How embedded payments are changing the face of B2B commerce

– Article prepared by TreviPay –

Customer expectations of payments are changing. While the adoption of traditional credit cards by consumers remains lower in Germany than many other European countries, the trend for the next few years remains a constant upward trajectory and alternative payment options based on credit are emerging.

The appeal of Buy Now Pay Later (BNPL) propositions have grown quickly across Europe. In Germany, BNPL was around 10 times higher than the penetration rate achieved in the United States.

To capitalise on this consumer trend, Barclaycard has announced a partnership with Amazon Germany to offer instalment lending for eligible purchases over €100.

The huge opportunity for B2B differentiation

According to data from JPMorgan Chase, the German B2B e-commerce market is the third largest in Europe behind France and the UK and is projected to be valued at over €130 billion in 2023. With such scale and competition, the BNPL offerings that are gaining popularity with European consumers presents a huge opportunity for German B2B providers of goods and services to differentiate themselves.

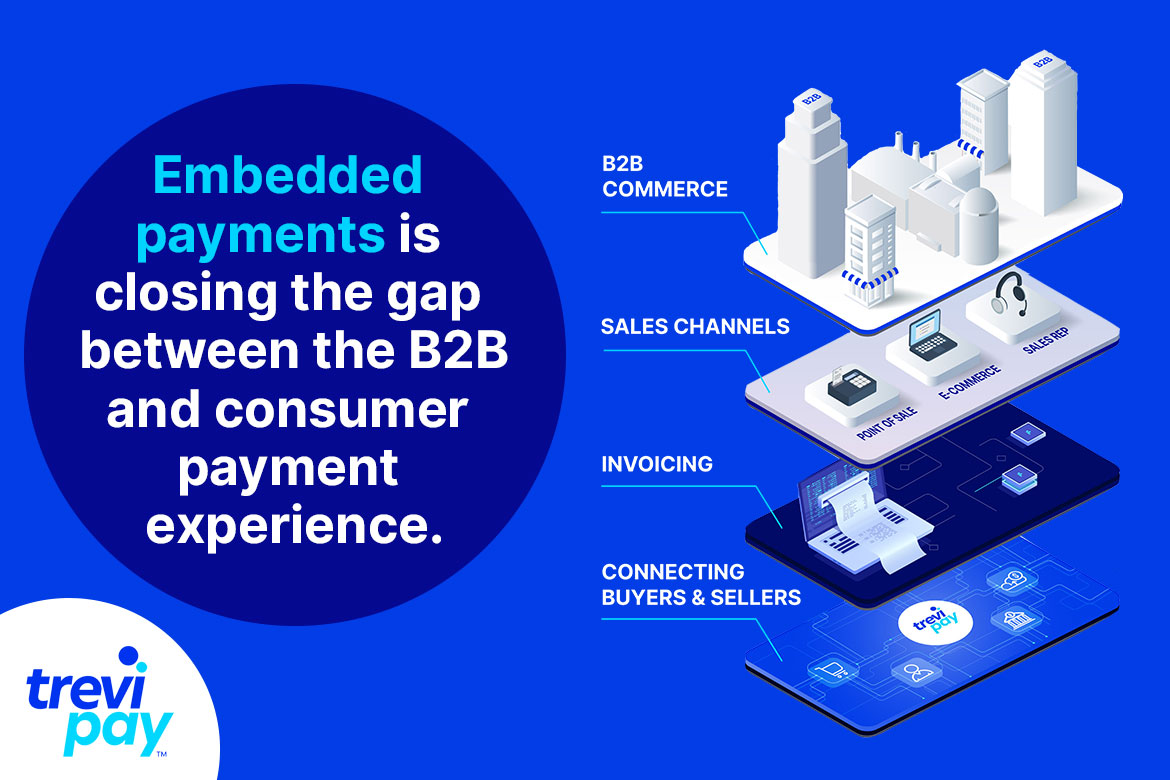

How can B2B merchants capitalise on the trend towards payment?

For providers of B2B goods and services, payment concepts are evolving rapidly to meet and exceed changing buyer expectations. Simplicity, choice and convenience are the benefits of embedded payments and it’s closing the gap between the B2B and consumer payment experience.

A brief history of embedded payments

Embedded payments have become the norm for consumers since the early days of Uber.

Uber’s business model and practices earned much attention for establishing new ways of operating, its frictionless payments experience for customers is among the most innovative and what really deserves the recognition. Just consider the difference in the user experience between the traditional taxi and Uber experience. In the former, the customer has the inconvenience of digging around for a card or cash to pay the driver before they can leave the cab. With Uber, the customer can jump out immediately and be on their way.

It’s important to remember that everyday consumers, like those who use Uber, can also be B2B buyers. So, it’s not surprising that B2B buyer expectations have also grown, and in a short period of time.

“Three years of consumer behaviour change was squeezed into one year in 2020”, wrote Forrester Principal Analyst Jay McBain.

“Consumers are now demanding online experiences, happily virtual, wanting seamless digital procurement and provisioning, and wanting everything at the click of a button. The delta between B2C buyers and B2B buyers has collapsed during the pandemic. It’s all about speed, convenience, and remote, whether the buyer is acquiring a Peloton or a software product”, McBain adds.

Providers of B2B goods and services are waking up to the fact that customers of all types have migrated to a digital-first buying behaviour. That means it’s only a matter of time before customers (both B2B and B2C) turn their backs on companies that do not live up to their expectations of a seamless, convenient payments experience.

Embedded payments can enable that invisibility and help B2B companies attract and retain customers, but it’s important to work with a partner who can help get it right. Here are some things to consider when it comes to integrating an embedded payments solution:

The needs of B2B customers are more complicated than those of traditional consumers

B2B transactions are more complex than their B2C equivalents. B2C transactions usually involve a single buyer using a single payment method, such as a debit or credit card.

A B2B transaction can involve several stakeholders. There will be the purchaser and then possibly the budget holder, the procurement and accounts payable teams, as well as many different payment options, like trade credit, purchasing cards, and credit cards, among others. It’s vital to make sure your embedded payments solution meets the needs of each stakeholder in the process.

Done correctly, an embedded payments solution will improve your cashflow by allowing buyers to receive invoices daily, weekly, or monthly and make payments on terms that they control. It’s also vital to allow data, such as PO numbers, to be added to invoices and support integrations into an enterprise resource planning or procure to pay platform like Tipalti.

While embedded payments require a significant amount of behind-the-scenes orchestration, the speed and ease in which transactions take place can be transformational.

Benefits for all – including the A/R team

A key deliverable of an embedded payment solution for B2B merchants is the implementation of a completely digital and automated onboarding experience into theirA/R process.

By eliminating mundane day-to-day tasks, A/R can move into a more strategic role. More merchants are realising that B2B A/R teams are customer-focused, with an emphasis on loyalty-building payment experiences—even when dealing with late-paying clients. In fact, 58% of finance leaders now participate on their organisation’s customer experience team, according to a 2021 Harvard Business Review Survey of over 1,000 executives.

The reality is that A/R typically has the most customer touchpoints. They are in regular communication with customers from onboarding through every order. If a customer’s account is seriously past-due, it’s typically the AR team that determines when to sever the relationship. In many cases, they may own your customer’s entire experience with the organisation. Digitisation can deliver transformational benefits across a merchant’s business.

Research shows that the majority (63%) of salespeople’s time is focused on activities other than selling —meaning only 37% of a sales team’s time is bringing in new business. Merchants can save time and money through this automation by eliminating the need to email forms, wait days for credit decisions, and perform manual bank reconciliations.

Instant decisioning and credit builds revenue and loyalty

By embedding payments, such as the ability to offer a line of credit to customers, can have immediate and measurable results. It will not only encourage increased order value but should make a merchant easier to do business with by letting the buyer interact, and transact, on their preferred terms.

It’s likely that merchants will find that their business customers prefer to purchase using trade credit and spend more with a business when they have a dedicated financial relationship and credit line.

Customers can easily purchase more stock when they need it, and merchants know that buyers are likely to return. It’s important that the credit issuance experience is quick and instantaneous. In the move to digital-first interactions, instant decisioning is essential and can be a make it or break it feature in the sales process.

The idea of offering trade credit to customers may however seem intimidating for merchants. As part of an embedded payments solution, the risk assessment and underwriting of the credit can be outsourced to a third-party.

A brief case study: Hospitality

An embedding payments strategy can create a competitive advantage for hotel chains. The ability to offer a line of credit and payment on terms can make the hotel chain easier to do business as the digital checkout removes the friction for both the corporate traveller and the A/R department by integrating the digital billing and payments process.

That is likely to mean higher levels of repeat business, long-term loyalty and profitability. Because the hotel is paid by the supplier rather than its clients, once the line of credit is in place, gone is the need for resources to chase unpaid invoices.

All expenses for all travellers are consolidated within a single invoice, drastically reducing the internal resources required to manage finance processes. The client can access folios in real-time so they can monitor where their travellers are staying as well as individual spending data.

When the client’s workers are ready to check out, there is no need for a card. They are free from the administrative burden of tracking, reconciliation and reporting their business expenses and the inconvenience of waiting for payment.

The right partner can help protect against business identity theft and fraud

Business identity theft and other forms of digital fraud are on the rise in response to the growing use of online channels globally. Merchants with a growing business must be especially cautious to manage the risk associated with invoice fraud as they find themselves with more vendors to pay and invoices to process.

When implementing an embedded payments strategy, finding a partner with a strong track record of risk decisioning and fraud detection is critical. When evaluating a partner, it is also advisable to check how long they have been in business to avoid choosing an inexperienced supplier.

To stay relevant and keep ahead of customer needs, B2B merchants must stay abreast of trends in consumer commerce. B2B customers will inevitably bring their expectations as consumers into their B2B purchasing experience.

B2B merchants who are looking to grow their revenue, increase customer loyalty and stand out from the competition should view recent European consumer payment trends as signpost for where their B2B payments experience should be heading.