Key Takeaways on Investing in an Age of Transformation [BNP Paribas report]

The world is in the midst of a transformation characterized by surging inflation and fundamental shifts in geopolitical power. Green transformation is taking place, we observe the global economy, and we focus on sustainable long-term growth.

In today’s article, we will provide investors with a lot of information that will guide them at a pivotal time for the global economy. Read the BNP Paribas report here, or keep reading our article.

Macroeconomic

A recession seems inevitable for the global economy. There are several causes: aggressive policy rate hikes by central banks to reduce inflation, an energy shock in Europe, zero-covid policies (ZCP), and a sluggish property market in China.

There is already a recession in much of Europe. The U.S. recession is expected to start in the third quarter of 2023, and China’s growth is likely to remain below historical levels.

There are many ways in which the situation could worsen: a breakdown in a key financial market due to the rapid rise in interest rates, a cold winter and blackouts in Europe, or a flare-up in US-China geopolitical tensions.

US

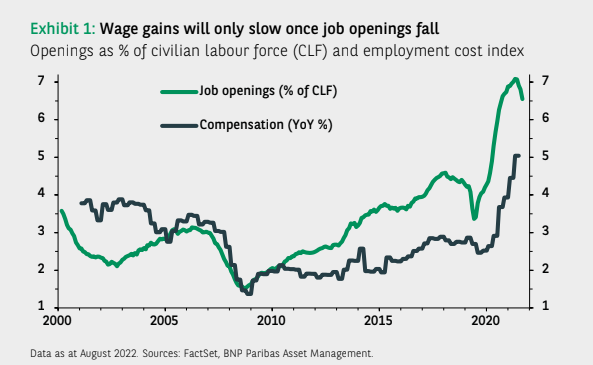

Because of the strength of the US labor market, which is reflected in both a low unemployment rate and high (nominal) wage gains, declines in non-farm payrolls in 2023 are likely. In order to control services inflation, the labor market must deteriorate. With base effects and lower demand, good inflation should decline, while shelter costs will eventually reflect the ongoing housing slowdown.

A key question is whether wage inflation can be reduced without a large increase in unemployment. There are still about twice as many job vacancies as there are workers, so companies are forced to raise wages.

Source: Investing in an Age of Transformation report

Europe

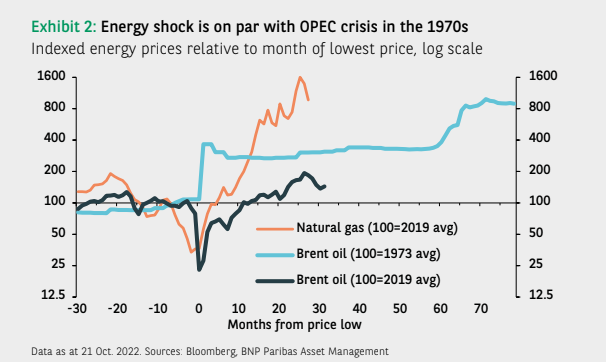

The energy shock Europe is experiencing is unlike anything the region has seen since the OPEC price increases in the 1970s. The price of gas has moderated recently, but it remains 10 times higher than the average in 2019.

Source: Investing in an Age of Transformation report

In some countries, inflation is in double digits, consumer sentiment has collapsed, and demand is weakening. BNP Paribas, however, believes headline inflation has peaked and will return to 2% by 2024.

Since the pandemic, governments have changed their response to economic shocks. As a result, governments have resorted to direct support to mitigate any decline in income (or profits) rather than rely on automatic stabilizers such as unemployment insurance.

China

In 2023, zero-Covid policies and an unsteady property market should moderate, allowing Chinese growth to rebound, though growth will likely remain below pre-pandemic levels.

Property market problems will likely take longer to resolve. As the Communist Party Congress has indicated, long-term policies will be pursued to create a housing system that ensures supply from multiple sources as well as to develop rental and real estate markets.

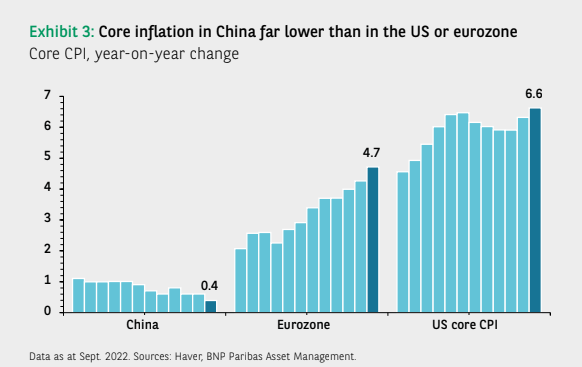

The government’s ability to stimulate the economy through fiscal and monetary measures is a key difference between China, the US, and Europe. Core inflation in the Eurozone and the US is over 6%, but only 0.4% in China.

Source: Investing in an Age of Transformation report

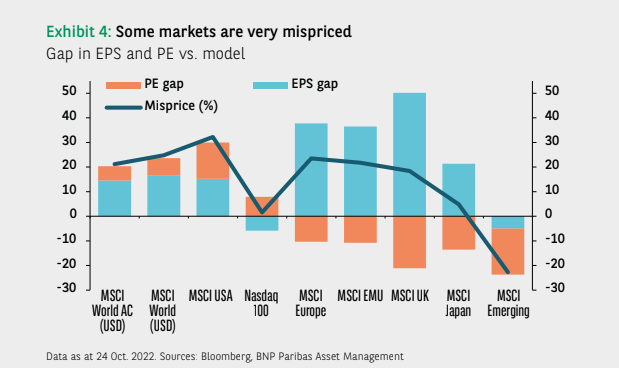

Market’s Outlook

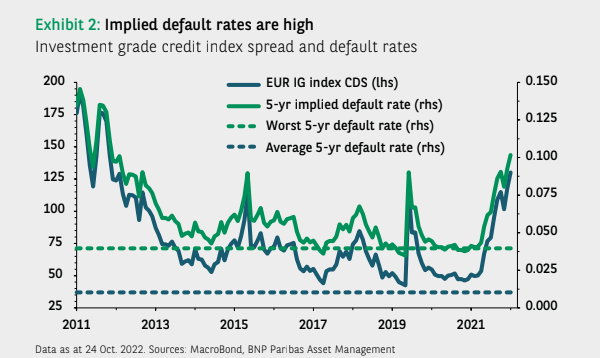

In 2022, real and nominal interest rates, as well as current and implied rates, increased dramatically in major economies. Despite the increase occurring across the curve, it was particularly sharp at the short end. It has been remarkable to see a 500bp rise in 2-year real rates since March, as well as a move from 1.5% to 5% in Fed funds in three years. In the past five years, five-year real rates have soared to levels last seen prior to the global financial crisis, which many views as a long-term guide for ‘neutral’ policy rates.

Central banks have been forced to set interest rates in the ‘rearview mirror’ due to persistently high inflation. By mid-2023, effective policy rates are expected to reach an effective rate of 5.0-5.5% in the US and 2.25 in Europe, just as growth and inflation weaken as the tightening already affects the economy. A pause may bring some respite for risk assets in rate hikes (the main driver of asset price weakness in 2022). How much is the question.

Source: Investing in an Age of Transformation report

The investment horizon is also peppered with geopolitical risks. Each of these developments could have an impact on both cash flows and discount rates, including the escalation of the Ukraine war and the energy crisis, China’s approach to Taiwan and the reopening of its economy, and trade wars and their impact on supply chains. The risks here are likely to remain high as there is no immediate resolution in sight.

Source: Investing in an Age of Transformation report

Sustainability

Environmental, social, and governance (ESG) criteria have been rigorously debated in the industry since 2005. During the discussion, parallel debates have been raging over what timeframe should be used to seek a maximum return and who should benefit.

Despite agreement in principle, much remains to be done to ensure ESG integration across portfolios is strong and accurate. Much of the recent criticism of ESG (including greenwashing) revolves around misleading claims made by some investors and messy ESG data. The regulatory community has stepped up its efforts to clarify what ‘sustainability’ is and how it should be applied.

As a result of the success of the ESG movement, broader discussions have begun on the future of sustainable finance. Investors have shifted from a purely financial focus on integrating ESG factors to recognizing that their ability to generate sustainable returns depends on a healthy planet and population.

Changes on the Way

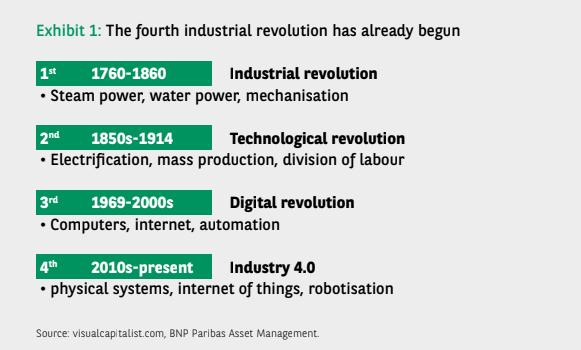

Climate change and the current energy crisis present long-term investment opportunities that can be analyzed by understanding the drivers of previous industrial revolutions.

Despite headwinds from crises such as food and energy supply stress and extreme climate phenomena, the world is on the cusp of a new industrial revolution – one that could lead to a more sustainable and greener future while allowing capacity – and resources – to be used more efficiently.

Industry 4.0 – which includes smart factories, autonomous systems, 3D printing, and machine learning – will enable a replenished biosphere, increased energy, food security, and improved living standards. As a result of computers, IT networks, and robotics, a new technological infrastructure will emerge.

Source: Investing in an Age of Transformation report

In 2023, the technology sector will be impacted by macroeconomic and geopolitical factors. In spite of this, BNP Paribas’ growth drivers and underlying technologies are considered sustainable. A long-term investment in digital transformation will result in higher revenues, profits, cash flow, and returns.

Last Words

Investing these days is quite a challenge and a risk. The above report presented the most important information and data on the state of the market, inflation, crises, or sustainability. We hope they will help you in your decision-making.

That’s it for today. If you’re waiting for more reliable information, sign up for our newsletter.