Global e-commerce overview: 2025 insights

Dive into our global e-commerce overview for 2025 and learn about the trends and insights that are going to influence the online shopping you already know.

Global e-commerce is no longer some kind of trend. It’s infrastructure. And it’s growing in new directions that matter for every retailer, manufacturer, or brand selling online.

We looked into SellersCommerce and the ECDB Global eCommerce 2025 whitepaper to bring you this overview. They dig into revenues, markets, growth rates, and customers. From inflation-adjusted growth to the rise of marketplaces and mobile commerce, the signals are clear: global e-commerce is stabilizing after years of shocks and setting a faster pace again.

Let’s look at what’s really happening — and what that means for you.

How big is global e-commerce in 2025?

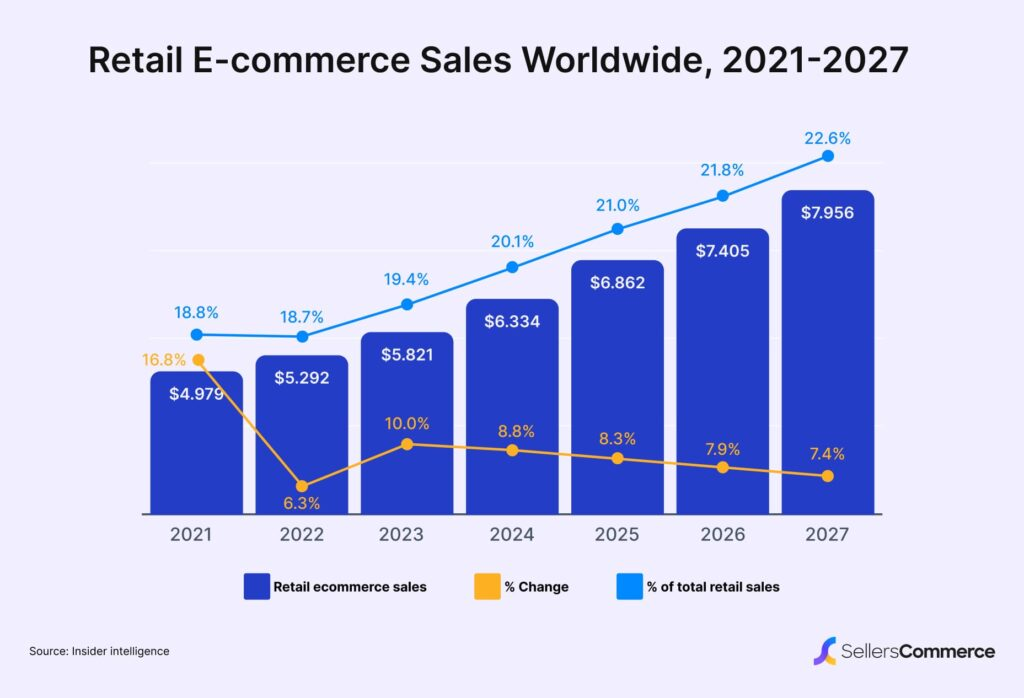

Let’s start with the money first. According to SellersCommerce, global e-commerce will surpass $6.86 trillion in 2025. That’s up 8.37% from 2024, and part of a steady climb that will take the market to nearly $8 trillion by 2027.

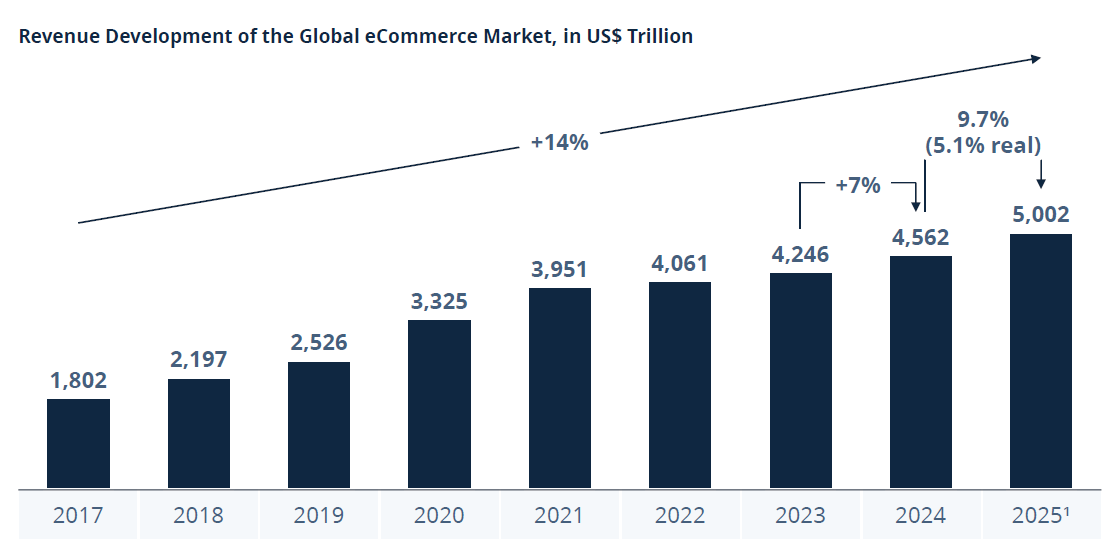

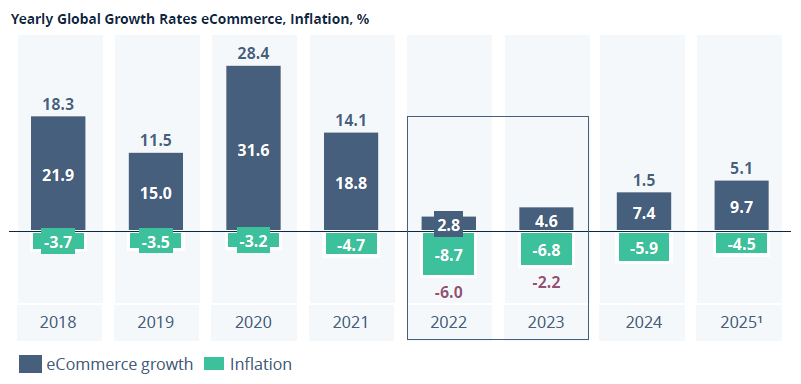

The ECDB report takes a narrower scope — just B2C physical goods (excluding services, B2B, C2C, returns, compensation for damaged or missing goods, any discounts granted, and digital products). Still, they project global revenue to exceed $5 trillion this year. That’s a 9.7% nominal growth, or 5.1% real growth after inflation.

That difference matters. In 2022 and 2023, inflation actually erased much of the market’s real gains. 2025 marks a return to actual growth — and that’s a major turning point.

Right now, 21% of all retail purchases happen online. By 2027, it’ll be 22.6%. And this isn’t just about the total spend. It’s about frequency, access, and digital-first behavior becoming the norm. There are 2.77 billion online shoppers globally — around 33% of the global population. In 2026, that number will climb again.

China leads, with 904.6 million shoppers. The U.S. is next with 288 million. But the growth is more distributed than ever. New markets are catching up fast, driven by mobile access, social commerce, and fast international shipping.

So what does this mean for your business?

That online isn’t optional.

But growth doesn’t come from simply being present. You need to know where it’s happening, how fast it’s shifting, and what your buyers expect from the experience.

Where is growth happening?

It’s not evenly spread — and that’s the whole point. It’s more regional, strategic, and often surprising.

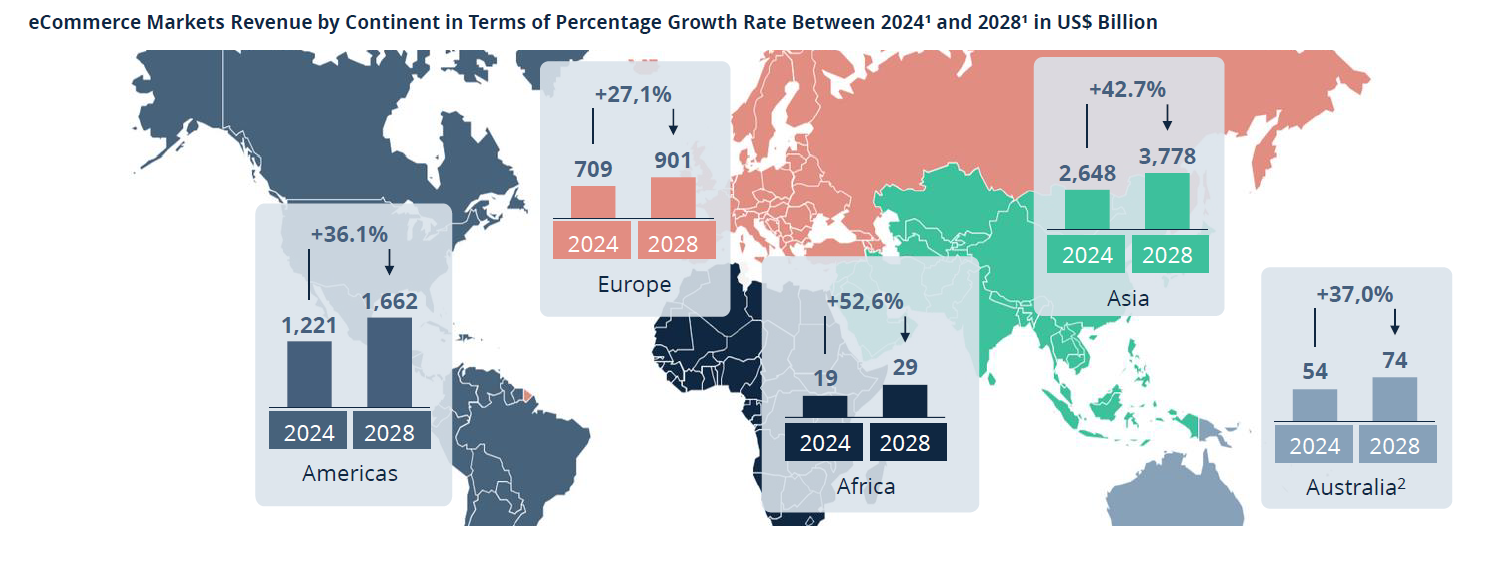

Let’s start with the raw numbers. According to ECDB, the fastest-growing continent between 2024 and 2028 is Africa, with a projected +52.6% growth. That’s followed by Asia at +42.7%, thanks to its scale and digital-first shopping habits. Australia and Oceania sit at +37%, and the Americas grow by 36.1%. Europe trails slightly behind, with +27.1% growth, reflecting the region’s maturity and slower adoption curve in certain countries.

But growth isn’t just about revenue volume – more about pace.

The 2024 growth champions in percentage terms? Poland and Brazil. Both countries saw a sharp spike in nominal growth year over year. Sure, they’re not the biggest markets — but they’re climbing fast. Sellers who catch those waves early have more space to build brand loyalty and grab market share.

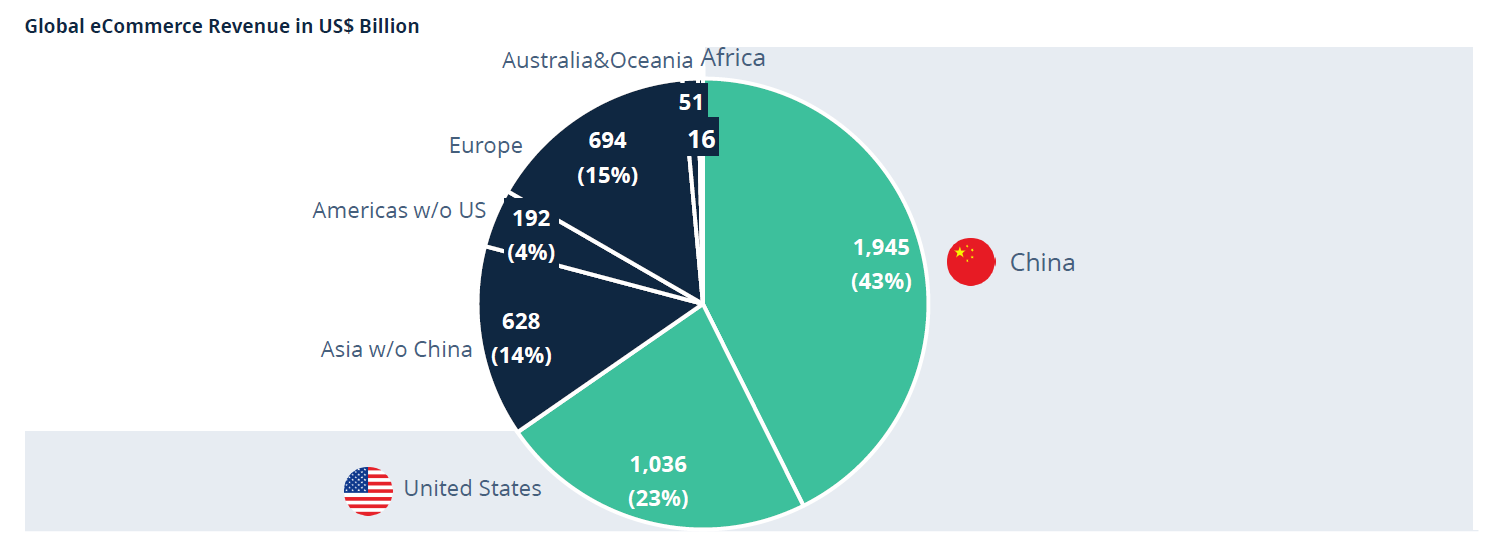

Meanwhile, China and the U.S. remain dominant in terms of revenue, contributing nearly 70% of global e-commerce spend in 2024. But their growth curves have shifted. China’s peak growth came earlier, in 2020–2021. The U.S. saw its biggest spike in 2022. Now, both markets are stabilizing at slower but still healthy rates, and that opens the door for other players.

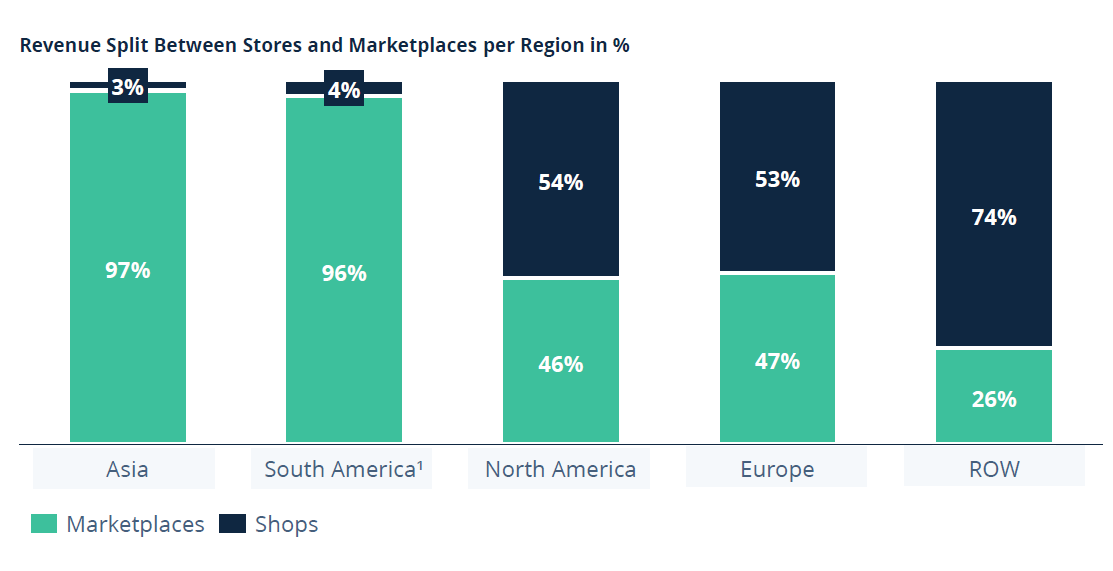

There’s also a shift in how buyers reach products. 72% of global e-commerce revenue comes from marketplaces. And that number is higher in high-growth areas. Asia sees 97% of its online revenue flow through marketplaces. In South and Middle America, that figure is 96%. Buyers in these markets rely on platforms like Shopee, MercadoLibre, and JD.com to find, compare, and trust what they buy.

Contrast that with Europe and North America, where online shops still hold a stronger position. In these regions, brand-owned stores and DTC models are more common, and marketplaces are a secondary channel — though that balance is shifting.

Another signal: more businesses are entering the game.

According to SellersCommerce, there are now over 28 million e-commerce websites globally, up 2.9% from last year. That’s about 2,100 new stores launched every day. Half of them are based in the U.S., but growth is happening everywhere.

So if you’re expanding or optimizing — look where growth is rising, not just where the money already is. The next five years will reward those who bet early on the right markets.

Who’s shopping — and how?

Now let’s move to behavior. Because knowing who shops is only half the story. The other half is how — and why.

So there are 2.77 billion online shoppers around the world. But what they do varies wildly by device, platform, and habit.

One constant: the move to mobile. In the U.S., 73% shop on their phones. In India, that jumps to 88%. In China, it’s 92%. Do you see it now? phones are the primary device for digital commerce, not just for browsing, but for full checkouts and repeat purchases.

That’s backed by spend. Mobile commerce is expected to hit $2.51 trillion in 2025, up more than 21% from the previous year. That’s more than half of all global e-commerce revenue.

But, of course, it’s not just about phones.

Shopping is getting faster, more frequent, and more casual. 34% of shoppers make online purchases at least once a week. The weekend bump is still real, but the behavior is always-on now. And that leads us to a key shift: platform-native buying.

Going further, 40% of U.S. shoppers have used live commerce. That number is even higher in parts of Asia and Latin America. Think livestream shopping, real-time demos, instant purchasing links. It’s interactive, fast, and social — and it’s catching on.

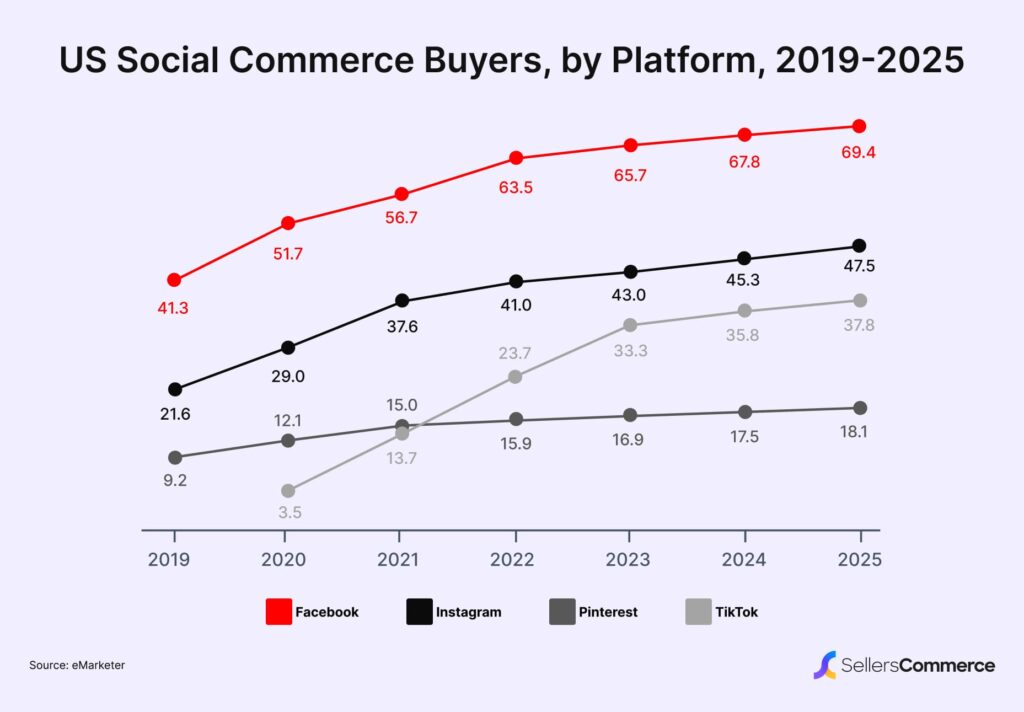

And social commerce? It is its own beast. It’s expected to hit $2.9 trillion by 2026. Platforms like Facebook, Instagram, and TikTok are driving this shift. In the U.S. alone, 69.4 million people shop on Facebook, 47.5 million on Instagram, and nearly 38 million shop on TikTok. Pinterest, while smaller, is growing fast in this space too.

What are people buying online in 2025?

The category split in 2025 shows what people care about:

- convenience,

- personal style,

- daily essentials,

- and hobbies.

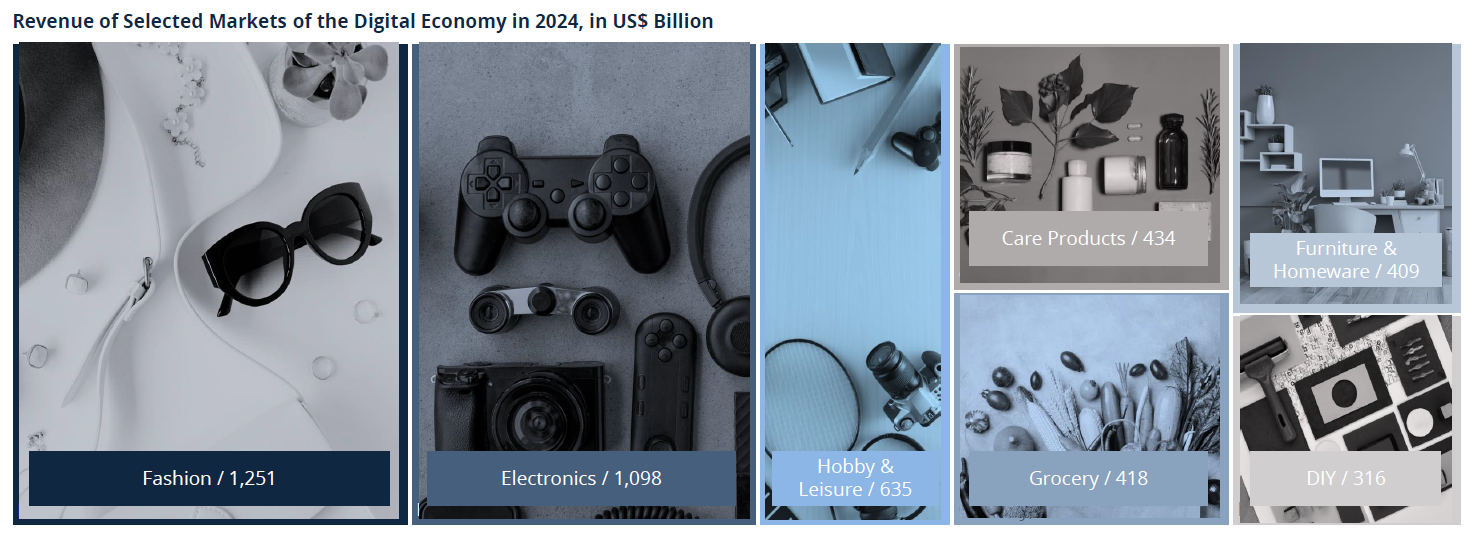

But the revenue also shows what’s becoming essential in the digital shelf. Let’s start with the top earners. According to the ECDB report, the #1 revenue category globally is:

01 fashion, $1.251 trillion in online sales in 2024

That includes clothing, shoes, and accessories. What’s driving this? Fast inventory turnover, brand loyalty, and a shopper habit that’s already digital-first. Next up:

02 consumer electronics, $1.098 trillion

Smartphones, laptops, headphones, smart home tech — they’re daily tools. They also have some of the highest review-read rates, which makes product trust and detail pages critical. From there, we get into a mix of functional and feel-good categories:

03 Hobby and leisure, $635 billion

It mixes gaming, sports, musical instruments, toys, and crafts. The growth here reflects a deeper lifestyle shift. People are spending more time at home and are willing to invest in what keeps them engaged. What’s next?

04 Care products, $434 billion

Including beauty and personal care. These are smaller-ticket items but high in frequency. Especially in social commerce, self-care wins. 19% of shoppers say they’ve frequently purchased health and wellness products via social platforms, with another 42% doing so occasionally.

Grocery and food is also climbing steadily online. Add in furniture & homeware and DIY products, and you see how global e-commerce has moved fully into everyday life.

However, category preference also depends on region. The UK, for example, has a stronger share of hobby and leisure, while Asia’s category split leans more toward electronics and grocery. These differences matter if you’re expanding into new markets.

What drives purchases — or stops them?

The motivations behind a click (or an abandoned cart) are sharper than ever. People shop online because it’s easier. But the moment something gets in the way, they’re gone.

Top motivator? Free delivery.

SellersCommerce found that 50.6% of shoppers cite it as the reason they buy online. Right behind it are:

- coupons and discounts (39.3%),

- easy return policies (33.2%),

- simple checkout (30.6%),

- next-day delivery (30.4%),

- Loyalty points (27.2%).

What’s crucial, reviews still matter… more than ever.

Can you imagine that even 99% of shoppers look at reviews, and 96% actively search for negative ones? That’s not a red flag — it’s trust-checking. Social proof doesn’t just happen on product pages anymore. Facebook reviews drive up to 40x more conversions than posts without them.

So what causes people to bounce? Cart abandonment is at 70% globally, and the top reason is still unexpected costs at checkout.

Hidden shipping fees, taxes, and forced account sign-ups are dealbreakers. A slow or unclear delivery estimate also sends buyers away. Moreover, 25% drop out if forced to create an account, and 24% leave due to slow shipping timelines.

The gap between browsing and buying isn’t deep. Sometimes it comes down to a shipping promise, a visible review, or a two-step checkout. Miss those, and your customers’s already somewhere else.

E-commerce models and platform trends

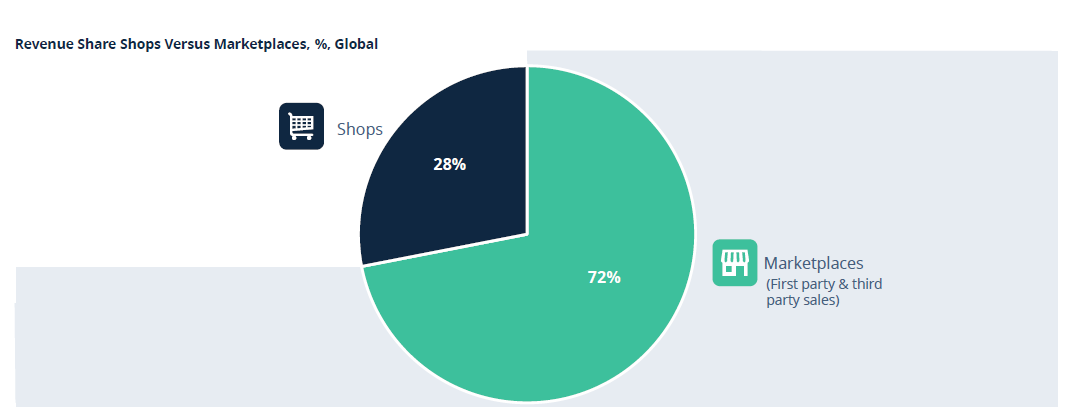

According to ECDB, 72% of global e-commerce revenue is now going through marketplaces. That includes both first-party and third-party sales. The remaining 28% happens on brand-owned or standalone online stores.

But as always, this split isn’t global in the same way. In Asia, marketplaces dominate, too. Think Taobao, JD.com, Shopee, Douyin, and Pinduoduo. In that region, 97% of all e-commerce revenue comes through marketplaces. In South and Middle America, it’s 96%. Yet, in North America and Europe, the split is more balanced.

In fact, brand websites still hold a stronger position in some sectors, especially fashion, wellness, and high-end consumer products.

And who’s winning on the marketplace leaderboard? No surprise here: Amazon leads with a massive $798 billion GMV in 2024. That’s nearly double the second-place platform, Pinduoduo, which hit $656 billion. After that come Douyin ($568B), JD.com ($498B), Taobao ($490B), and Tmall ($487B) — all Chinese platforms.

Further down the list are Kwai Shop, Shopee, and eBay. Each serves a distinct audience. Shopee, for instance, leads in Southeast Asia. eBay’s power lies in secondhand and niche categories.

At the same time, subscription models are creating hybrid strategies. Some brands sell through Amazon and run a recurring box through their own site. Flexibility is key. In this way, the subscription e-commerce sector is set to hit $450 billion by the end of 2025.

So if you’re building a model, think in layers.

What’s next for global e-commerce?

ECDB projects that the real growth is back, with a 5.1% growth rate in 2025, adjusted for inflation. That matters after two years, where inflation made even strong revenue gains feel flat. Sellers now see actual gains, not just inflated numbers.

Another highlight: people want proof over promises. 80% of consumers say they trust brands that back sustainability claims with real, public data. Green labels aren’t enough anymore. What matters is whether your ESG goals are measurable and visible.

Then there’s AR shopping. Right now, 32% of online buyers use augmented reality tools to test products. And 40% say they’d pay more for a product if they could preview it through AR. This is especially strong in furniture, cosmetics, and fashion. Younger shoppers lead the way, but adoption is widening.

Automation is also reshaping back-end operations. The most successful e-commerce companies are the ones using automated tools for inventory, customer service, and marketing. SellersCommerce notes that 72% of high-growth e-commerce brands already use automation in some form, and they’ve seen up to 80% boosts in lead generation.

Expect to see more of this on the customer side, too. Chatbots, AI product recommenders, and dynamic pricing — these tools are becoming plug-and-play for small and mid-sized brands.

And behind it all? Data. 78% of marketers now rely on data-driven decision-making for customer engagement. Who buys, how often, when, and through which channel. If you can read the signals, you can shape the sale.

Conclusion

If you’re selling online in 2025, you’re not early. You’re not too late either. But you are in the middle of something big, and what you do next matters.

The global e-commerce is driven by experience, speed, trust, and smart strategy. Global revenue is climbing, mobile dominates, marketplaces are the backbone in most regions, and shoppers are clearer than ever about what they want.

You shouldn’t launch a new business fast or chase all trends. First, you need to understand what works and where. Know which markets are opening up. Which platforms your customers actually use. And what makes someone choose you over the next tab.

So whether you’re selling through Amazon or building your own store, whether you’re targeting France, Mexico, or Southeast Asia — you’re working inside a system that’s huge, fast, and very real.

Global e-commerce is wide open. And it rewards those who build with clarity. So let’s keep building.

***