How Zalando’s acquisition of About You affects German market dynamics

Zalando’s acquisition of About You marks a strategic shift in German eCommerce, consolidating its dominance in the fashion sector while Otto continues to struggle with stagnation amid fierce competition from Amazon and emerging low-cost marketplaces. (Ad)

Commercial collaboration

By Nadine Koutsou-Wehling, Data Journalist at ECDB

Shifts in German eCommerce have made headlines at the end of 2024: Fashion retailer Zalando is acquiring About You from Otto. The changes involve Germany’s largest domestic eCommerce retailers, which prompted us at ECDB to take a look at the underlying market dynamics.

Few things are clear: Amazon is the undisputed number one, with no plausible risk of being overtaken by any of the other leading retailers. At the same time, the German mail-order company Otto has been stagnating for years, while Zalando is on an expansion course, especially with the recent acquisition of its closest competitor.

All these shifts are happening at the same time that marketplaces with either a low price offering (AliExpress) or a high audience appeal (TikTok Shop) have entered the game. What does all of this mean for German eCommerce?

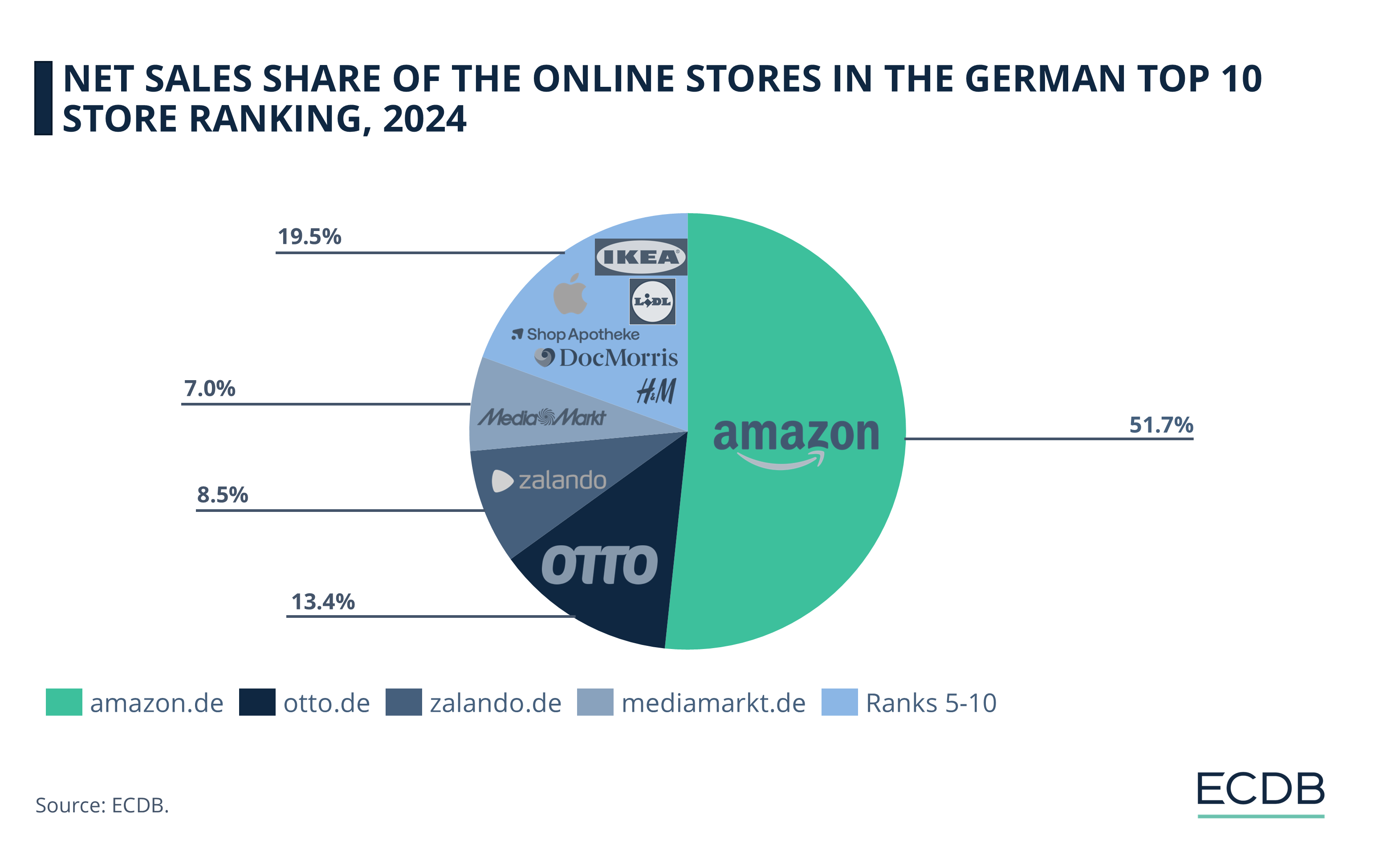

Amazon stands alone at the top of German e-commerce

A visual representation of the market shares within the top 10 online store rankings in Germany illustrates Amazon’s outsized position compared to the other rankings. When the total online store revenues of the top 10 players in German eCommerce are depicted, Amazon accounted for 51.7% in 2024.

This shows that even if the top three German eCommerce companies (Otto, Zalando with About You, and MediaMarkt with Saturn) were to merge, they would not be able to seriously challenge Amazon’s market dominance. Even in a scenario where all subsidiaries are included, their market share would not reach Amazon’s leading figures.

And this is just considering the online store: Including Amazon Marketplace, with its consistently high GMV, would increase its lead even further. With or without the marketplace, Amazon is number one in German eCommerce, as it is in many other comparable markets such as the U.S., UK, Canada, and France.

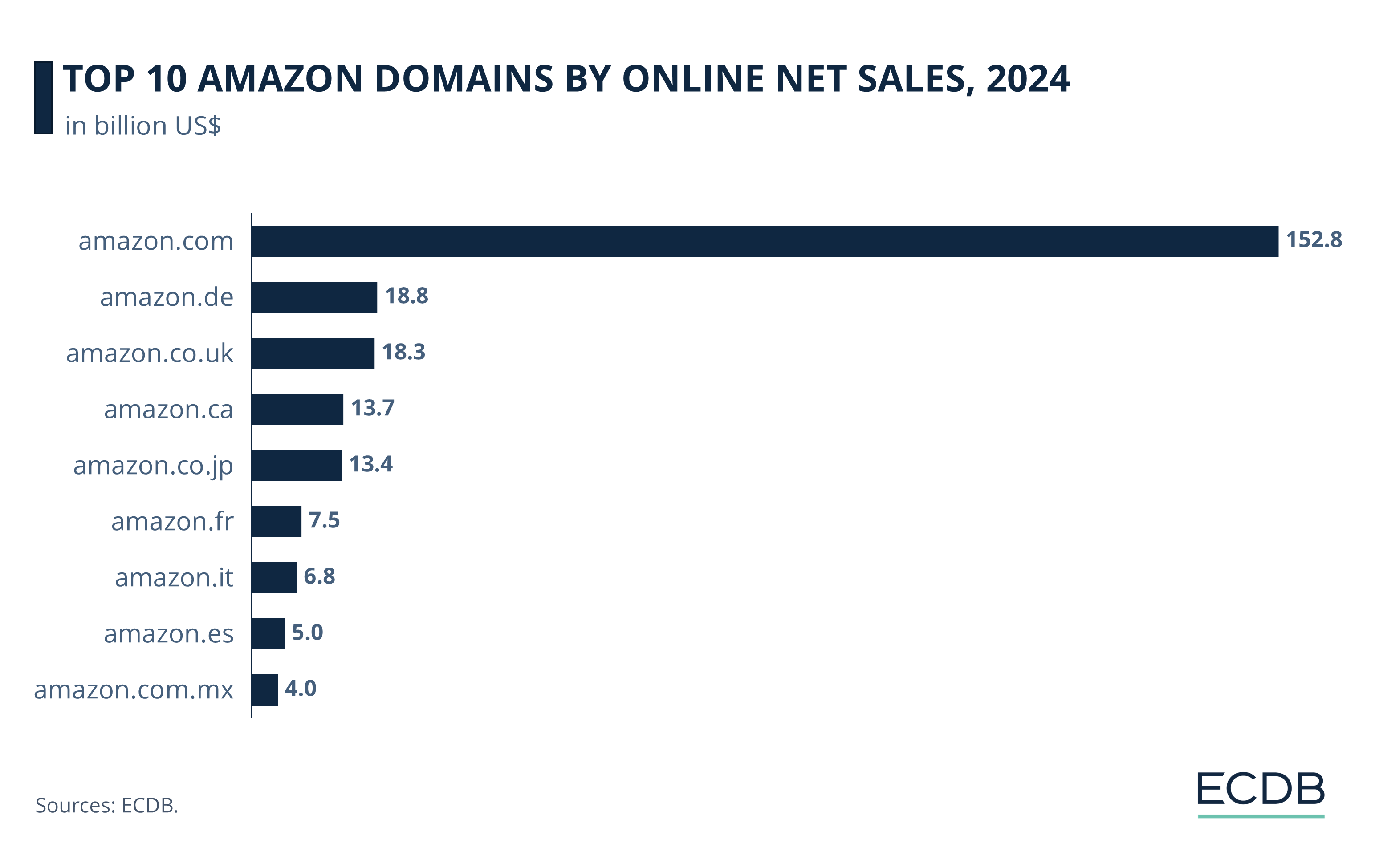

Amazon is the no. 1 retailer in each of its top markets

The top 10 Amazon domains by online store revenue reflect Amazon’s top regions – the U.S. domain amazon.com is by far the leading store. But even for Amazon’s weaker domains, Amazon is the dominant eCommerce retailer in each market.

This is true for all of the top 10 markets shown in the chart. While US$18.8 billion on amazon.de are far from the US$152.8 billion that amazon.com generated in 2024, it is still a long shot from the figures other retailers generate. Amazon.co.uk and amazon.de are very similar in size, as is the economic power of the respective countries in which these domains operate. Amazon.ca and amazon.co.jp follow with comparable revenues of about US$13.5 billion.

Next are the smaller but still significant markets of France, Italy, Spain, and Mexico. In each of these countries, Amazon is again the number one online store.

With Amazon’s outstanding performance across domains and countries, it seems that other retailers in the industry have no choice but to accept defeat.

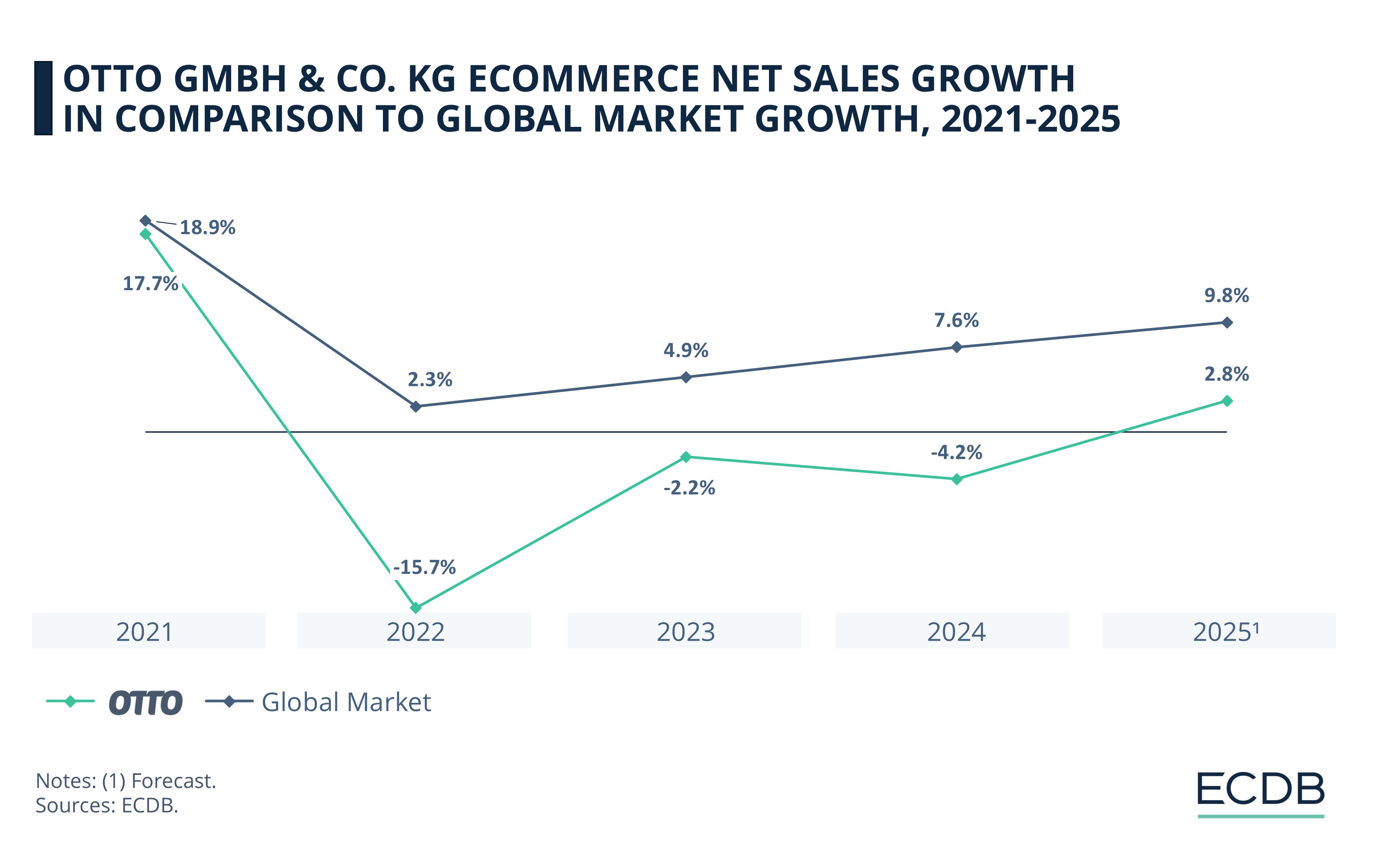

Otto’s lack of differentiation is an obstacle

Otto GmbH & Co. KG was the leading mail order company in Germany before the advent of the online economy. With the development of eCommerce, its approach has lagged behind, although it remains one of the most recognized retailers in the country.

In comparison to the growth rate development of eCommerce, Otto has been on a consistently lower path. While the pandemic years accounted for higher demand and overall willingness to buy products online, the subsequent years were riddled with economic pressures, consumer uncertainty and growing competition in the online market.

Amazon offers everything Otto does and more, especially in terms of consumer convenience. For this reason, it is difficult for Otto to differentiate itself enough for consumers to consistently choose Otto over comparable retailers.

The aspect of differentiation is a big one: Due to the highly competitive nature of global eCommerce, where Germany is deeply connected through its economic relations, differentiation is one of the core necessities to remain relevant in shifting market conditions.

A look at Otto GmbH & Co. KG’s portfolio of online subsidiaries further makes it clear that the company’s domains are various, but only a few generate enough revenue to sustain growth. Especially in the coming years, the outlook for Otto’s journey in the online market is challenging. Now that Zalando is acquiring Otto’s second-largest store, About You, it is likely to tilt the balance towards the former.

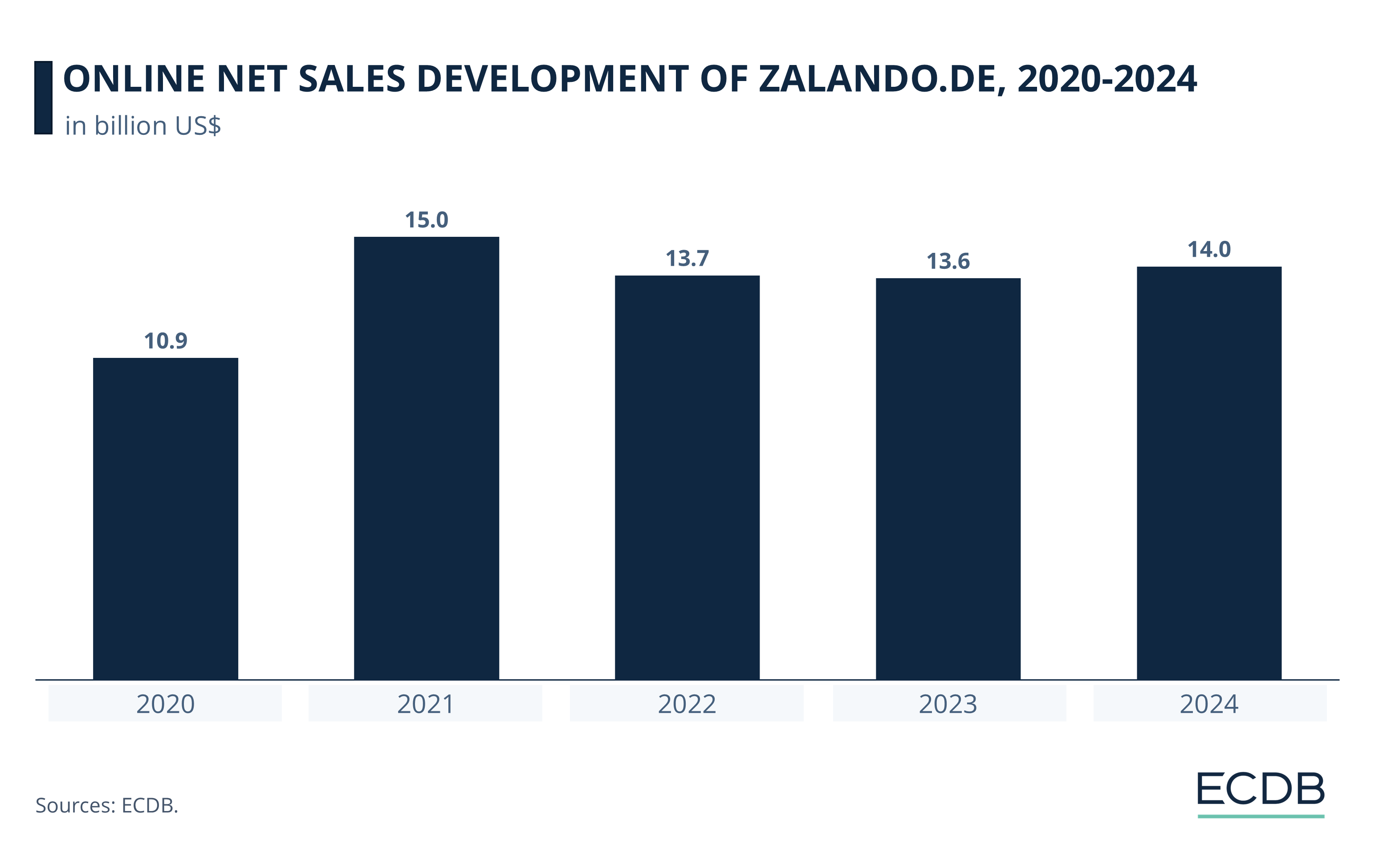

Zalando meets global fashion dynamics with merger

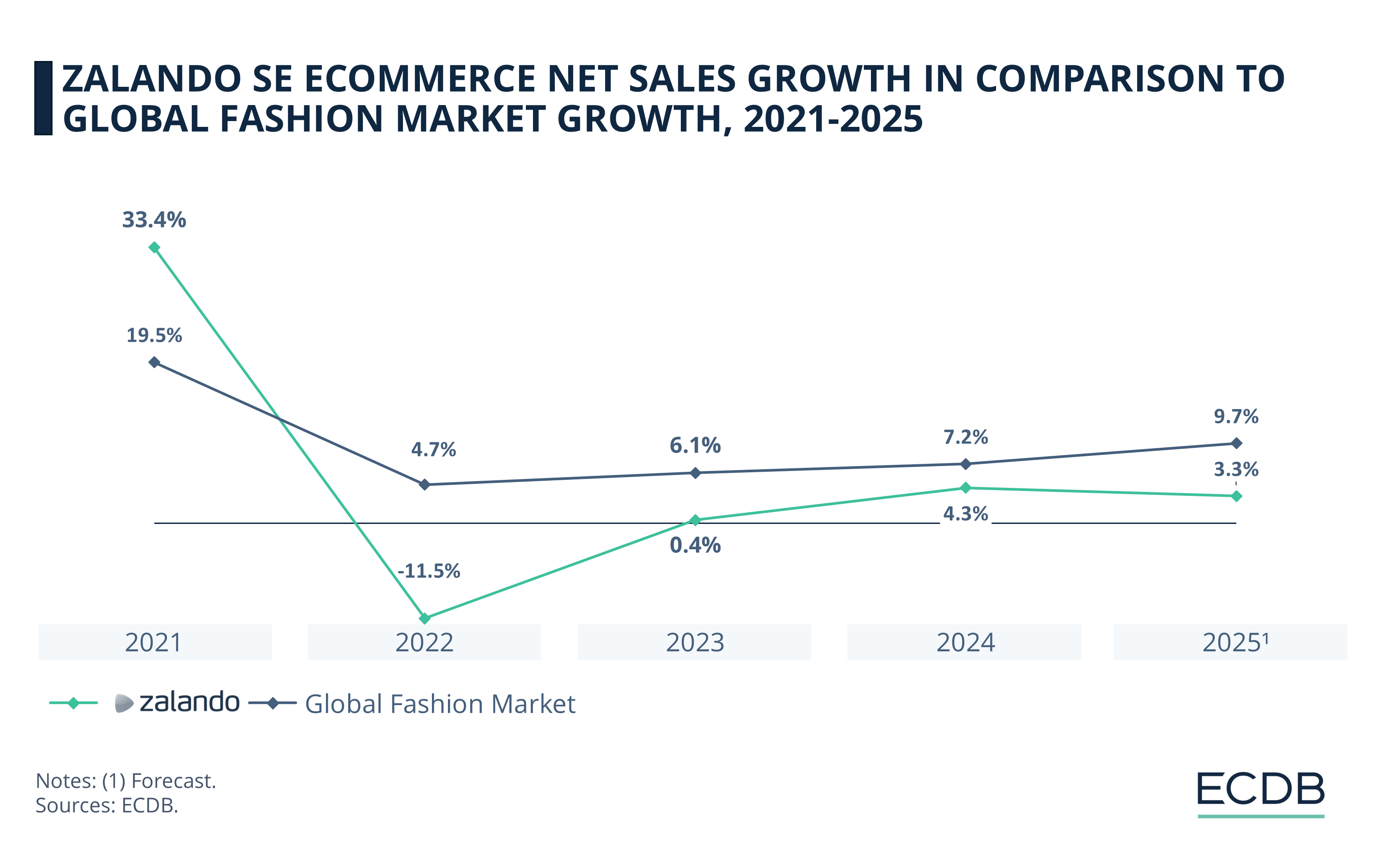

For an online store to be consistently chosen over the market leader Amazon, it must have a distinct offering and its own set of perks and conveniences. Zalando averted a sharp decline in online net sales after the pandemic, when consumers typically returned to physical stores or shopped less frequently.

Online net sales on zalando.de were around US$14 billion from 2022 to 2024. By acquiring its closest rival, About You, Zalando is killing two birds with one stone: Extending its lead in the German fashion market and covering more European destinations at once.

Zalando.de is the number one online store in German fashion eCommerce. It beats both otto.de and amazon.de in second and third place, respectively. And why is that? Because Zalando has a differentiating factor that makes more consumers want to shop their fashion items at Zalando, rather than Amazon (or Otto, for that matter).

Compared to the global fashion market, Zalando SE revenues have experienced higher peaks and steeper declines, but have remained closer to global developments than Otto’s.

Frequent style updates, styling ideas, a virtual shopping assistant, extensive marketing to stay top of mind, wide price ranges with large assortments: Online shoppers visit Zalando with the clear intention of finding new clothes, and the site’s service helps them do just that, with convenient returns to try on pieces at home and pay as they go.

Its closest competitor, About You, is now being integrated into Zalando’s operations. In this way, the two most influential online fashion stores in German eCommerce are merging: While their total net sales still don’t approach Amazon’s lead in this regard, it’s the next best thing other retailers can hope for in a market where Amazon has taken over.

Outlook: What’s next for German e-commerce?

Some developments are global, as is the emergence of low-cost online platforms that are challenging established online stores with larger assortments and more competitive prices.

Their competitive edge is enabled by the use of technology that allows them to respond more quickly to global trends, which is a more modern way of updating product assortments than the retail chain of the past century. Literally, this is called the LATR (large-scale automated test and re-order) model, which originated with Chinese innovators and has recently been introduced to European and American markets. It saves cost and time, two factors that have caused a global stir as retailers scramble to adapt their approach.

The current rollout of TikTok Shop across Europe, most recently in Germany, France and Italy, is indicative of how world trends become global phenomena. Amazon has little to fear, given its pre-eminent position in online markets. Neither do Zalando (and Otto, for the time being). The companies who are most affected by these developments are the smaller ones with little to no differentiation at the bottom of the rankings.

***