A brief overview of China’s e-commerce in 2021

Competition between Chinese e-commerce giants is growing more and more. This year’s new payment systems will make things even more interesting as we’ll see significant players operating in new roles. The case is so interesting that 98% of urban Chinese consumers already use their digital wallet for daily purchases, and most consumers don’t carry cash anymore.

Below you can find some essential information from the report about China e-commerce and digital marketing q2 2021. Please read the full report for more details and statistics as it brings you the latest insights to help brands and companies ace marketing in China for quarter 2 of 2021!

New retail is blossoming

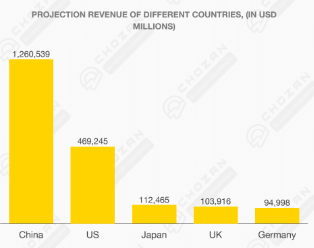

Revenue in the e-commerce market is projected to reach USD 1,260,539 m in 2021.

They are far exceeding that of significant players in The US and Japan.

Online consumption is growing at a rapid rate, but Chinese consumers require trustworthy and accessible shopping destinations. Marketplaces provide verified brand stores that give consumers a one-stop-shop. Brands need to be involved in such marketplaces for exposure and legitimacy.

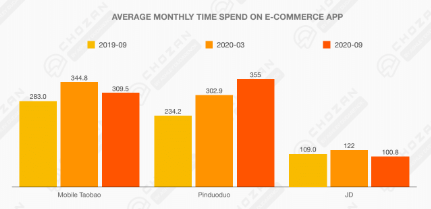

In post-Covid-19 China, users start spending more time on e-commerce. Pinduoduo is experiencing the most consistent growth in the monthly app use time.

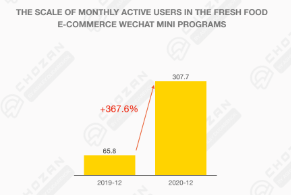

The exciting thing is about fresh food ecommerce growth and distribution. Covid-19 accelerated the new grocery e-commerce industry with nearly 370% growth on WeChat compared to the last year. Lockdowns, social isolation, a rapid rise in general health concerns, and an already blossoming delivery economy have culminated in favour of the industry.

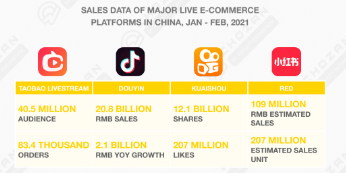

Another curious thing is about live streaming by platforms. Live streaming continues to support the growth of e-commerce in China as the conversion rate from live streams to sales increases yearly. Below you can see sales data of major live e-commerce platforms in China. 2021 will be another year of rapid growth in live streaming and video e-commerce.

China’s Internet giants

China’s internet giants like Alibaba, JD.com, Pinduoduo and Kuaishou are the winners as they harness significant network effects, billions of active users and financial leverage.

Alibaba

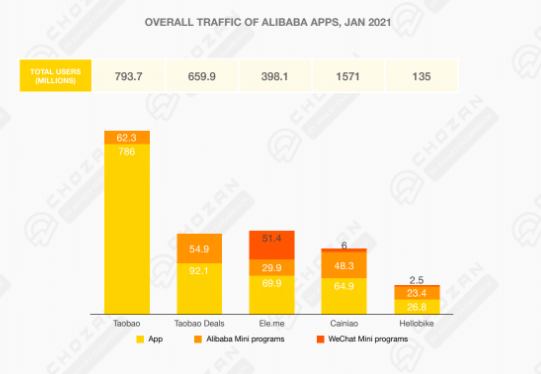

Alibaba started with the goal of becoming an online directory for China’s manufacturers and sellers and has since expanded its product range significantly. Two Alibaba market segments include Taobao, which is more general and allows consumers to search for any product they want quickly. At the same time, TMall caters more towards premium and high-end product consumers.

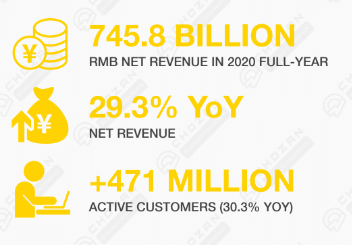

Alibaba announced its 2020 December earnings highlighting strong revenue growth of 37% YoY and EBITA growth of 22% YoY while Tmall’s GMV increased by 19% YoY. Yet, throughout this quarter and the rest of the year, Tmall will have to focus on defending its market share and ramping up GMV due to increased pressure from Pinduoduo’s organic growth as well as market regulators’ actions to create a more balanced and non-exclusive e-commerce environment, specifically between Alibaba and JD.

Tmall’s key measures to address this are new brand onboarding, brand incubation, continued emphasis on content marketing, livestreaming, KOCs, expansion of luxury channels, and focusing on the grocery category and local purchases.

What’s more, Alibaba continues to grow its business in all aspects.

JD.com

JD.com is the largest competitor to Alibaba, positioning itself as a retail firm (opposed to a marketplace) with a market dominance on electronic goods. Its end-to-end logistics approach makes it easier for JD.com to verify suppliers/distributors and maintain control over goods sold, while a quarter of its inventory is sold through its platform. Below is an overview of the 2020 full year.

JD is focused on using its supply chain advantage to stay ahead of the curve and deliver an experience that far exceeds expectations, whether that means ensuring a vast selection of products, providing a new venture or service, or influencing the creation of new products.

Like Alibaba JD continues to grow its business – JD has continued to increase numbers of stores throughout China, planning to open the third E-Space store in Xi’an this 2021.

Pinduoduo

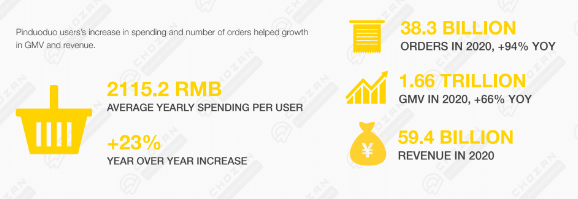

Pinduoduo is a recommendation based third-party platform. Aggregating demand through team purchases socially connects demand products to corresponding potential customers to avoid searching and scrolling through product options. The platform invests heavily into IP infringement minimisation as a priority to maintain trust with and between customers and users and associated brands/store. The regularity of the deals and the frequently purchased items involved mean that customers are more likely to return to the Pinduoduo platform.

Pinduoduo is the #1 group buying platform in China and the top agricultural, farm to table platform. These are two key areas where Alibaba and JD are playing catch up. If Alibaba, JD or another platform gains significant market share from them in the next year, it could spell big trouble for the social commerce pioneer.

Kuaishou

Kuaishou is one of China’s most popular short-video sharing and livestreaming social e-commerce platforms. Key opinion leaders (KOLs) control intense fan loyalty and trust, making Kuaishou an excellent promoter platform driving traffic to online stores. Recent decisions to massively increase investment by Kuaishou in livestreaming infrastructure and capabilities indicates its increasing success – especially seen during the current maintain COVID-19 pandemic.

Kuaishou will continue to focus on optimising its traffic allocation. The platform will also allocate more user traffic, through an internal bidding system, toward mid-level MCN-backed KOLs and merchant livestreaming instead of top KOLs.

To sum up

Chinese’s market is dynamically changing, and you can see it thanks to numerous statistics. Businesses appreciate the importance of brand experience, and they are now reevaluating their strategies to find growth in China. Alibaba excels, but its competition isn’t far behind. Stay up to date with Chinese’s e-commerce and see how the situation changes!