Luxury Goods: trends and predictions for 2022 (Bain Report)

“Luxury is back… to the future” is the title of the latest market study worldwide by Bain – Altagamma.

With 2022 already knocking on our doors, it’s time to step into another year full of new and interesting trends, figures and actions for the Luxury Goods market.

From insights to the performance of the market, through estimates for the approaching us 2022, all the way up to some key recommendations – this study contains data no one from the Luxury Goods industry should overlook.

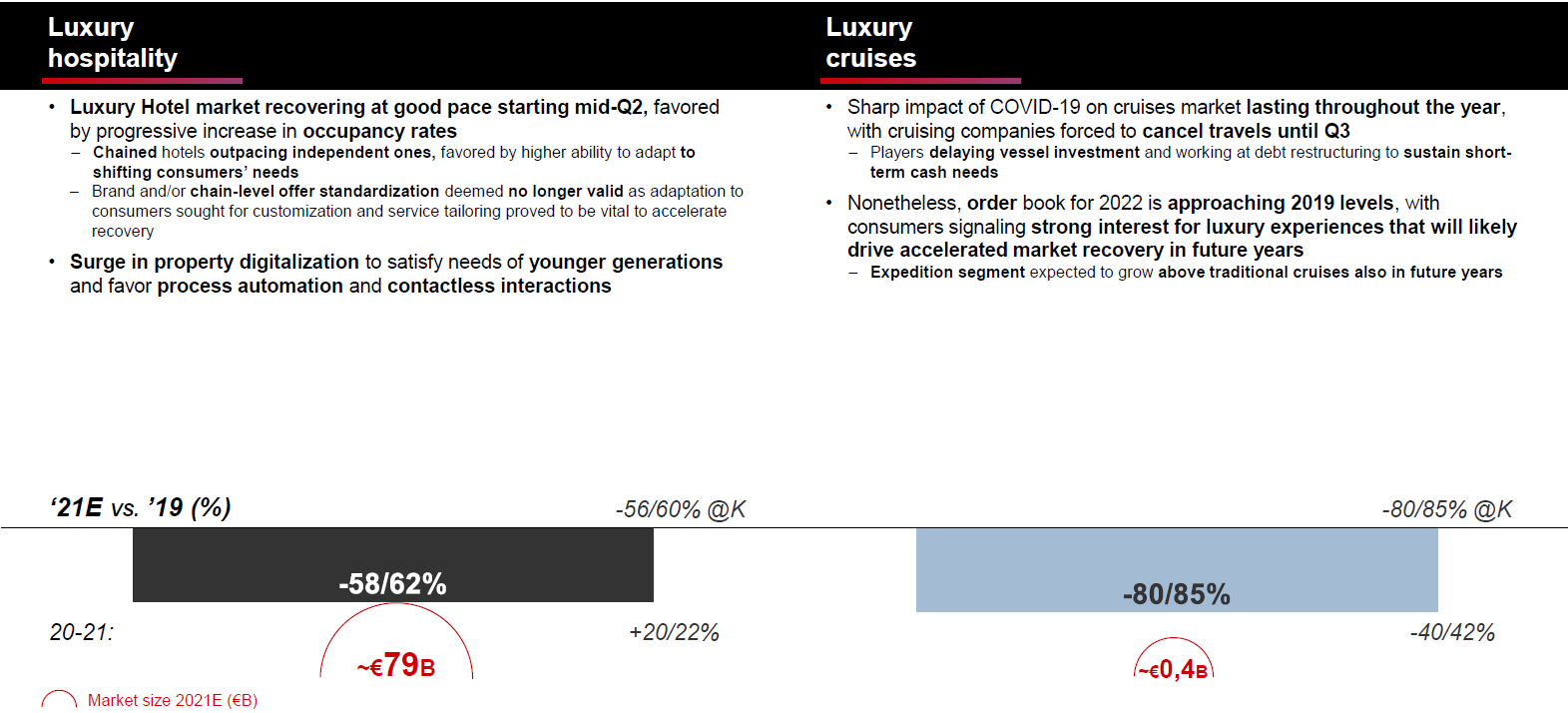

Global luxury markets include items and services like personal luxury goods, cars, hospitality, gourmet food & fine dining, fine art, private jets & yachts, and even luxury cruises.

When it comes to the overall value of this market, luxury cars significantly outperform all of the other components combined. More specifically, they make up for almost 50% of the whole market.

The estimated value for the whole market in 2021 is € B 1.140.

3 Top Performing Categories – High-Low:

- Design furniture

Core high quality design market, already showing stronger-than-forecasted performance in last quarters of 2020, continuing on its growth path sustained by continued refocus of consumer spending on home, in particular on Living& Bedroom, outdoor and lighting.

- Fine wine and spirits

Spirits driving maret recovery thanks to growth in local consumers’ interest for Asian spirits, increasing interest for status spirits and better ability vs ine brands in catering interest of younger generations.

- Luxury cars

Market favored by positive consumption tailwinds, yet partially slowed-down by disruption across the supply chain.

Top 3 categories on their path to recover to pre-pandemic levels:

- Private jets & yachts

Luxury yachts confirming positive momentum, with growth in deliveries paired with sharp growth in order books.

- Fine art

Fine art market rebounding thanks to gradual reopening of public auctions and art fairs.

- Gourmet food and fine dining

Driven by the dichotomic impact of pandemic outbreak in 2020, the luxury food market is showing significant difference in growth rates within its components.

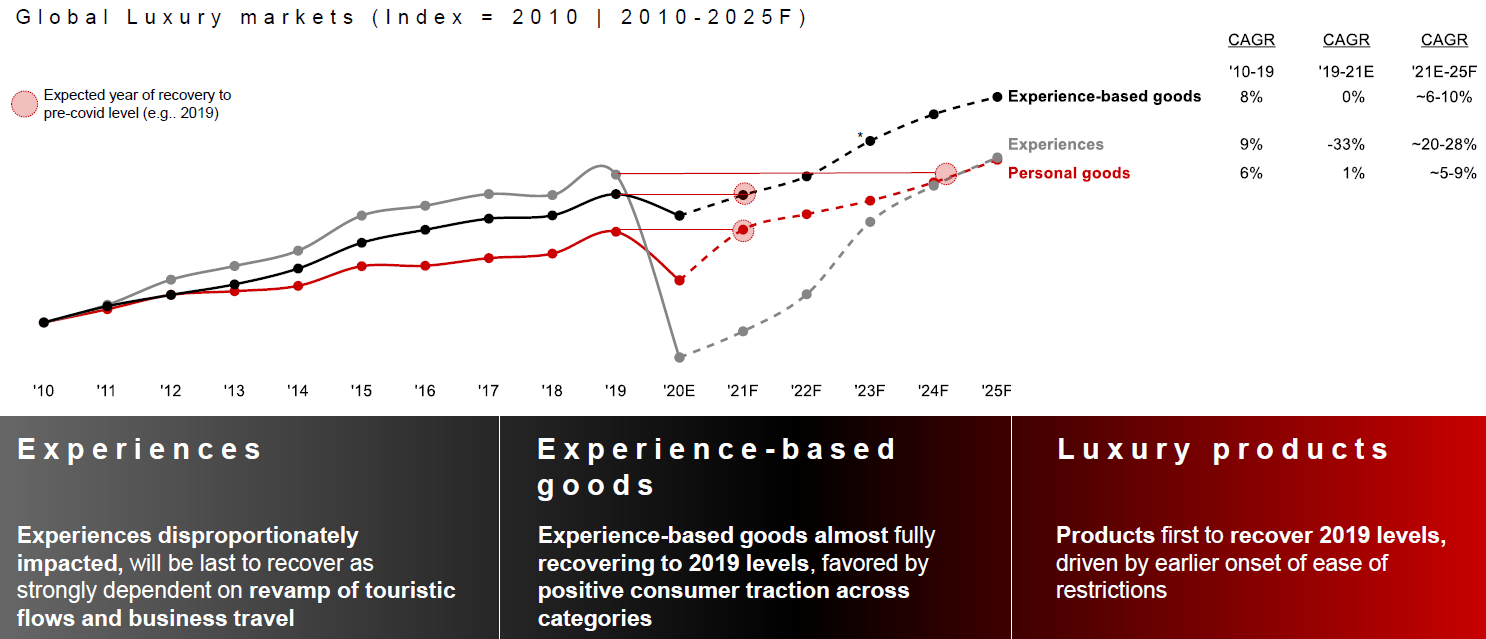

Not all sectors can enjoy stable recovery, however. There are sectors that were affected by the pandemic much more, and one of them is experiences.

The experiences sector, including travel and any in-person brand experiences, is still way below its pre-covid levels, mostly because of travel restrictions.

Unfortunately, it doesn’t show signs of improving sooner than in 2024 back to its 2019 levels. Despite the slow recovery process, however, the demand for experiences to be allowed back is higher than ever.

“Consumers overindulged on products, but the willingness to go back to experiences is at an all-time high” – we can read in the report.

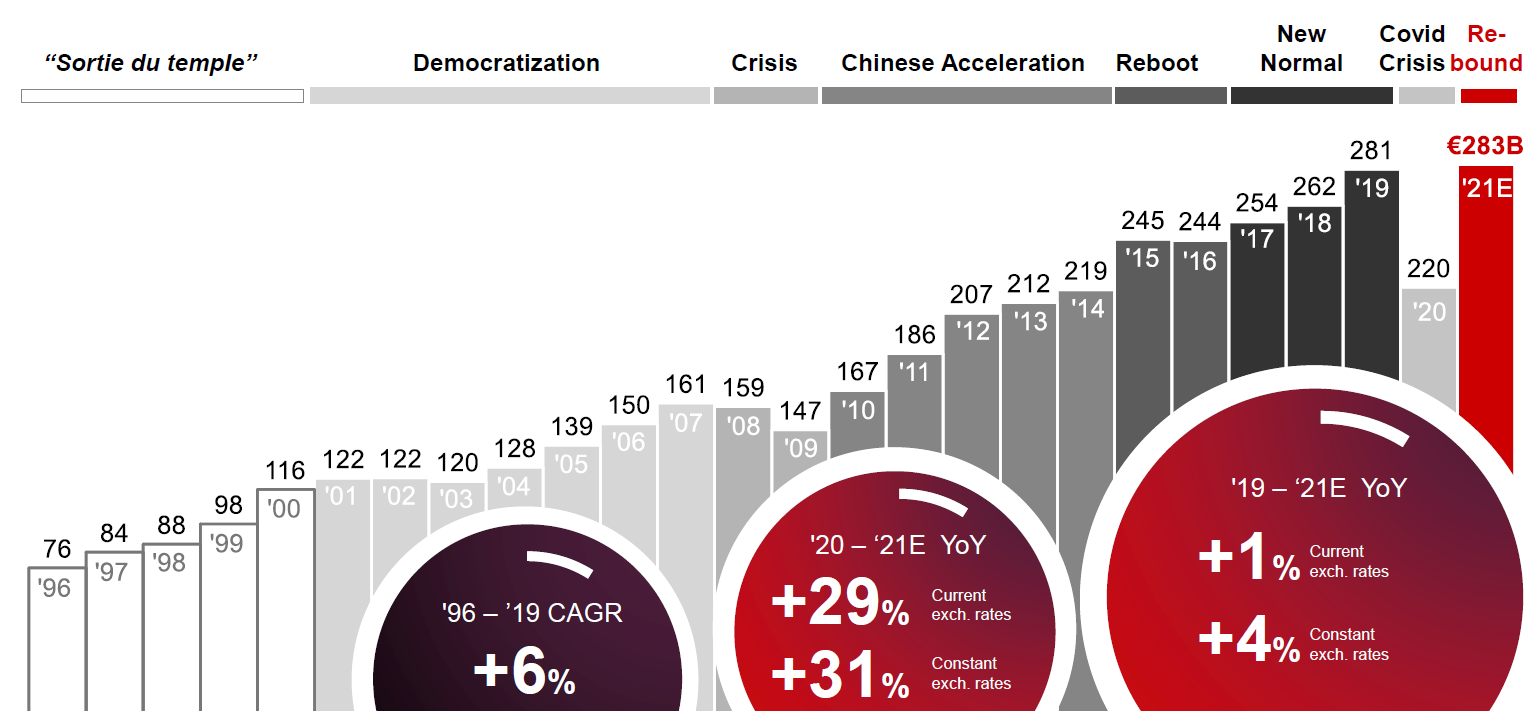

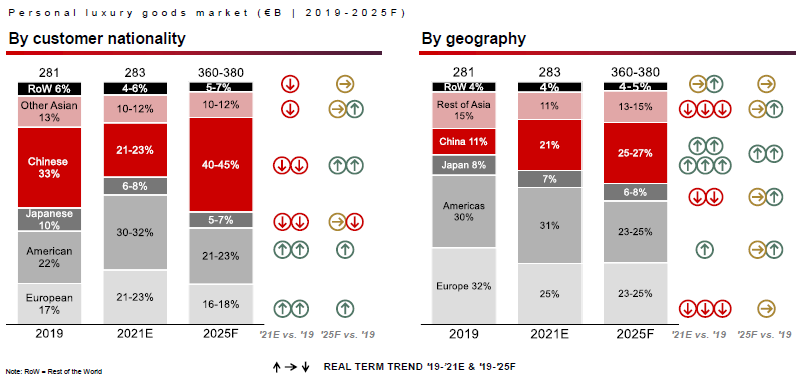

Worst dip in history for the personal luxury goods market:

Personal luxury goods are items like jewelry, luggage, haute couture clothing, sports cars and more.

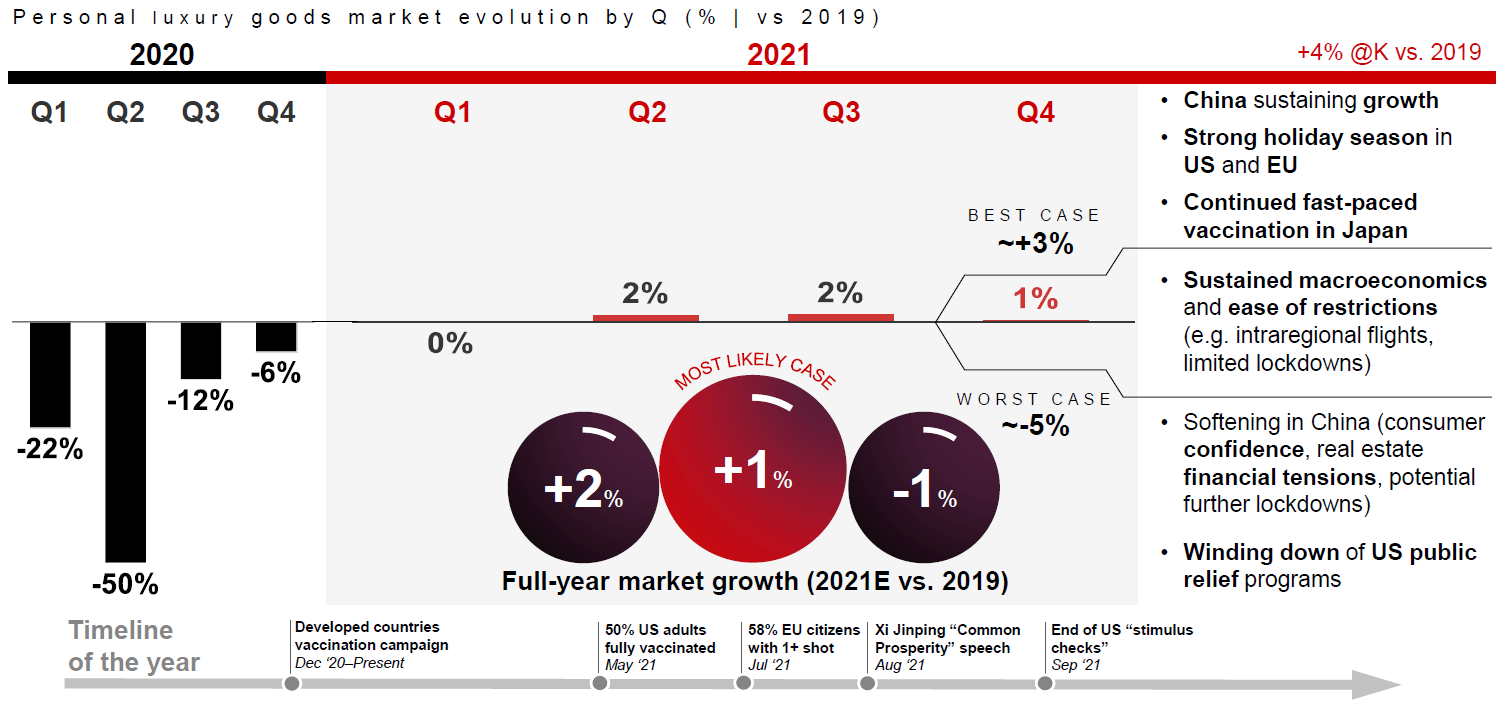

Interestingly enough, the pandemic caused this market to experience its worst dip in history. Later on in 2021 that dip turned into a V-shaped recovery, with the value in 2021 being slightly bigger than before the pandemic.

Even though this market is constantly improving since Q3 2020, there still is some uncertainty when it comes to the next holiday season. What will it bring?

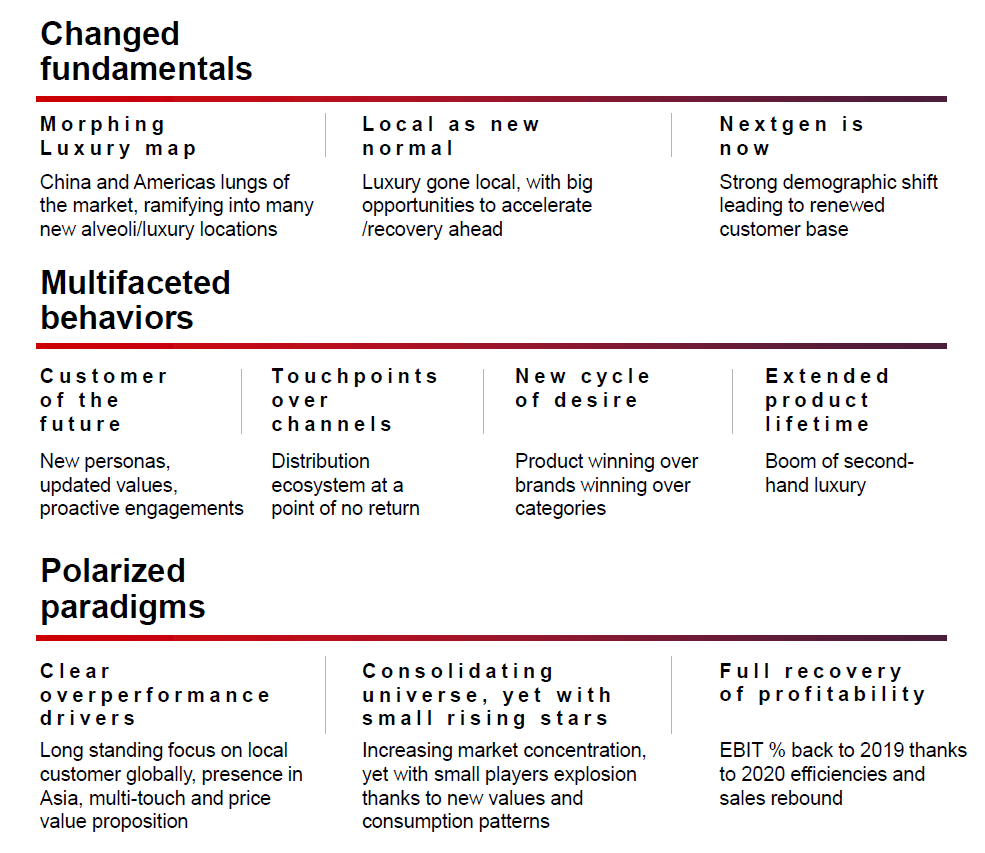

COVID-19 – A new beginning? Emerging changes

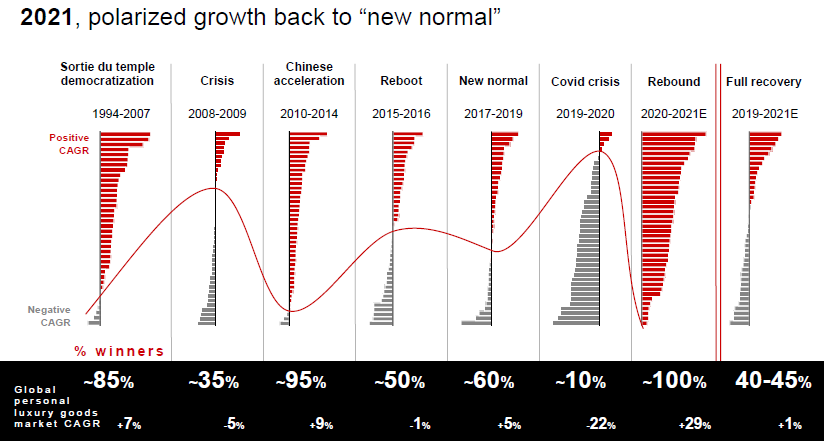

After 20 years of large expansion and deep evolution, Covid-19 has fast forwarded and anticipated some of the key changes for the next 20 years of the global luxury market.

This reports reveals and describes what they are:

Morphing Luxury Map

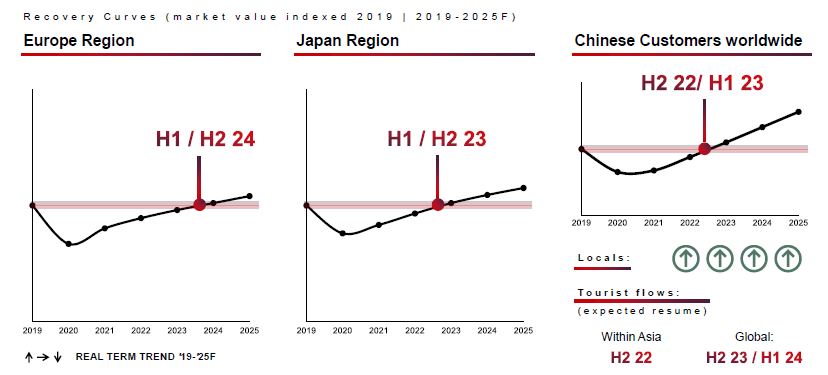

China doubling and Americas booming, Europe and Japan are still in recovery mode.

M. China:

- Strong cross category, generation and price growth.

- After softening in Aug-Sept, consumption restarted strong in October despite scattered lockdowns.

- Hainan as the key touristic luxury hub.

Americas:

- Solid rebound, polarized between entry prices and tops items.

- Strong market share shift towards European brands.

- Evolving luxury map: new cities emerging, large cities back and persisting suburban areas.

- Blasting Brazil.

Europe:

- Local consumptions are strong everywhere.

- Some tourists bounce back over the summer.

- London and the UK suffer the most, while Russia is championing thanks to a strong repatriation.

Asia:

- Weak Hong Kong vs mixed Taiwan and Macau.

- South Korea back to 2019 levels: full repatriation of local customers over-compensate for the lack of tourism.

- SEA is still suffering from a lack of tourism.

Japan:

- Local consumptions impacted by the slow vaccine adoption.

- Fukuoka is emerging as a rising star.

- continued focus for large established brands, with few exceptions intercepting the next gen of customers.

Rest of World:

- The Middle East is very strong throughout markets, with Dubai and Saudi Arabia leading growth.

- Struggling Australia which only recently reopened after months of lockdown.

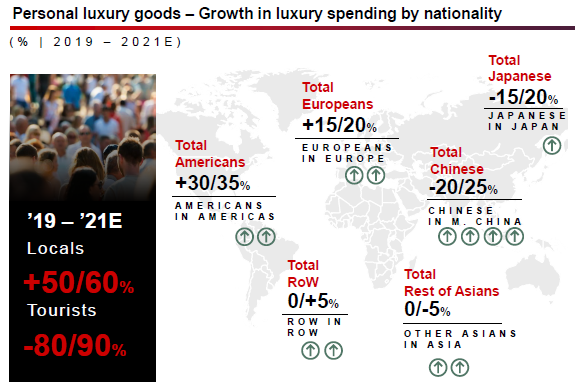

Local as new normal

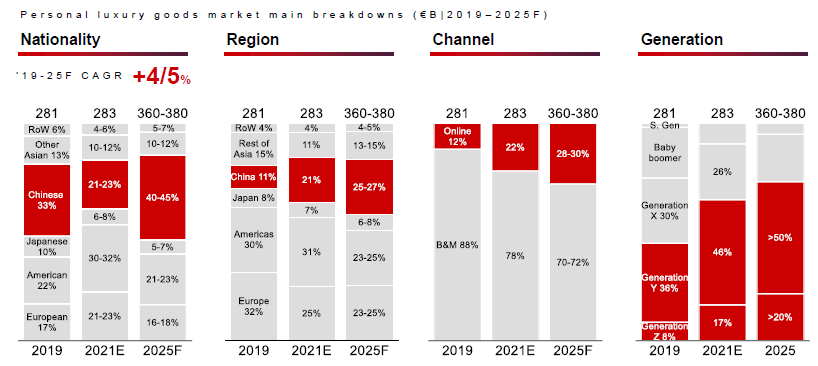

- There will be some changes in the growth in luxury spending by nationality

- Some countries will finally see some long awaited recoveries: China, Japan and European countries.

- Chinese customers will be back by 2022-23, Japan by 2023 and Europe in 2024. Globally, things should go back to normal between 2023 and 2024.

- China’s time to shine – again.

The study reveals that some of the consumption fundamentals of China will go through changes.

Examples include: acceleration of middle class and consumption upgrade, pressure on uber-wealth, delayed spending given current uncertainty.

In general, luxury brands have the chance to secure common prosperity, but they will need to challenge and adapt their strategy.

The year of 2021 confirmed China’s growing importance in luxury, together with a bright evolution for European and American customers.

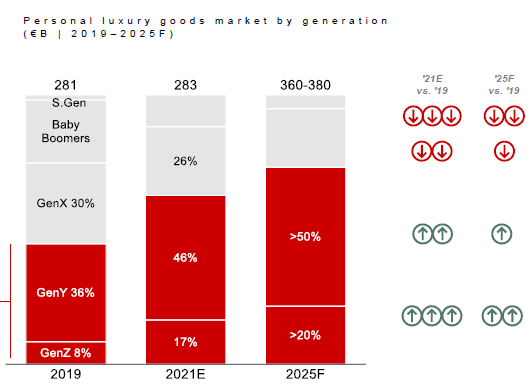

Next gen is now

People under 40 years old will remain main drivers for growth up to 2020 in the luxury goods market. Moreover, Gen Y and Gen Z are expected to contribute roughly 180% of the total growth from 2019 to 2025.

What other changes can we expect looking at consumers’ age?

Older generations will be permanently leaving the luxury market. However, the spots will be replaced by new consumers, mostly Generation Y and Z. In 2021, they accounted for around 30% of new customers that entered the market since 2019, which is a total of 25% of the Personal Luxury Goods market.

Customer of the future

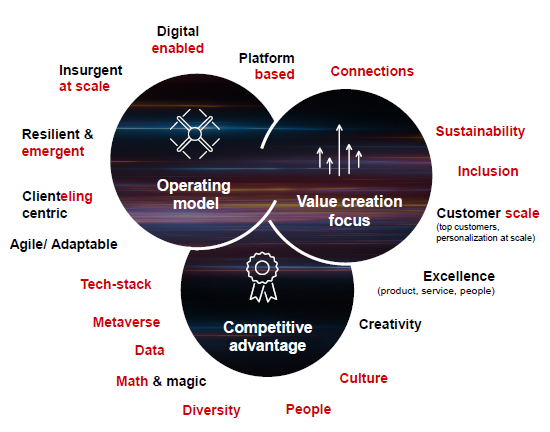

Cultural relevance and evolving values ask for a new value-creation model in customer engagement.

There will be a new value creation model (high tech & high touch), new KPIs to track (earned growth rate) and clear positive results (churn rate reduction) – a lot to look forward to.

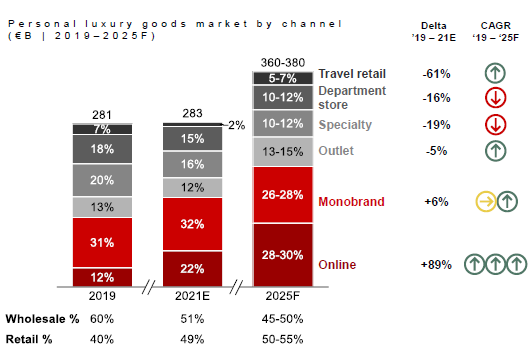

Touchpoints over channels

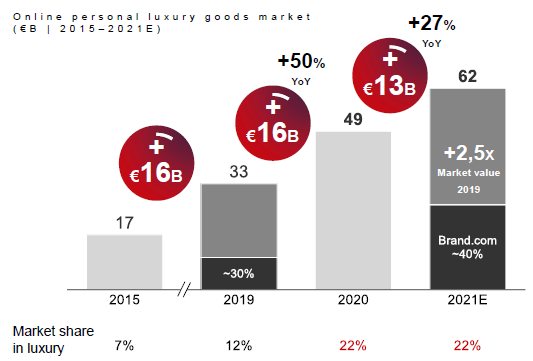

Online and monobrand, key channels for 2021 recovery, will lead the mid term growth of the industry. The online personal luxury goods alone almost doubled in 2 years.

New cycle of desire

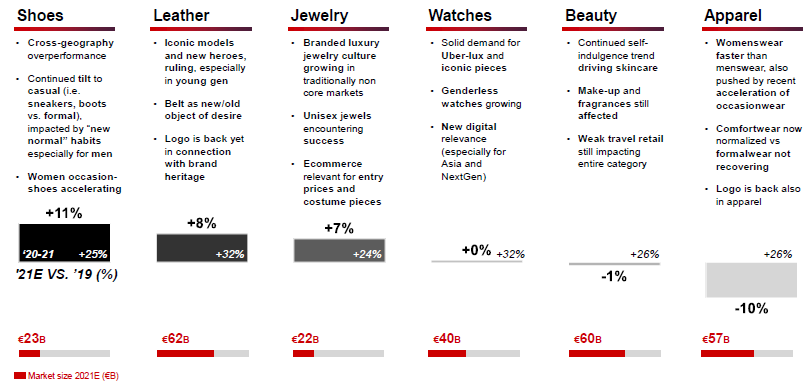

Best performing categories of 2020 are already beyond 2019 in 2021, watches and beauty on par, apparel is still lagging.

Shoes, leather, jewelry, watches, beauty and apparel – these categories can expect changes, with the highest growth between 2019 and 2021 being the shoes category.

New role of brands

It seems that traditional market segmentation lost its relevance. Now, brands are multi-price points to answer to different customer needs.

Extended product lifetime

In order to extend the lifetime of luxury products, the second hand market will be booming in the years to come.

This provides both opportunities as well as potential threats to brand, fashion platforms and investors.

Opportunities include entering a growing market, developing a network-based business model, showing commitment to sustainability, gathering data on customers and more.

The threats revolve mostly around understanding the winning value proposition, cracking operation complexity and defining logo and rebranding strategies.

Polarization and profitability

Overperformance drivers, consolidating strengths and profitability full recovery

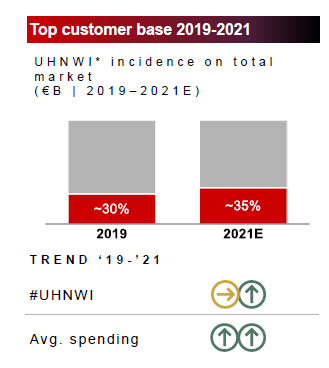

- Clear overperformance driver: the focus will be on local customers, exposure to China, multi-touch and price value proposition – these will be the top drivers of resilience.

- Increasing market concentration, yet with high dynamism from rising stars.

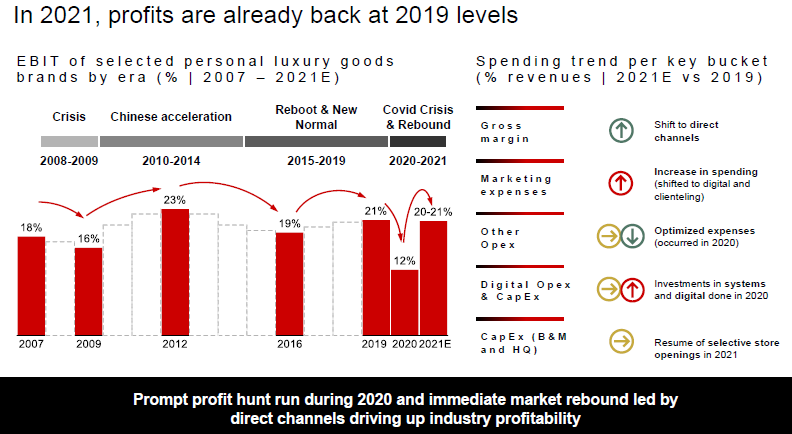

- In 2021, profits are already back at 2019 levels.

Key takeaways:

- The top growth drivers are Chinese consumers in China, online channels and younger generations.

- 2020-21 is the turning point for establishing the keyword for the next 20 years of luxury.