6 highlights from Deloitte’s Global Powers of Retailing 2020 Report

The world economy is in a rather precarious situation. Many countries are struggling with the economic crisis, rising inflation, and economic growth which is rather low. The year 2020 brings many unknowns, mainly due to the pandemic that has affected the entire world. In this text, you will find some takeaways from the report that Deloitte prepared based on the data from before the pandemic has started. If you want to dive into the topic, here you can download the full report.

Restrictions have a huge impact on global trade and retail

One of the world’s largest economies – the United States, is an excellent example of how huge impact on global trade this year has the COVID-19 pandemic. Two years ago, in the US, the average US tariff on imports from China was only 3.1. By the end of 2019, it reached 21%.

The average US tariff has always remained below all G7 countries’ (except Canada). Today it surpasses all G7 countries’ tariffs. The United States has the highest tariffs in 30 years. And they are one of the most important players on the world stage, which means most economies are experiencing this drastic increase in tariffs.

Eurozone has struggled, too

The eurozone also has some problems. They started in the second half of 2019 when the recession began. The main reason for this was the economic slowdown in Chinaand the decline in Italy’s activity. Germany is still suffering from weak investments and exports. No wonder, 2020 is not a good year for rebuilding economic power.

Thankfully the European Central Bank reacted to the problems in the euro area. Among other things, by further easing of monetary policy. However, according to the former ECB president, such steps may be insufficient and thus encourage to fiscal expansion, especially by Germany.

There are two German retailers in the Top 10 retailers

As you can see, we are talking about the Schwarz Group and Aldi.

Schwarz Group reached 7.6% of retail revenue growth. It moved up from 10th to 4th place. It’s quite a feat. This Group has under its wings, among others Lidl and Kaufland. It is constantly focusing on the modernization of stores and expansion to new markets, such as Serbia, Estonia and Latvia.

Another German-based retailer is Aldi. Its retail revenue growth reached 6,7%. Aldi is operating in 19 countries (including the latest entry in China), and its revenue from foreign countries is the highest in the top 10. It stands at a level of 66.3%.

All German companies in the ranking are doing quite well. They had the biggest retail revenue from foreign operations so it is clearer than Germans know how to expand their business.

There are also other German highlights in the Top 10: despite Amazon.com being classified as the US retailer, they can attribute their impressive growth (18.2) also to the increased volume of sales in Germany.

Geographic Analysis – Germany is rocking it

There are 34.4% of retailers from the Top 250 ranking across Europe. As many as 19 of them are German companies, and only a little less because 14 come from Great Britain. European companies earn as much as 40.7% of their retail revenue outside their homelands. This is more than the percentage for the entire ranking (22.8%).

Due to fierce price competition, discounters such as Aldi or Lidl focused on channel diversification by introducing, for example, self-service checkouts or e-commerce. The three giants, two from Germany – Schwarz Group, Aldi, and French Tesco, jointly generated revenues that excessed $80 billion.

Below you can find a list of every German store which is included in the Top 250 ranking.

| FY2018 Retail revenue rank | Name of the company | FY2018 Retail revenue (US$M) | FY2018Parentcompany/grouprevenue(US$M) | FY2018 Parent company/ group net income (US$M) D | Dominant operationalformat | #Countriesofoperation | FY2013-2018RetailrevenueCAGR² |

| 4 | Schwarz Group | 121,58 | 121,581 | n/a | Discount Store | 30 | 7.1% |

| 8 | Aldi Einkauf GmbH & Co. oHG | 106,175 | 106,175 | n/a | Discount Store | 19 | 6.7% |

| 16 | Edeka Group | 62,054 | 63,233 | n/a | Supermarket | 1 | 3.2% |

| 20 | Rewe Group | 56,435 | 62,971 | 507 | Supermarket | 13 | 4.5% |

| 34 | Metro AG | 28,724 | 43,454 | 414 | Cash & Carry/Warehouse Club | 25 | n/e |

| 38 | Ceconomy AG | 25,475 | 25,475 | (250) | Electronics Specialty | 15 | n/e |

| 85 | Otto (GmbH & Co KG) | 12,030 | 15,866 | 206 | Non-Store | 30 | 0.6% |

| 95 | Dirk Rossmann GmbH | 11,160 | 11,160 | 11,160 | Drug Store/Pharmacy | 7 | 7.3% |

| 98 | dm-drogerie markt GmbH + Co. KG | 10,905 | 12,804 | 132 | Drug Store/Pharmacy | 13 | 7.1% |

| 119 | Tengelmann Warenhandelsgesellschaft KG | 8,949 | 9,212 | n/a | Home Improvement | 14 | -0.2% |

| 136 | Adidas Group | 7,654 | 25,854 | n/a | Hypermarket/Supercenter/Superstore | 14 | 8.4% |

| 139 | Globus Holding GmbH & Co. KG | 7,510 | 7,580 | 107 | Hypermarket/Supercenter/Superstore | 4 | 3.1% |

| 161 | Bauhaus GmbH & Co. KG | 6,539 | 6,539 | n/a | Home Improvement | 19 | 3.9% |

| 166 | Zalando SE | 6,356 | 6,356 | 60 | Non-store | 17 | 25.0% |

| 176 | Deichmann SE | 6,024 | 6,842 | 159 | Apparel/Footwear Specialty | 26 | 5.0% |

| 214 | HORNBACH Baumarkt AG Group | 4,774 | 4,774 | 48 | Home Improvement | 9 | 5.4% |

| 222 | Müller Holding GmbH & Co. KG (formerly Müller Holding Ltd. & Co. KG) | 4,619 | 4,619 | n/a | Drug Store/Pharmacy | 7 | 3.8% |

| 232 | McKesson Europe AG | 4,375 | 24,506 | n/a | Drug Store/Pharmacy | 9 | 2.1% |

| 240 | NORMA Unternehmens Stiftung | 4,223 | 4,223 | n/a | Discount Store | 4 | 3.8% |

The Fastest growing retailers

There are two retailers from German that are growing rapidly. We are talking about Zalando and Adidas. The first one increase its revenue by 25% since FY2013. Adidas by 13%. There are a very good scores. Both companies’ revenues crossed 6,000 which is the reflection of its popularity among consumers around the world.

Since both of these are running e-commerce stores it is pretending that despite the fact that 2020 is being challenging for companies, both of them will performance consistently well on the global market.

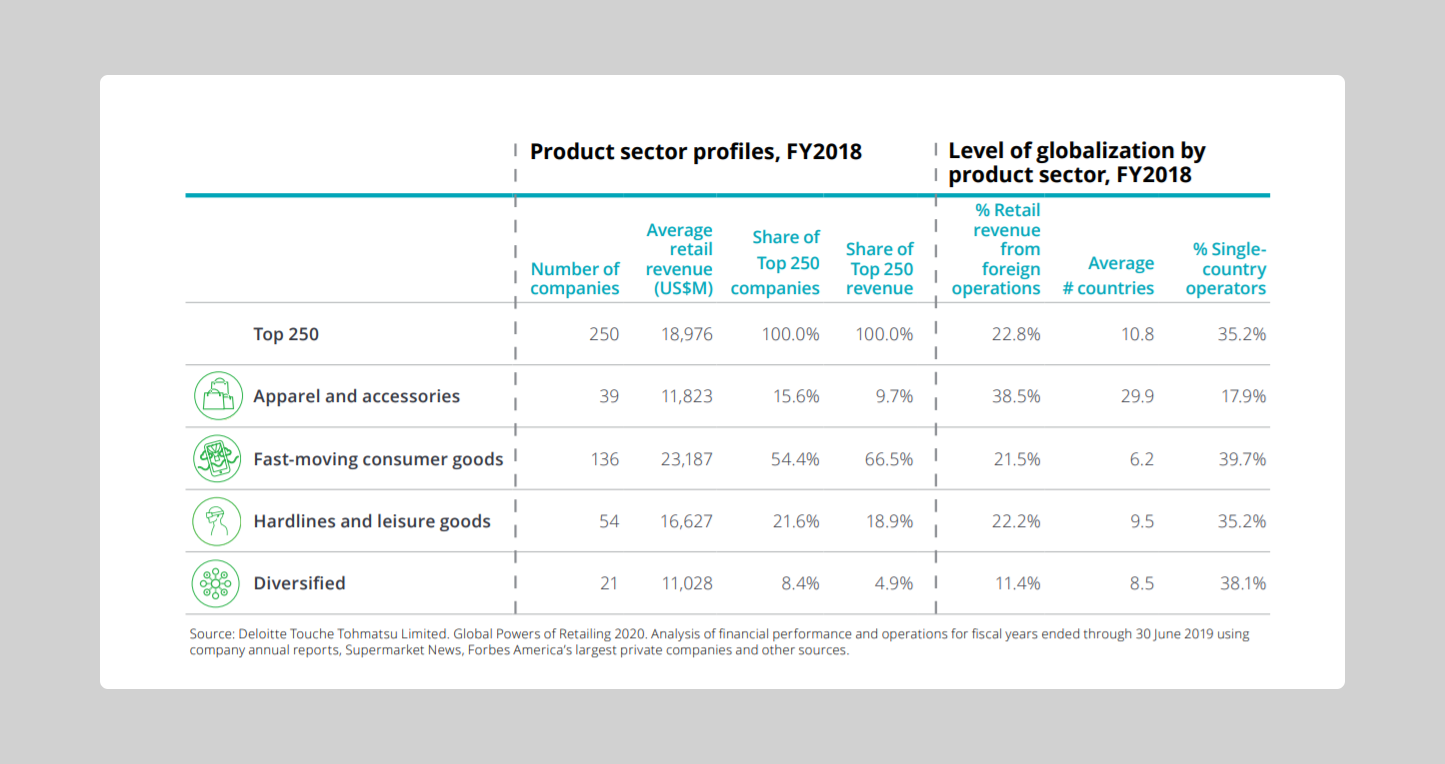

Over half of the companies in the Top 250 ranging belong to the FMCG market

The fast-moving consumer goods market is the leader not only when it comes to the number of companies. Its average retail revenue has crossed 20. Same with the share of Top 250 companies – FMCG markets covers above half of it (54.45%).

These numbers are not a big surprise. Three big players from this market (Schwarz Group, Aldi, and Tesco are in the first 10.

To sum up

Deloitte’s report is based on the data from FY2018 which has ended in the middle of 2019. Predictions for the future are not clear, the global situation is dynamic and it is hard to predict. If you want to learn more from the report we encourage you to download the full text and analyze some data.