouse entry | Customer preferences for flexible and precise delivery times have pushed companies like DHL to leverage AI to predict delivery windows with 90%-95% accuracy. With this data, customers receive updates about delivery timing and can make real-time adjustments, resulting in higher satisfaction and fewer missed deliveries. |

| Accuracy: 60%13 key priority according to last mile delivery retailers in Europe | In the post-pandemic last-mile environment, retailers consider accuracy a more important success factor than speed, which is ranked second. This can be challenging, as the last-mile delivery market is expected to nearly double during the period from 2022 to 2027. |

| Carbon footprint: 1.5 to 2.9 times 14 more greenhouse gas emissions offline vs. online shopping in Europe | Offline shopping results in between 1.5 and 2.9 times more greenhouse gas emissions than online shopping. This is driven by more efficient traffic levels (vans vs. individual cars are 4 to 9 times less polluting), lower land use, and reduced building energy consumption. |

| Fresh products: 33% 15 of European consumers reported purchasing fresh food online | This growth trend underscores the need for supply chains and distribution hubs to be located closer to urban areas to ensure the freshness and timely delivery of perishable goods. |

| Bulkier items: 26% 16 of European consumers purchasing furniture/home decoration/ gardening last 3 months | The trend toward bulky items emphasizes that a single central distribution point may not be sufficient, as it is not economically feasible to transport larger goods over long distances. |

About the author

Tobias Kassner, Head of Research, GARBE Industrial Real Estate

www.garbe-industrial.de

Sources:

1 Source: Eurostat, ONS, Green Street, Oxford Economics, CBRE. Note: EU-8 total covers UK, DE, FR, NL, PL, ES, IT, SE. Average of EU-8 based on weighted average of total internet sales in 2023 in the eight countries

2 Source: ECDB

3 Source: Coherent Market Insights

4 Source: Research and Markets

5 Source: foxintelligence/NielsenIQ

6 Source: Green Street/Oxford Economics/CBRE

7 Source: Green Street/Oxford Economics/CBRE

8 Source: Green Street/Oxford Economics/CBRE

9 Source: Green Street/Oxford Economics/CBRE

10 Source: Green Street/Oxford Economics/CBRE

11 Source: Cushman & Wakefield

12 Source: DHL

13 Source: PWC

14 Source: Oliver Wyman

15 Source: Fooddrink Europe

16 Source: Ecommerce Europe

***